December 2019 was a relativity quiet month as far as P2P news is concerned, compared to the 3 preceding months anyway. The new FCA lending rules kicked in on December 9th, and Landbay stopped accepting retail investors (more on that later). My overall P2P income was up a little from November in both the GBP and Euro portfolio. XIRR fell a little in the GBP portfolio as I started the rebalancing process.

Rebalancing

Last month I discussed how I intended to rebalance my portfolio. My thought last month is that I would have 20 or more GBP accounts with £10k per account. Unfortunately what I’ve realized is; there may not be enough (what I consider to be) safe Peer to Peer lenders out there to distribute the capital with that much diversity. Also Landbay stopped accepting retail investors, so I also have one less account than I thought. So I decided to up the maximum amounts a little to £15k per lender, which is still a 50% reduction in exposure from some of the larger accounts I had. I’ve been executing this in December which became a little bit messy at the beginning as I cashed out too much to bring accounts down to the initial £10k, then ended up sending capital back to them when I realized that in order to keep most of my capital invested, I would need to up the stake to £15k.

New Lenders

I’ve been looking at a couple of new lenders but honestly I haven’t put a great deal of time in to it yet as December was a busy month for me personally. Because of this, I have some money now sitting in the bank not earning anything. Hopefully I’ll get time in the coming weeks to look at some new lenders and distribute the cash.

Moving On

If you would like to see historical individual Peer to Peer lender account screenshots from my lending accounts etc. You can click on the links next to each Peer to Peer lender update and go to the account page where you can see balances and what I’m actually invested in.

For the current month, I have added thumbnails of account screenshots below the account title. Click on the thumbnails to enlarge.

GBP Portfolio Update

Income from the GBP Peer to Peer lending portfolio was up from £403.12 in November to £633.31 in December. Funding Circle again hit me with a bunch of defaults but came in with a £19.28 overall gain for the month, which is still pretty bad all things considered.

Overall Portfolio XIRR was down a little again from 5.59% in November to 5.51% in December. This was due to portfolio rebalancing as well as all of the larger lenders reducing their targeted returns.

You’ll notice now that the overall portfolio is starting to look a lot more balanced as far as exposure to any single lender. I’m still drawing down Funding Circle and Assetz Capital as selling loans in both is taking a little more time than other lenders. Lenders that are not yet at the £15k mark like Unbolted, CrowdProperty, LendingCrowd & Ablrate are purely because it’s taking time to get invested. I’ll add more capital as the cash balance gets lent out.

I honestly haven’t been paying a lot of attention to Ablrate. Everything is going as expected but I really need to increase my account balance with them. The problem is “time” at the moment as Ablrate takes a little bit of time to get invested with, as it is all manual lending and they don’t have many new loans each month. There are several loans to buy on the secondary market still so I’ll take a look as soon as I get some down time.

XIRR was down a little from 13.40% in November to 13.11% in December. The XIRR on Ablrate is still high (for a UK lender). This I believe is mostly due to some secondary market loans I bid on. When bids are accepted lower than the original loan value on the secondary market, the XIRR goes up to reflect this.

Ablrate Signup & Cashback Offers

Ablrate offer £50 cashback on your first £1,000 investment.

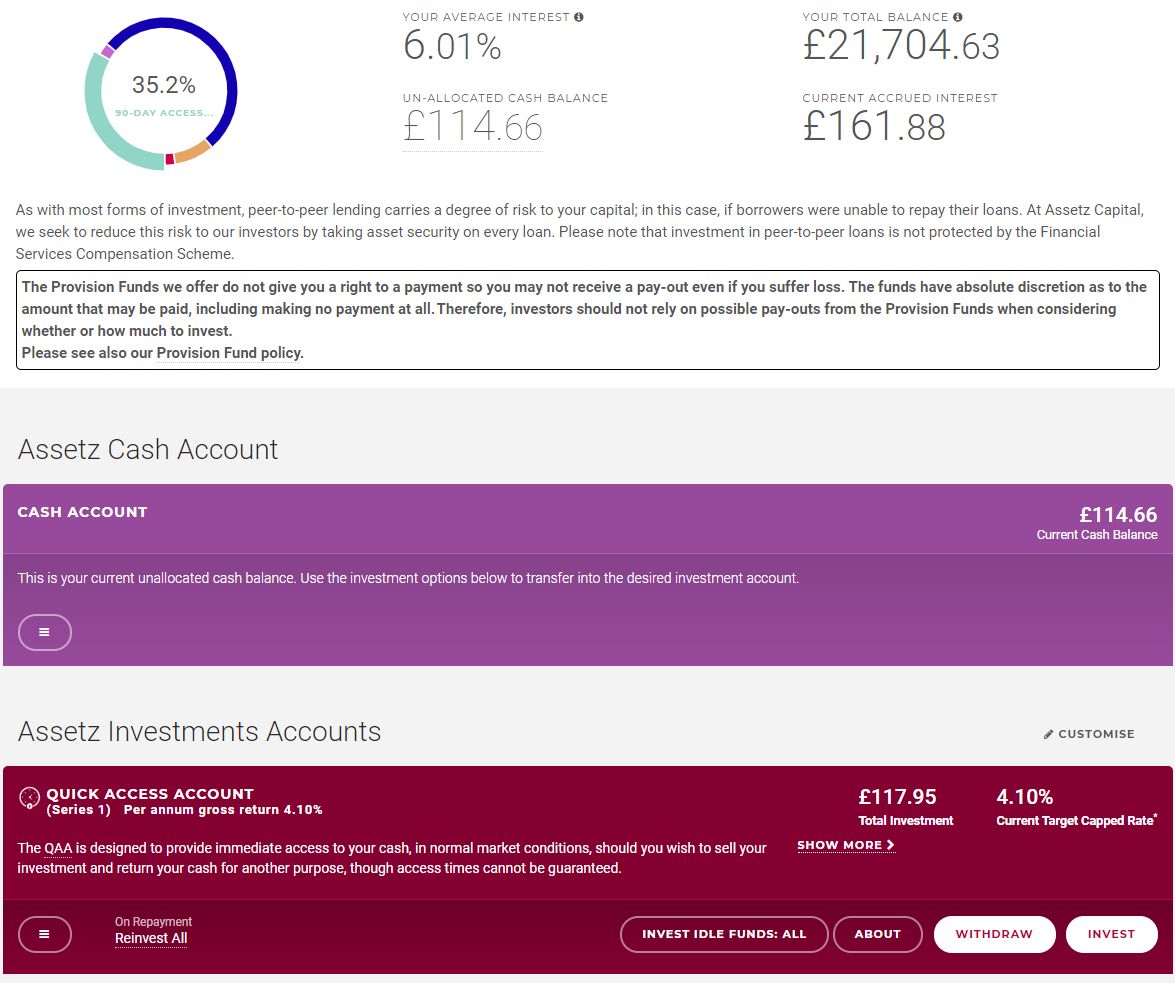

Assetz Capital announced in November that they will no longer be allowing investment in their PSA (property Secured Account) or their GBBA2 (Great British Business Account Series 2). Current investors can remain invested in both accounts if they want to. However because I have decided to reduce the larger account exposure I have started to sell out of Assetz PSA & GBBA2. It’s slower than I thought it would be but overall not too bad.

XIRR increased a little from 5.58% in November to 5.93% in December.

Assetz Capital Signup & Cashback Offers

Assetz Capital’s last cashback offer finished on November 30th unfortunately (Booo). But they are still one of the best and safest lenders out there.

If you’re considering investing with Assetz Capital, please

CrowdProperty are a new lender I added to the portfolio in October. In short; a first charge, secured property lender with an excellent track record offering 7%-8% returns on medium term (12-24 month) loans. Rather than go through everything in this update, I decided to write an initial review here for anyone interested in taking a look at them.

I increased the investment to £10k in November and set up Auto-Invest with a £500 maximum in to each loan. Not all of it has been lent out yet unfortunately as the auto-invest only takes a percentage from each lender to fill the loan based on the maximum investment set. So sometimes I get the full £500 into a loan, but other times I only get £100 or £200. It seems the way to get money lent out faster is to be in front of the computer when a loan comes live as I’ve found I can get the full £500 if I’m fast (the loans sell out in a couple of minutes). Unfortunately it seems I’ve been away from the computer at 10am most days when loans come live so I’ve had to stick with the auto-invest, and thus, getting some cash drag.

Returns

My CrowdProperty account won’t begin to show much return for the first few months as most of the loans I’m invested in don’t pay returns until the loan completes when all capital and interest is paid back. This is normal with some development loans as it allows the developer to complete the project and sell it before having to worry about large loan payments while the project is ongoing. Obviously this adds some more risk to the loans, but that’s why most are paying around 8%.

If you’re looking for higher returns in GBP lending, definitely worth checking CrowdProperty out. Please consider using the link below so CrowdProperty will know that I sent you.

As you’ll know if you’re a regular reader of Obviousinvestor.com, I’ve been trying to get out of Funding Circle since July 1st 2019. It’s taking a while but I’m slowly getting there.

XIRR declined again from 3.89% in November to 3.75% in December. I’m still showing an overall profit with Funding Circle at least, but again there were defaults to the tune of £146.93 in December. Not as bad as last month but still no fun.

I did manage to withdraw £1,600 in November (from repayments & loan sales) and it all went to Loanpad where it’s safe and I can get almost 6% 🙂

Selling Funding Circle Loans

Just as a reminder, Funding Circle have changed the way their selling feature works on December 2nd. Instead of sellers having to wait their turn to sell all of their loans, they are going to cycle between sellers in a “round robin” fashion, just selling parts of their loans before moving on to the next lender. So in theory, this gives everyone a chance to get some capital back quickly.

The problem is they have now introduced a 1.25% selling fee, which is going to the buyer of the loans as an incentive to purchase them. That kind of sucks when it used to be free to sell loans early, and it was the initial agreement when I first invested the money. I understand why they are doing it, however personally I think Funding Circle are making a huge mistake putting the fee onto current investments. They are basically holding investors capital for ransom and alienating them even more than they were before. Not a good idea for a company that’s not yet profitable and now has such a bad reputation already.

New Selling Feature Update

As an update on the selling feature; it’s total rubbish. I’ve now sold about £1000 in December which I’ve been charged for at 1.25%. Funny thing is, I was only able to withdraw just £100 more than last month (which was just from repayments, so no sales and no charge). Seems to me there is something not quite right about that but there is not much I can do. I’ll just keep selling until I can get out and put Funding Circle down to a learning experience. If it wasn’t such a huge company, I’d have to say that Funding Circle is a scam.

Unfortunately though, Funding Circle are just a classic example of how greedy corporate executives can ruin a good company. I updated and wrote in my Funding Circle review how they got here.

Funding Circle Signup & Cashback Offers

For anyone considering investing in Funding Circle, I would suggest you wait and see how things pan out, there are better lenders to invest with at this time.

However if you’re a new investor, and do still want to invest with Funding Circle (bad idea), the cashback offer for new investors is: Invest £2000 and receive £50 Amazon Gift Certificate. If you are hell bent on investing with Funding Circle, you may as well get the bonus.

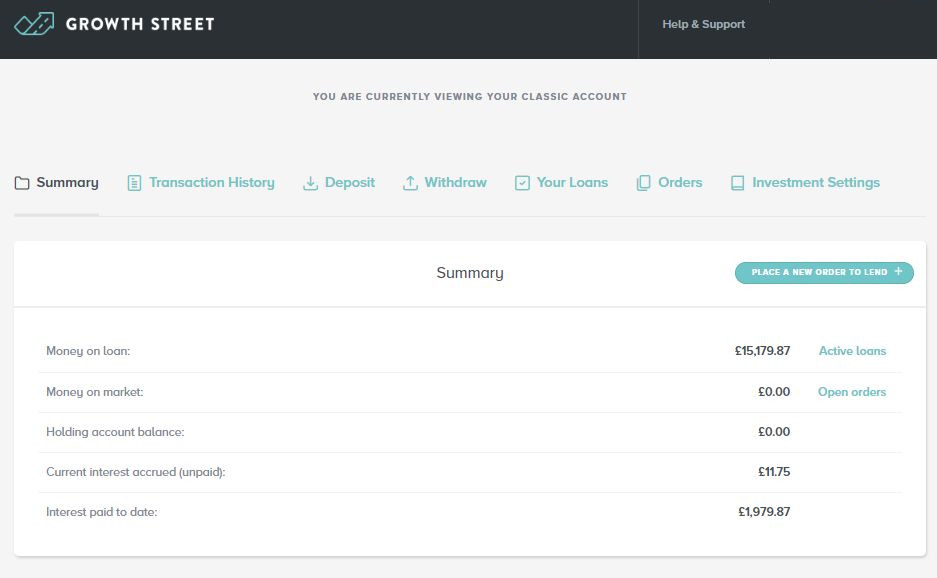

Decreasing my investment with Growth Street makes me sad, but it had to be done to stick to the diversification rules. I have to say though it is just about the easiest lender to get capital returned from. I simply turned off auto-invest and I had the capital ready to be withdrawn in 2 weeks. No problems. Being able to get 5%+ returns and having (almost guaranteed) access to your capital within 30 days can’t be beat.

XIRR down just a little from 5.16% to 5.10% in December, mostly because I switched off auto-invest and forgot to check how many loans had been sold, so I ended up selling too many. It’s all ok as I was able to get back in again but it took a couple of days so there was a little cash drag.

Growth Street Signup & Cashback Offers

For new investors, Growth Street have a very decent cashback offer: Invest £5000 or more for 1 year for £200 cashback.

I increased my investment with Kuflink in December to the £15k mark, so they are now at the account limit. I consider Kufflink to be one of the safer lenders so I had no hesitation on doing this.

XIRR dipped a bit from 6.65% in November to 6.52% in December. This was due to a bit of cash drag while I was waiting to get invested into new loans. No problem though, almost fully invested now. Just a few hundred left which should get lent in the next week or so.

Check out the new cashback offer below if you’re considering investing with Kuflink.

Kuflink Signup & Cashback Offers

Kuflink have a great cashback offer right now which is well worth taking advantage of if you are thinking of investing with them. You can get up to £500 in cashback bonus (depending on how much you invest).

New Kuflink customers receive the following Kuflink cashback on an investment of £100 or more when they use signup links from obviousinvestor.com. Must invest into loans within 14 days of first investment to qualify for cashback.

In a surprise move in December, Landbay returned all retail investors capital (including any bonuses owed) and said they would no longer be accepting retail investors. As retail was only 3% of their investment business, I assume they didn’t want to have to deal with the new FCA rules. Rather than go into a long diatribe about the situation here, I updated my review with all of the information so take a look at the review for further info.

This didn’t help with my diversification plan as this is just one less lender to distribute capital to. They did everything professionally and ethically though so I have nothing bad to say about Landbay.

LendingCrowd monthly income is not as consistent as some other lenders, but they still deliver over time with XIRR sitting at 7.50% in December. This was down a bit from 7.58% in November due to some cash drag. Loan flow has been down for the last few months but defaults have been in check so I’m happy overall. Hopefully the loan flow will pick up in 2020 so I can get some more capital over there and take more advantage of these great returns.

LendingCrowd are proving out over time to be one of my most profitable lenders. I’ll be upping my investment with them to get to the total of £15k diversification target. I may need to drop my lending rates a tad to keep from getting cash drag, but I’m willing to do that now I am feeling safer with LendingCrowd.

LendingCrowd Signup & Cashback Offers

If you’re new to Peer to Peer lending and would like a shot at some higher rates; take a look at one of the last P2P lenders that still allow bidding on loans so you can get the best rates! LendingCrowd have Up to £400 cashback for £10,000 investment.

I withdrew from Lending Works in December to meet my diversification targets. It was difficult to do so as they are about the safest lender out there in my eyes. Selling loans was quick and easy, it took just a couple of hours. I made the same mistake here as I did with a couple of other lenders by withdrawing the account down to £10k, then having to send £5k back when I realized diversification was going to be difficult at the £10k level. Lending Works then wouldn’t let me back in for 20 days because of the free sell out they did.

Because of this, Lending Works XIRR decreased just a bit from 5.82% in November to 5.58% in December. This will obviously continue to decrease now due to the new, lower target number of 5.4%.

Lending Works Signup & Cashback Offers

If you decide to invest with Lending Works (which if you’re getting in to P2P, is a sensible idea as part of a diversified portfolio).

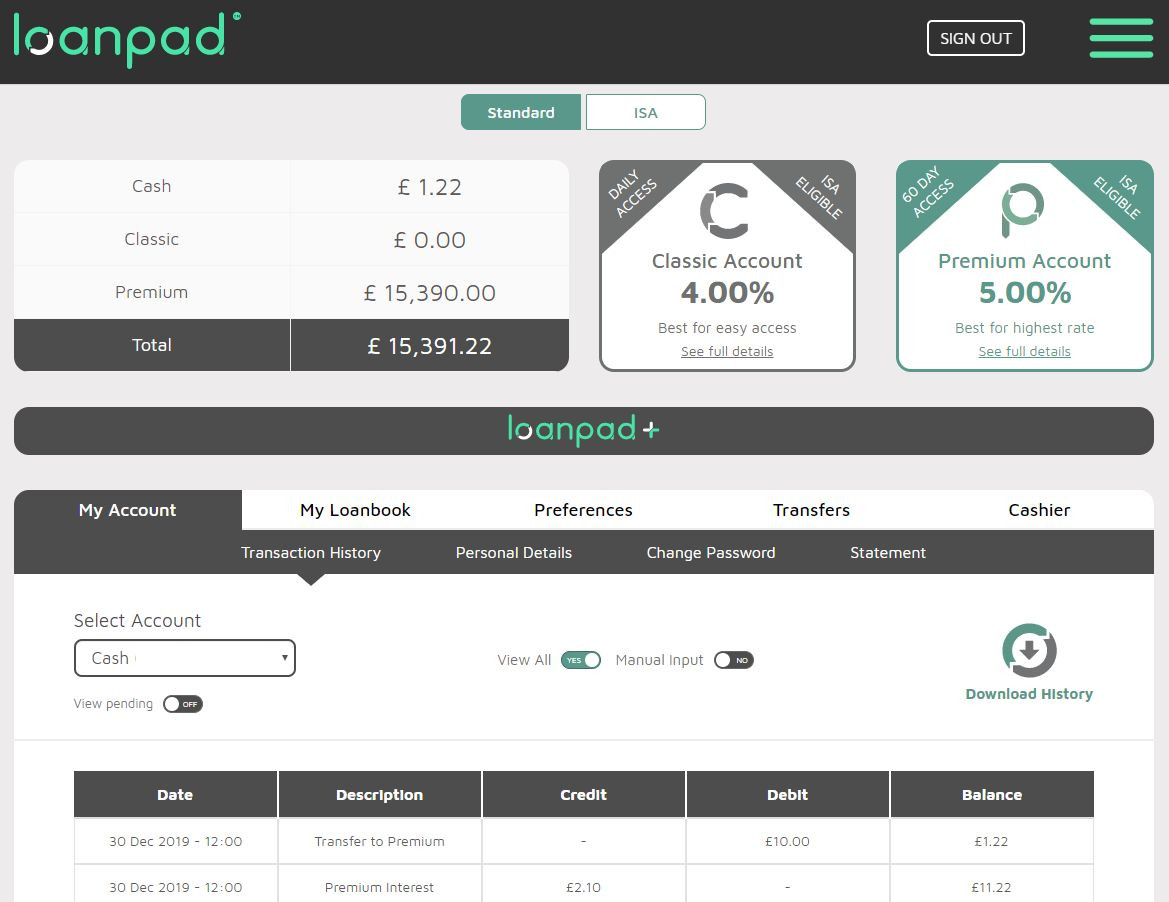

I sent over another £4k to Loanpad in December bringing to total up to the target £15k. You can see by the chart above that this had an immediate effect on income for the month.

Loanpad XIRR jumped in December to 6.14% from 5.86%. I can’t understand why it is so high on a 5% target rate, but I’m not complaining. I thought it might be cashback bonus or affiliate bonuses but I have taken them in to consideration as capital increase so that’s not it. The 5% target rate on the account is the actual rate you get, not taking in to consideration investing all of the returns for the effects of compounding. As opposed to the AER (Annual Equivalent Rate) given by most other lenders (both Peer to Peer and Banks/Building Societies) which estimates the rate based on all of the interest being invested back in to the account.

Loanpad Signup & Cashback Offers

Loanpad have a great cashback incentive if you’re thinking of joining:

£50 bonus if you invest into a lending account a minimum of £1,000 within 4 weeks post registration and keep this invested for 365 days.

£150 bonus if you invest into a lending account a minimum of £10,000 within 4 weeks post registration and keep this invested for 365 days.

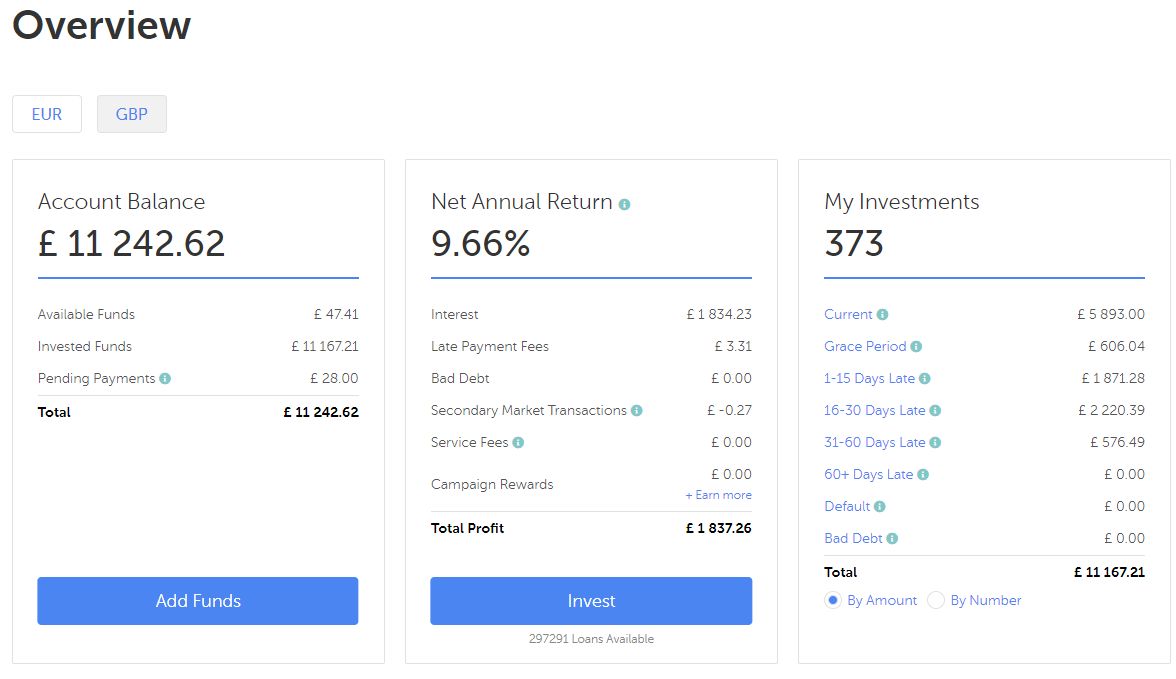

I’m still having to withdraw capital from Mintos because GBP MoGo car loans have gone away for good it appears. Unfortunately it looks like I’ll need to keep drawing it down without any more GBP loans available.

XIRR actually increased a bit again from 9.62% in November to 9.68% in December. Sad to have to withdraw GBP from Mintos, but on the bright side I still have an XIRR over 13% on Mintos Euro loans and the loan flow is much better there.

Unfortunately Mintos are still saying that UK residents can no longer invest in Mintos loans for now. Hopefully that will be ratified soon.

Mintos Signup & Cashback Offers

If you are NOT a UK resident, Mintos have a wonderful cashback bonus, one of the best in fact. Mintos offer 0.50% of the value of your investments cashback for the first 90 days you are investing with them!

In November RateSetter decided to drop rates. As of December 2nd, “Access” still pays 3%, but “Plus” has been lowered from 4% to 3.5% and “Max” has been lowered from 5% to 4%.

Mistake

I made a mistake with RateSetter by selling almost all of my loans instead of just the loans to take the account value down to £15k. I’m still not sure exactly what happened. Anyway it meant I was uninvested for most of December and thus my total return on RateSetter for December was a whopping £4.03 🙄

XIRR dropped in December to 5.13%. When I reinvested it got me back in at 4.3% so obviously that number will be a lot less next month.

RateSetter Signup & Cashback Offers

RateSetter is offering £20 cashback for investing £10 (woohoo! 🙄 ).

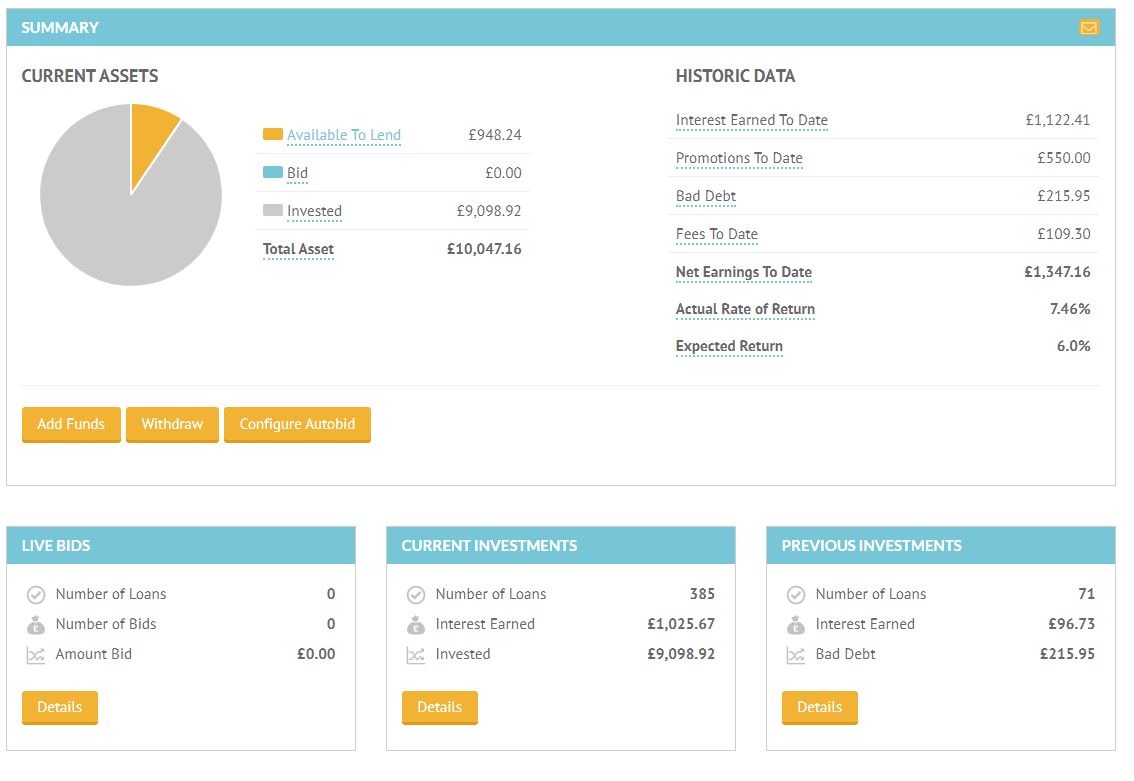

I sent over another £4,000 to Unbolted in November, but their loan flow has dropped a bit in December (probably because of the holidays) so I still have just under £1,000 that is not invested. Hopefully that will get gobbled up in January. As soon as it does, I’ll send over more money until I get the balance up to the target £15k.

XIRR down a little in December to 8.14% no doubt because of the cash drag. Still, 8%+ is nothing to sniff at, and the return has been immediately noticeable on the income chart above.

Unbolted are not like the big Peer to Peer platforms such as Funding Circle or RateSetter, and I like that. I like Unbolted’s spin on asset secured pawnshop style loans, and I certainly like the 8%+ return rates. When Unbolted loans default, assets are sold very, very quickly. Unbolted typically recover more than the item was worth. The average at the moment is 117% of the loan value is recovered! I regularly get emails saying that a defaulted asset has been sold and capital recovered, and the amount has been credited to my investment account. Zero losses in almost 2 years so far. See my Unbolted Review for more information on this unique lender.

One last thing that struck me about Unbolted over the last few weeks: in a recession, pawn shops typically do better than in a good economy. When people don’t have money, they often need to borrow money to get by. If banks won’t lend them money, an option is to lend money against personal assets. Basically Unbolted is high-tech pawn shop, so in theory they should do just fine in a recession, if not even better.

Unbolted Signup & Cashback Offers

Unbolted has a wonderful cashback bonus – £50 cashback if you invest just £1,000 by using the the link below!

Another great month for the Euro Portfolio with income of €537.56. Unfortunately that will change a bit next month as I withdrew €10,000 from Mintos to pay for new windows for the house in Portugal. I’m still waiting for the Euro to drop a bit before I buy more so using the Mintos Euros are a good option for now.

XIRR was up for the month to an overall 14.04% from 13.90% in November.

Still seeing great rates for lending Euros. I really do need to get some more Euros to lend out so I can also try some more lenders. I just wish they would come down a bit against the USD or GBP.

I’ve had a few people email me and ask about how I exchange money from GBP or USD to Euros and the best way to fund Euro Peer to Peer lenders, so I wrote a quick post on it here for anyone interested.

Crowdestor had a huge jump in income in December. This was due to a project I invested into in March called “Biomass Boiler House” which paid a balloon payment of €93.16 in December. With this project, for first 6 month interest payments were not paid but capitalized and paid in a bullet payment together with the Loan principal payment after the first 6 month period. Moving forward payments will be monthly. Payments on other projects were as normal.

XIRR also jumped from 13.39% in November to 16.08% in December because of the above payment.

Crowdestor Signup & Cashback Offers

No cashback offers from Crowdestor this month. Who needs cashback when you can average over 16% on your investments!

If you’re interested in giving Crowdestor a try, please

See All Account Data & Screenshots From My Envestio Account

Envestio income keeps on rising each month. There has been a bit of a panic on some of the Facebook groups and P2P websites about some of these high interest lenders. CEO’s changing and office addresses changing. Projects being fake and companies not being as they seemed. As far as I can tell though, no one has actually lost any money or not been paid yet, so I’ll wait until that happens before I start panicking. I really don’t pay a great deal of attention to it. In my eyes most of the Euro lenders I invest with have been in business for 2 or 3 years and they are out to build a business, not rip people off.

Investments paying upwards of 16% are inherently more risky, that’s why I don’t have €200k in them. It would be terrible to lose some of the money, but let’s give these companies a chance and see what they can do. I’m quite happy with Envestio so far, as I am with the other Euro lenders I’m with.

XIRR jumped from 16.84% in November to 17.08% in December. They say I’m getting with a 16.93% target rate so XIRR is very close and I’m totally happy with that..

Envestio Signup & Cashback Offers

Envestio have a €5 bonus for the first €100 deposit + 0.5% cashback from all investments for 270 days.

Grupeer seem to have moved away from the cash drag they were getting in November. I see all of my Euros have pretty much been invested all of December. Nothing more to say for Grupeer. Easy auto-invest with great returns.

XIRR up to a very reasonable 13.85% in December from 13.62% in November.

Grupeer Signup & Cashback Offers

No cashback offers from Grupeer at the moment.

If you’re interested in investing with Grupeer, please

Mintos short term loans are still hovering around 10%-11% unfortunately so that’s all I’m picking up. The lower rates are reflected in the XIRR which decreased a little again from 13.78% in November to 13.10% in December. This is still more than the Mintos target rate of 12.79%, and who can complain at almost 13% actual returns? Hopefully things will pick up soon and we’ll start seeing some of those 16% – 30 day loans again! I like those 😀

I withdrew €10,000 Euros to pay for some alterations I’m having done to the house in Portugal as I mentioned earlier in the overview. Once I get some more Euros changed, I’ll be putting some back with Mintos for sure.

Mintos Signup & Cashback Offers

Mintos have a wonderful cashback bonus, one of the best in fact. 0.50% of the value of your investments cashback for the first 90 days you are investing with them!

Robocash XIRR dropped a bit again from 12.62% in November to 12.36% in December. Still getting a little bit of cash drag here but it is still a bit better than the lender target rate of 12.00%, so no complaints here. Another easy auto-invest account which requires no maintenance at all.

Robocash Signup & Cashback Offers

No cashback offers with Robocash this month

If you’re planning on investing with Robocash, please

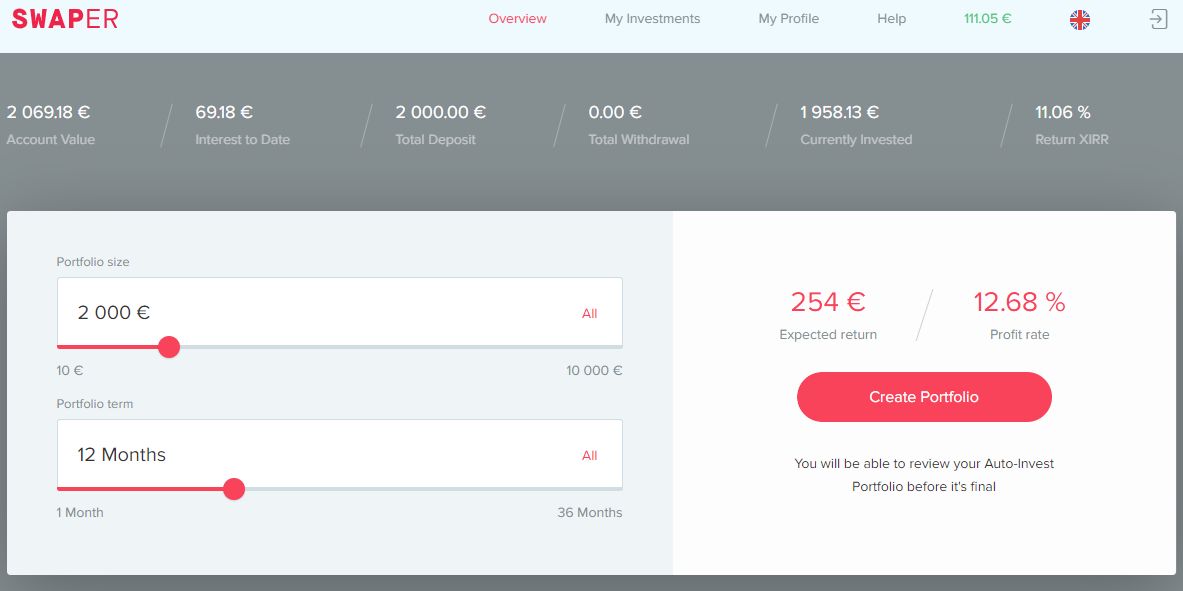

Swaper XIRR keeps creeping up slowly towards the lender provided target rate of 12%. XIRR rose once again from 10.21% in November to 10.71% in December. This should keep increasing moving forward as repayments are invested. I really need to get some more Euros invested with Swaper but I need to buy some first as I keep harping on about.

Swaper Signup & Cashback Offers

No current cashback offers.

If you’re interested in investing with Swaper please

Just a short update this month. Hopefully I was still able to get across what I’m doing and why for each account?

If you have any comments or suggestions, please comment on the post or email me, I’m always open to feedback!

You can always go back and look at the previous updates for more details on why I’m investing in these companies and my ongoing lending experiences with each of them.

Finally I hope the month of January goes well for everyone. I WISH YOU ALL A PROSPEROUS NEW YEAR FOR 2020! I will update you on my P2P Portfolio investments around the same time next month.

Thanks for reading my blog! Please feel free to comment below if you have comments, questions, criticisms or suggestions. You can also email me if you prefer. I love feedback!

Please note, most of the cashback offers on this site are for new lenders to a company. I suggest you do your own research before investing as cashback offers change daily.

This page is presented for informational purposes only. I am not a Financial Adviser and therefore not qualified to give financial advice. Please do your own research and make your own investment decisions. Do not make investment decisions based solely on the information presented on this website.

* My opinions, reviews, star ratings and risk ratings are based on my personal investing experience with the company being reviewed. These ratings are personal opinions and are subjective.

** Some of the links on this website are affiliate referral links. When you click on these links, I can sometimes receive a commission, at absolutely no cost to you. This helps me to continue to offer new reviews & monthly portfolio updates here on my website. I don’t receive commissions from all platforms and it has no effect on my ongoing opinions on investments & investment platforms. Income from my investments and capital preservation are my main motivations.

Platforms reviewed on this website I am currently investing with, or I have invested with in the past. You can see with full transparency on my Portfolio Returns page which assets & platforms I am invested with (or have previously been invested with) at any point in time. I am not paid a fee by any of the companies to write reviews, so the reviews are unbiased and purely based on my own personal experiences.

Please read my full website Disclaimerbefore making investment decisions.

4 thoughts on “P2P Lending Portfolio Update For December 2019”

Es

Interesting that you’ve decided to put an equal amount in all the platforms. Aren’t you tempted to vary the amounts to some extent depending on how safe you consider the platform to be?

Putting more into platforms “I” thought were safer had been my strategy for the last couple of years. Unfortunately it’s clear that things change and also I’m not always correct (perish the thought 🙂 ).

For example, when I started lending with Funding Circle, the first year (if you look back at my lending history with them) was great. Averaging around 7% income with great liquidity, meaning that loans could be sold in a couple of hours and cash withdrawn the same day. When FC went public, they were “rumored” to have relaxed their lending policy and made a bunch of “less than sensible” loans to boost their IPO price. This in turn led to the current situation where loans are defaulting, return rates have dropped drastically, and everyone wants out. Unfortunately no one can get out because the liquidity dried up. I’m not worried about FC in the long term as they are a huge company with lots of money, but I will likely be waiting until some of the loans come to term before I can get out of them all. So, currently £23k tied up for the next few years (worst case). I would have preferred that to be £15k or £10k if it had to be anything.

Based on this situation, along with the fact that all of my larger accounts reduced return rates drastically in December (reducing the risk/reward ratio), it made me review my investing rules. I decided to reduce my exposure to any single account. All of the accounts I invest with I consider to be at the safer end of the lending spectrum in my opinion (that’s “safer” not “safe”). Each of the platforms have their own “safety systems”, like RateSetter and Lending Works distributing risk between all investors, and having well funded provision funds. Loanpad, Kuflink, Unbolted, Lending Crowd, Assetz Capital and others having asset security with low LTV’s etc. However the fact is that we can’t always know what’s going on with a particular platform. So, the best strategy in my opinion is to diversify. With a smaller amount in each lender, not so much capital can be tied up if a lender goes belly up, or something changes. I say “tied up” because I’m not really worried about losing all of the capital in a particular platform as we are investing in individual loans, not platforms, and mostly we do have some asset security. So I would expect even in that event, I would get all or most of the capital back as loans came to term or assets were sold. The bankruptcies of Collateral, Lendy and Funding Secure recently have shown that when this happens, it gets very messy. So better in my mind to play defensively rather than have a lot of money exposed to any single platform, no matter how “safe” I think they are.

My overall investment strategy, whether P2P, Bonds, Stocks or Gold or other, always begins with diversification, so all I’m doing is sticking with that. It has served me well for the last 30+ years investing, so as they say “if it ain’t broken, why fix it?” 🙂

Yes, diversification is the number one rule, so decreasing the proportion of some makes sense; I’m just not sure I’d necessarily want to have the proportion exactly the same for all of them. Having said that, you’re obviously doing OK out of it! 🙂

I understand what you’re saying about not having the proportions exactly the same (you’ll notice my proportions are not exactly the same, yet either).

The question is; how do we decide what is the correct proportion for each lender? Again, look at FC. They are the largest UK lender and 2 years ago would have been classed as one of the safer and best just because of their size. So know one really knows. Obviously some companies are stronger than others, but things change over time. I’ll put into each lender what I feel comfortable with. It that makes all of the accounts the same, then that would work well.

Anyway, as you say, things have worked out OK so far, so we’ll see how that goes moving forward 🙂

The Obvious Investor website uses cookies to offer you the best possible browsing experience. By browsing this site, you give us the ok to use cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

_abck

1 year

This cookie is used to detect and defend when a client attempt to replay a cookie.This cookie manages the interaction with online bots and takes the appropriate actions.

bm_sz

4 hours

This cookie is set by the provider Akamai Bot Manager. This cookie is used to manage the interaction with the online bots. It also helps in fraud preventions

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_gat_gtag_UA_127056176_1

1 minute

This cookie is set by Google and is used to distinguish users.

_gat_UA-127056176-1

1 minute

This is a pattern type cookie set by Google Analytics, where the pattern element on the name contains the unique identity number of the account or website it relates to. It appears to be a variation of the _gat cookie which is used to limit the amount of data recorded by Google on high traffic volume websites.

_gcl_au

3 months

Provided by Google Tag Manager to experiment advertisement efficiency of websites using their services.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

NID

6 months

NID cookie, set by Google, is used for advertising purposes; to limit the number of times the user sees an ad, to mute unwanted ads, and to measure the effectiveness of ads.

Interesting that you’ve decided to put an equal amount in all the platforms. Aren’t you tempted to vary the amounts to some extent depending on how safe you consider the platform to be?

Hi,

Putting more into platforms “I” thought were safer had been my strategy for the last couple of years. Unfortunately it’s clear that things change and also I’m not always correct (perish the thought 🙂 ).

For example, when I started lending with Funding Circle, the first year (if you look back at my lending history with them) was great. Averaging around 7% income with great liquidity, meaning that loans could be sold in a couple of hours and cash withdrawn the same day. When FC went public, they were “rumored” to have relaxed their lending policy and made a bunch of “less than sensible” loans to boost their IPO price. This in turn led to the current situation where loans are defaulting, return rates have dropped drastically, and everyone wants out. Unfortunately no one can get out because the liquidity dried up. I’m not worried about FC in the long term as they are a huge company with lots of money, but I will likely be waiting until some of the loans come to term before I can get out of them all. So, currently £23k tied up for the next few years (worst case). I would have preferred that to be £15k or £10k if it had to be anything.

Based on this situation, along with the fact that all of my larger accounts reduced return rates drastically in December (reducing the risk/reward ratio), it made me review my investing rules. I decided to reduce my exposure to any single account. All of the accounts I invest with I consider to be at the safer end of the lending spectrum in my opinion (that’s “safer” not “safe”). Each of the platforms have their own “safety systems”, like RateSetter and Lending Works distributing risk between all investors, and having well funded provision funds. Loanpad, Kuflink, Unbolted, Lending Crowd, Assetz Capital and others having asset security with low LTV’s etc. However the fact is that we can’t always know what’s going on with a particular platform. So, the best strategy in my opinion is to diversify. With a smaller amount in each lender, not so much capital can be tied up if a lender goes belly up, or something changes. I say “tied up” because I’m not really worried about losing all of the capital in a particular platform as we are investing in individual loans, not platforms, and mostly we do have some asset security. So I would expect even in that event, I would get all or most of the capital back as loans came to term or assets were sold. The bankruptcies of Collateral, Lendy and Funding Secure recently have shown that when this happens, it gets very messy. So better in my mind to play defensively rather than have a lot of money exposed to any single platform, no matter how “safe” I think they are.

My overall investment strategy, whether P2P, Bonds, Stocks or Gold or other, always begins with diversification, so all I’m doing is sticking with that. It has served me well for the last 30+ years investing, so as they say “if it ain’t broken, why fix it?” 🙂

Hope that makes sense.

Yes, diversification is the number one rule, so decreasing the proportion of some makes sense; I’m just not sure I’d necessarily want to have the proportion exactly the same for all of them. Having said that, you’re obviously doing OK out of it! 🙂

I understand what you’re saying about not having the proportions exactly the same (you’ll notice my proportions are not exactly the same, yet either).

The question is; how do we decide what is the correct proportion for each lender? Again, look at FC. They are the largest UK lender and 2 years ago would have been classed as one of the safer and best just because of their size. So know one really knows. Obviously some companies are stronger than others, but things change over time. I’ll put into each lender what I feel comfortable with. It that makes all of the accounts the same, then that would work well.

Anyway, as you say, things have worked out OK so far, so we’ll see how that goes moving forward 🙂