April 2021 was a good month for my investments. I increased my P2P lending investment significantly, & added a couple of new Peer to Peer platforms to the Peer to Peer Lending Portfolio.

More PolkdaDOT was added to the Crypto Portfolio when prices dipped towards the end of April. I also staked all of the DOT, and ADA as staking seems to be paying off.

So with that in mind, let’s get right in to it with the detailed Peer to Peer lending update first.

Peer to Peer Lending Sites & Portfolio Update

Peer to Peer lending investment increased significantly in April from £122k at the and of March to over £185k invested by the end of April.

I added a new lender (easyMoney) which I’ll discuss below. I also withdrew capital from Lending Works & Unbolted due to cash drag. Can’t have money sat there for months making nothing.

The information below is comprised of my opinions on current investment market conditions and my personal actions with my investments. It should not in any way be construed as financial advice. Please do your own research before making investment decisions and do not base them solely on what you read on this website. Please read my full disclaimer of more information.

Some of the links on this website are affiliate referral links. For cashback offers, you’ll generally need to use these links to qualify for the cashback. If you use these links I can sometimes receive a commission, at absolutely no cost to you. This helps me to run the website, write new platform reviews, publish monthly portfolio updates & generally keep me interested in taking the time to share the information you are currently reading. I don’t receive commissions from all platforms, and it has no effect on my ongoing opinions on platforms, which are entirely focused on generating Income from my investments and preserving capital.

No change in my Ablrate investments this month. Nothing really changed there so I’m just watching what happens for the time being. Ablerate brought a couple of new loans online in April which is promising.

Here’s a recap of the current situation:

I drew down many of my loans with Ablrate as I was not sure how they would fair throughout the pandemic. My current investment balance is quite low and I’m not sure if I’ll increase it anytime soon. The main reasons being the work involved to invest in Ablrate loans & the late loans they currently have.

Ablrate still look to have about about 25% of their loans late or in default, but hopefully that will come down as things get back to normal with the economy.

Ablrate still seem to be a strong platform with great returns available if you’re willing to put in the work. They are still recovering from the pandemic hit but surviving and hopefully getting back to a normal default level soon.

Here is a view of my Ablrate account as it stands at the end of April 2021.

My current Ablrate Investments (as you can see, still only 1 late currently)

My Ablrate Strategy.

There are some great returns available through Ablrate if you’re willing to put the time in to do the research and buy the best loans. Up to 15% per annum. One of the best rates of all UK Peer to Peer lending sites.

For some it will be totally worth the effort. For me with my “Lazy Investor” attitude, the time commitment required exceeds my enthusiasm at the moment. That may change in the next few weeks, but for now I don’t have the time to diversify a significant amount of capital in the way I would like.

If you do have the time to spare, Ablrate are one of the best paying lenders out there as far as returns go. The fact that they are still around after the pandemic also has to say something about their business model and the saftey of the platform.

Ablrate Signup & Cashback Offers

£50 Ablrate Cashback on £1000+ investment for New Investors

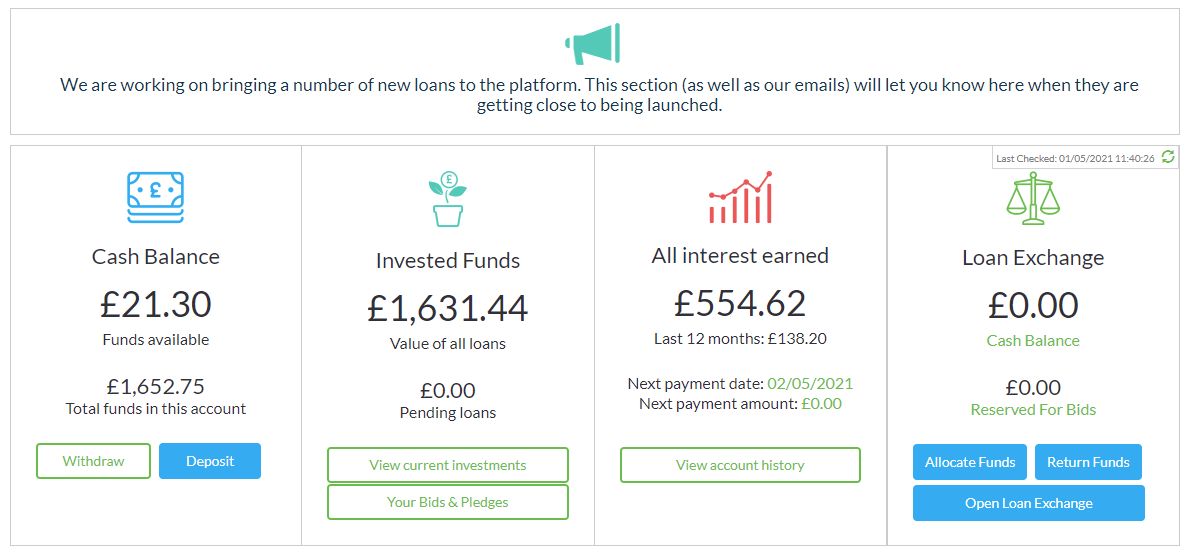

Assetz Capital seem to be pretty much back to normal now. I haven’t seen any discounts available for investment in to their Access Accounts in April, which means liquidity must be getting back to normal. As normal as it’s going to get for the foreseeable future anyway.

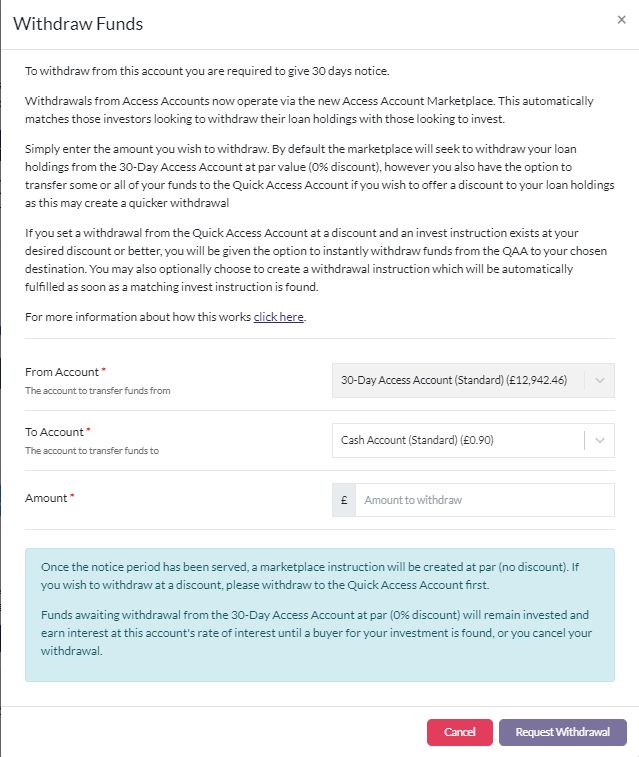

During the pandemic, Assetz implemented a discounting system for the Access Accounts enabling investors who needed their capital out “now” to offer a discount in order to do so. You can read more about how it works on Assetz Capital’s website here. It seems as though this new system is here to stay and I’m not sure that’s a bad thing. Under normal market conditions, there should be plenty of incoming capital to fulfill withdrawal requests. Under less than ideal situations, the discount capability is there. An added benefit for people in the notice accounts (30 & 60 day) is that in the event of an emergency, they can still offer a discount and get out faster if need be.

Here’s a screenshot of the 30 Day Access Account withdrawal screenshot:

So if you want to give a larger discount, you can get out faster than the 30 days providing there is someone looking to invest at the discount level you’re looking for.

Here’s what my Assetz Capital account looks like now:

My Assetz Capital Strategy.

I started to increase my investment in Assetz Capital once things started to look like they were getting back to normality. Right now I’m a little over £18k invested with them and I’ll probably increase more as things get back to baseline normal.

I like Assetz, they were my biggest P2P investment account at one point, but when the pandemic hit and the liquidity squeeze came on, I think it surprised everyone (including me). Assetz Capital are still here after the pandemic, and I can see they are much stronger for the experience.

CrowdProperty brought several new loans to the platform in April. I invested in almost all of them accept for a couple which I missed as I wasn’t in front of my computer for the 10 seconds it took to fill them.

This platform has so much money on it looking for investment right now, you have to be fast.

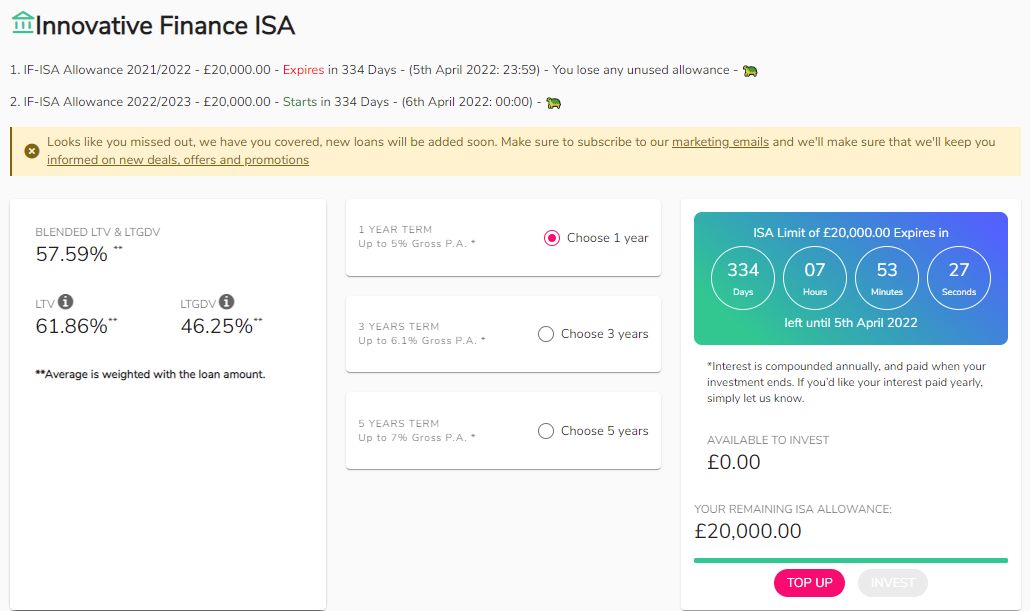

I increased capital with CrowdProperty by opening an IFISA with them as I had allowance left from 2020. IFISA investment with CrowdProperty is pretty much the same as with the regular manual investment, you just need to specify the funds should come from your IFISA when placing the pledge.

Because of the IFISA investment, I withdrew some un-invested capital from my regular account which would be at the back of the IFISA investment queue. Once I use up the IFISA capital I’ll begin to increase in the regular account again.

Other than that, no changes for April.

CrowdProperty offer property secured development loans, all with first legal charge and reasonable LTV’s. I continue to feel like the loans they have written are well vetted, and are some of the safer development loans available in the P2P market. In fact they all but proved this by the way their business prospered throughout the pandemic.

Here’s a screenshot of my CrowdProperty account at the end of April 2021.

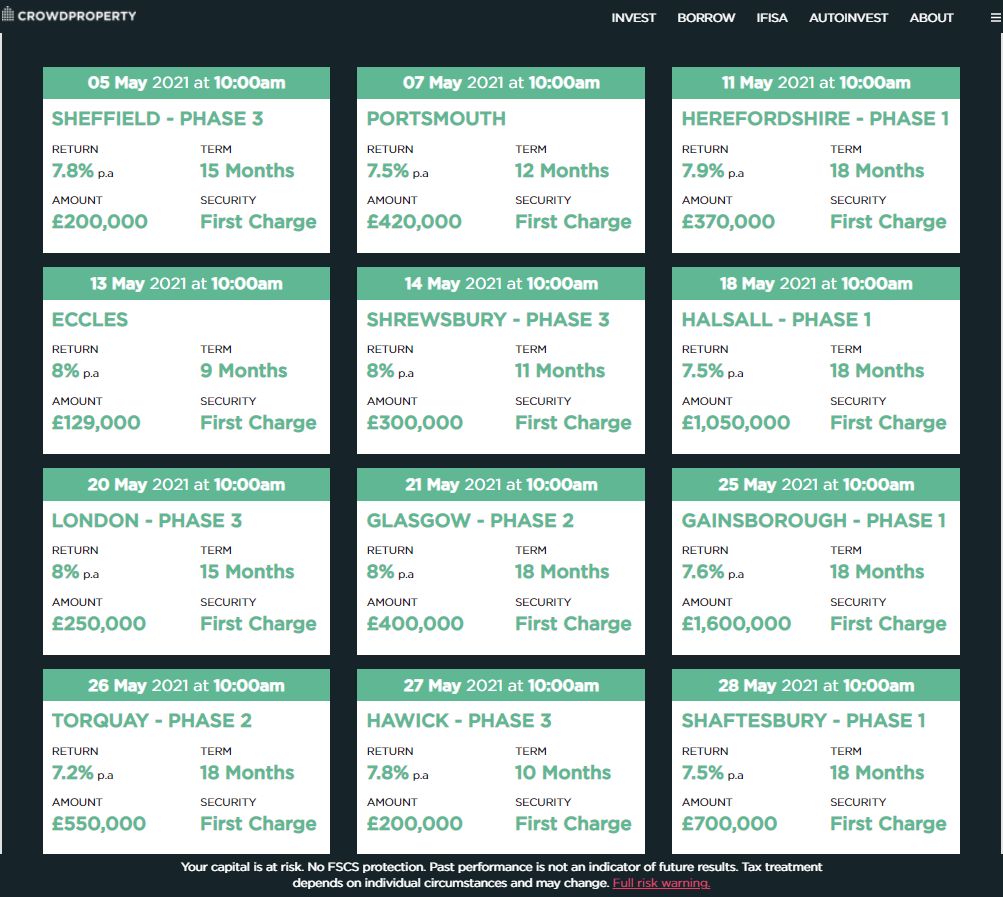

Here are some of the loans coming in May 2021

My CrowdProperty Strategy.

My strategy since the beginning with CrowdProperty is to invest £500 into almost every loan they have. If the LTV is low, and it’s a tranche 1, I’ll invest £1000. I do a little due diligence on each loan before it goes live. Once in a while I see something I don’t like the look of and I don’t invest in that particular loan. I’ll often look closely at higher level (numbers) tranches and pass over some of them at times. Overall though, that happens very infrequently so it’s pretty much £500 or £1000 into each loan.

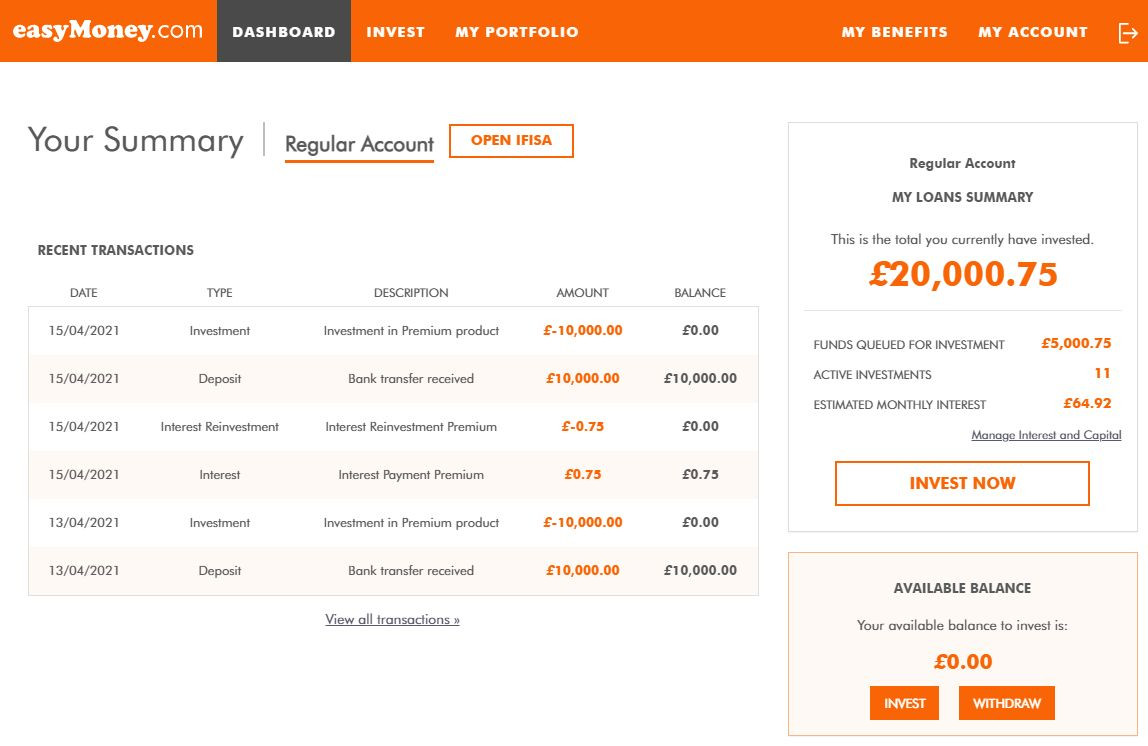

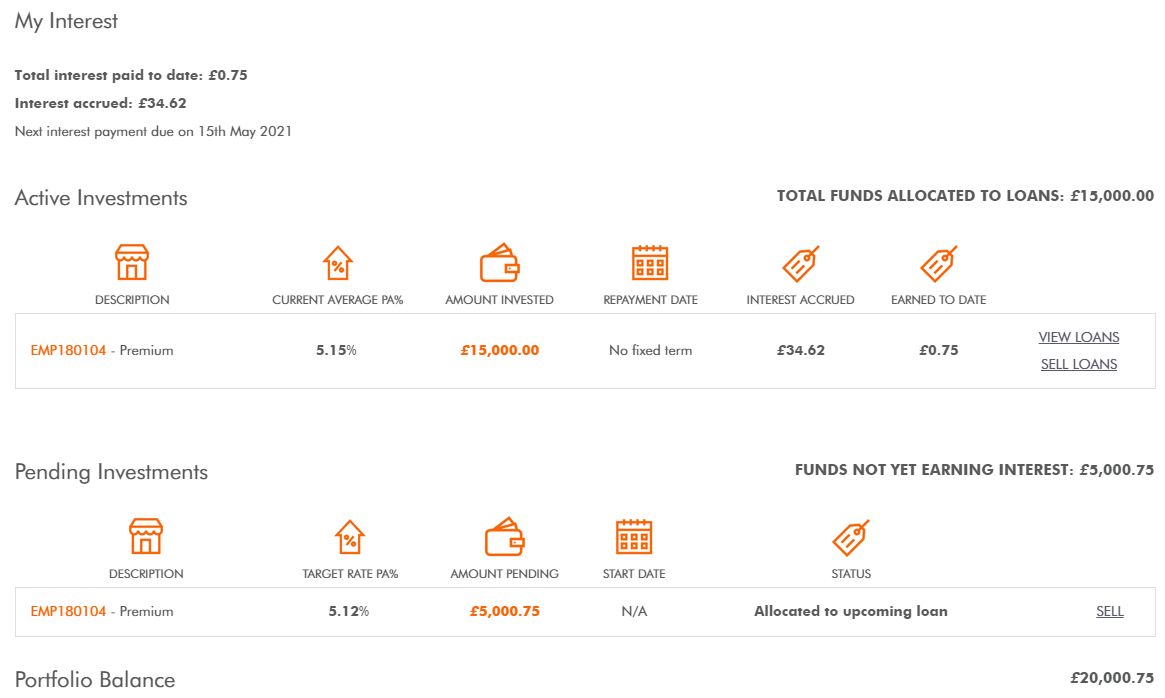

easyMoney was another new investment for me in April. As the name suggests; they are part of the “Easy” family of brands (EasyJet, EasyHotel, EasyCar etc.), however to be clear, this is just branding which they pay a fee for. They are their own entity and not backed financially at all by the other “Easy” companies. As such, I look at them as a stand alone platform.

easyMoney were founded in 2018 and since then have an impeccable history of zero defaults. They are very particular in the loans they choose to finance, which are typically short term property purchase & development loans from 3 to 12 months in length. They are very similar to CrowdProperty & Kuflink, except the only option with easyMoney is auto-invest. They diversify your investment capital for you between available loans.

I looked at easyMoney several times in the last few years. Although they seemed credible enough & had a decent reputation, the rates they offered always seemed quite low compared to other, similar lenders. After the pandemic though, with many platforms reducing rates, easyMoney rates are starting to come inline & make the risk/reward look attractive. The fact that the pandemic didn’t seem to phase them also caught my attention.

I initially invested £10k and it was invested quite quickly. Diversification is not as I would ideally like (11 loans), but because the platform is auto-invest only, there is not much I can do about it, and because of the quality of the loans, I’m fairly comfortable with it.

A couple of days later I decided the 6.06% on the Premium Plus account was the “sweet spot” for returns. To get any higher I would need to invest over £100k which is too much for one (newer) platform. I sent over another £10k to take me to that 6.06% level and that’s where it will stay for now.

The only thing I’m not really happy about is that £5k that is yet to be invested. I believe that’s because they have a limit on percentage of investment per loan (or possibly all investments are currently filled and no one is looking to withdraw). As it’s only been a couple of weeks, I’ll keep an eye on it and see how it goes.

Here’s a screenshot of the easyMoney Dashboard

You may have noticed the rate currently says 5.12%. That’s because rates are adjusted & interest paid on the 15th of each month, therefore I just missed the higher rate in April so I’ll need to wait until the 15th of May.

Nothing new with Funding Circle in April. I withdrew £700 which had been paid back.

Here is how my Funding Circle account looks now (the 3.1% returns indicated is misleading, that’s assuming no more defaults & reinvestment of capital. Neither of which is going to happen).

My Funding Circle Strategy.

I’ve been drawing down my Funding Circle account since July 1st 2019 – trying to sell out and get my capital back after events that unfolded in 2019. You can read more about it in the Funding Circle Review Funding Circle still have no liquidity, and all I’m doing is receiving monthly loan repayments as loans are paid back. I will not be investing new capital with Funding Circle for the foreseeable future. Never say never though. Maybe they’ll get back to lending as they used to one day.

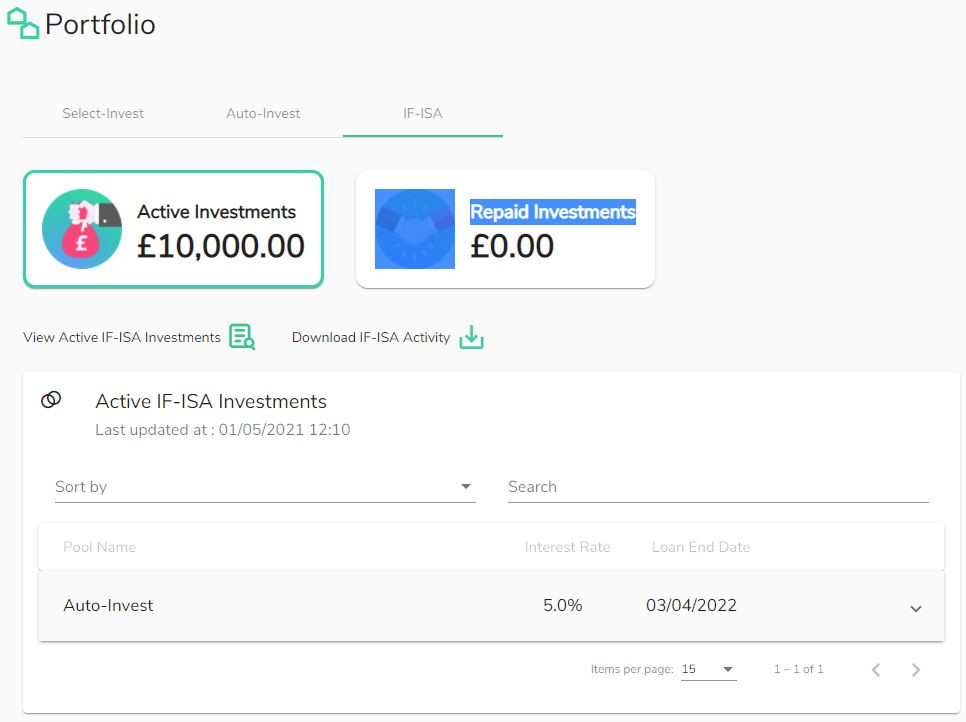

I increased my investment with Kuflink again in April by opening a IFISA with them and also adding capital to my Select Invest Account.

Only auto-invest is available with IFISA’s through Kuflink so I had to choose between 3 options. 1 year of investment at 5%, 3 years at 6.1% and 5 years at 7%.

I decided this time I would go with £10k the 1 year at 5%. Reason being, not quite everything is back to normal in the UK economy yet so I want to see what happens in the next 12 months before I commit to a longer period and higher rate. Also as most loans are 12-18 months with Kuflink, I always look at it as a mid-term platform and I’m comfortable with that for now.

Kuflink are still bringing plenty of Self Select loans on board as well so I have kept investing chunks of capital in new deals there.

Several loans also paid back in April, so I have a little capital sat waiting for more loans to come up.

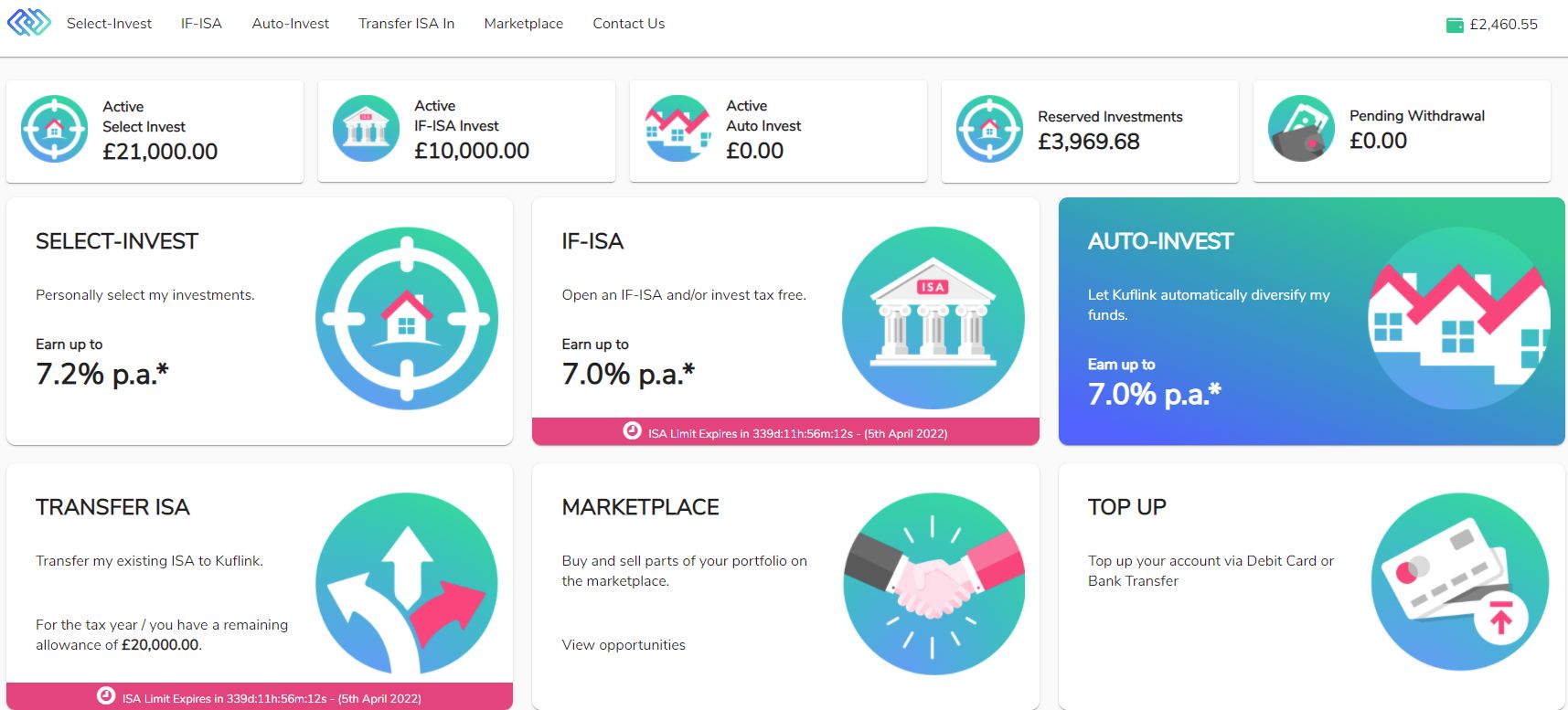

Here is a snapshot of my Kuflink account

£21k active investments, almost £4k reserved and £10k IFISA with £2.5k sat in cash waiting for more loans.

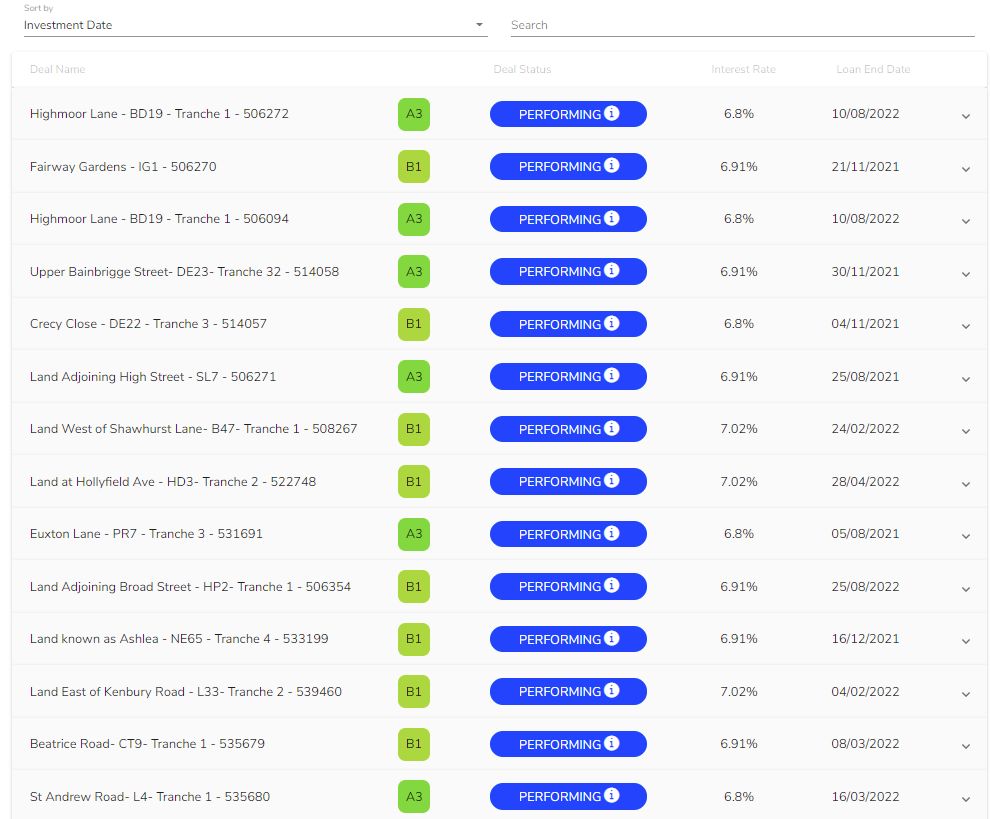

Here are all of the self select loans I have invested in (click to enlarge). You’ll note all are performing. Kuflink does have some loans that are in default but luckily I didn’t get caught in any of those. I think they are mainly from before the crisis and most will get current in the next few months I would think. If not the property will be sold and investors capital returned (eventually. Can take a while).

You’ll note I’m in multiple tranches of some loans & I’m ok with that. Sometimes I look at a loan and decide I want more money in it at a higher rate (and a little more risk of course) so I take positions in later tranches.

My Kuflink Strategy.

I continue to invest £500 in to almost every loan Kuflink brings with an LTV over 50%. For loans with LTV’s under 50% & first legal charge (& usually tranche 1), I invest £1000. As with CrowdProperty I do a little due diligence and if I see something I don’t like, then I don’t invest. That does not happen often though as Kuflink do great due diligence themselves, so it’s pretty much £500 or £1000 into every loan.

Kuflink Signup & Cashback Offers

New Kuflink customers receive the following Kuflink cashback on an investment of £1000 or more when they use signup links from obviousinvestor.com. Must invest into loans within 14 days of first investment to qualify for cashback.

No changes. Just withdrew a little capital which was paid back.

Recap:

I decided to retrieve capital (where possible) from lenders who have unsecured loans to reduce my overall exposure to Peer to Peer lending when the pandemic hit. Although LendingCrowd do have some secured loans, many just have directors personal guarantees. Historically, trying to recover from just these personal guarantees has been hit and miss. So, I made an early decision to withdraw my capital.

I was able to sell about 75% of the loans as I was early to start selling in March 2020.

Repayments have still been coming in slowly for the last year and LendingCrowd are currently lending only through the UK government backed CBILS scheme and as such are not accepting new capital from retail investors. Hopefully when things get back to some form of normality, LendingCrowd will open its doors to retail investors again.

Here is a screenshot of how my account looks currently

My LendingCrowd Strategy.

As mentioned previously; LendingCrowd are currently lending only through the UK government backed CBILS scheme and as such are not accepting new capital from retail investors.

As soon as they start accepting investments again, I’ll make a decision on if & when to increase my investment again with LendingCrowd.

I had decided to give Lending Works another try in February when I deposited £10k with them to see how they do. They had huge liquidity problems throughout the pandemic and also made some bad decisions on how they handled customers investments. Even so, they seemed to be coming back to normal so I thought I would give them another shot.

Unfortunately though by the end of April, still none of the £10k I invested had been lent out (still on offer). So, enough is enough, I withdrew it and put it elsewhere so I can make some returns.

I have no idea what will happen with Lending Works now but I’ve lost interest in them. Offering 4% with a 3 month or more wait to get invested is not going to do it with me. I realize they have a lot of fund investments now but if they’re still going to offer retail investment, they should lend the capital out quickly when investors decide to invest.

Maybe I’ll revisit at a later date, or maybe I won’t.

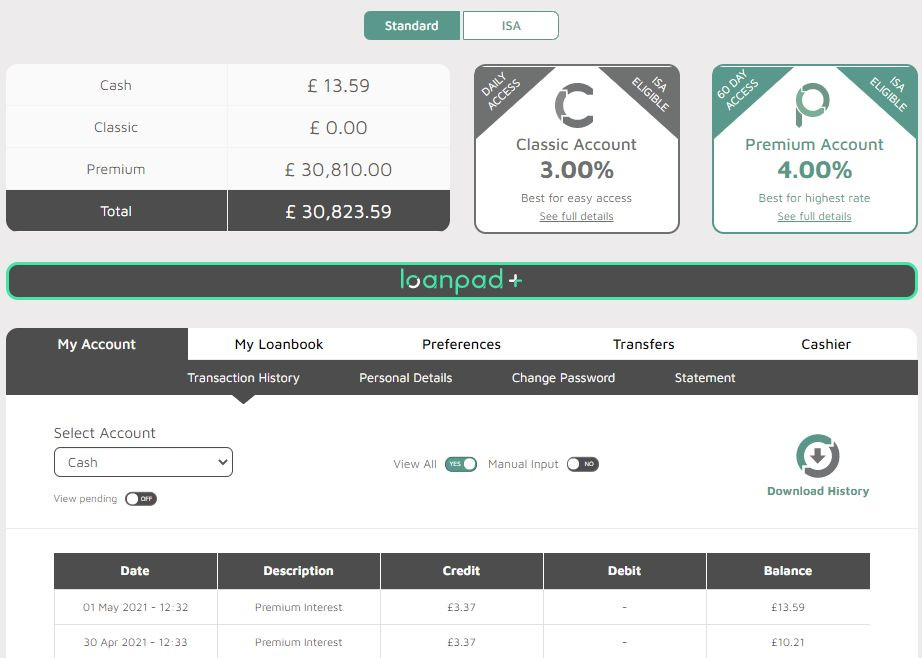

I decided to open an IFISA with Loanpad (for 2020/2021). I did the whole £20k with them as I couldn’t decide where else to put it and I consider Loanpad as just about the safest lender out there currently. Now, as my CrowdProperty funds get invested, I may decide to move some of that there as the higher returns are good for IFISA investment. For now it’s fine with Loanpad though and I like to see my daily interest come in and get reinvested.

Here is a screenshot of how my account looked at the end of April 2021

My Loanpad Strategy.

As mentioned above, I’ve continued to increase my investment with Loanpad substantially. Already in April I’m at £50k and (for now at least) that’s enough for a single lender. The great thing about Loanpad is; it’s a completely hands-off investment. Set up the auto-invest and everything just works like clockwork. No need to do anything after that.

I realize the amount I have invested with Loanpad is higher than I would normally allow with my diversification rules. However because of their low LTV loans, and the fact that they came through the pandemic virtually unscathed. I’m perfectly comfortable with my investment in this case. Now, as I find new lenders that perhaps pay a little more income for a reasonable risk, I may diversify some of this capital into other platforms.

Loanpad Cashback Offers

£50 bonus if you invest into a lending account a minimum of £5,000 within 4 weeks post registration and keep it invested for 1 year

£100 bonus if you invest into a lending account a minimum of £10,000 within 4 weeks post registration and keep this invested for 1 year.

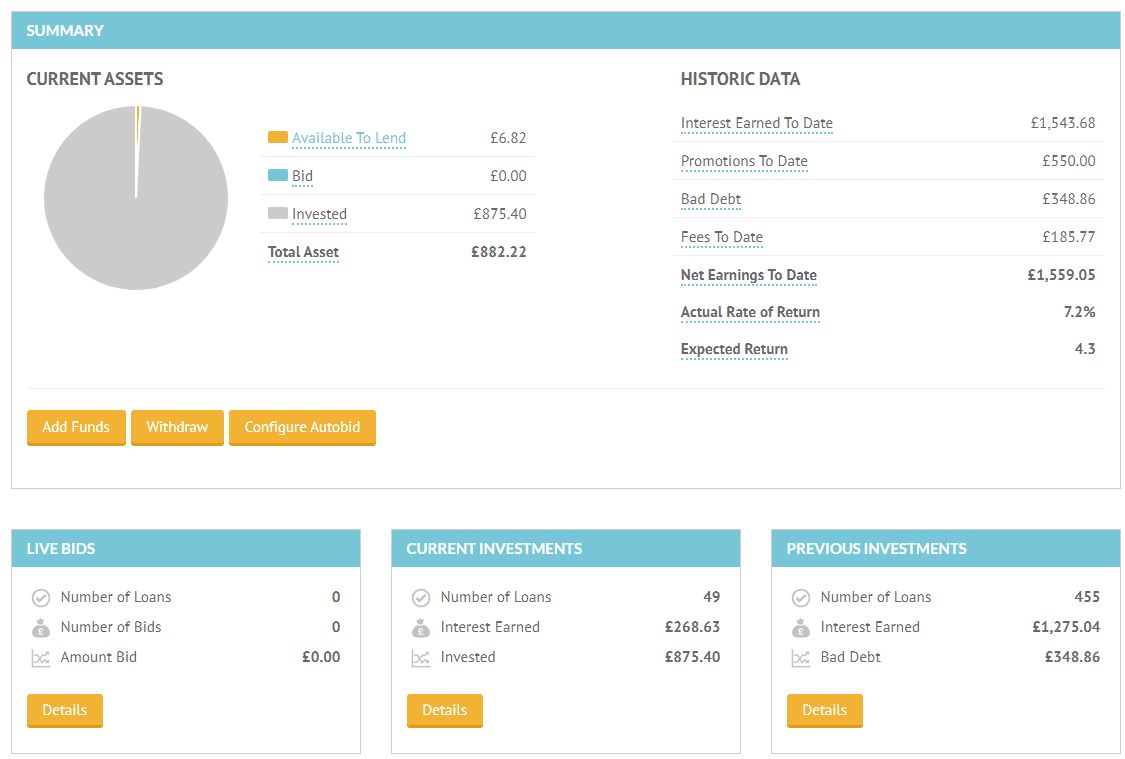

I had to withdraw £5k from Unbolted in April. It had been sat there for a couple of months & I couldn’t see any way to get it invested.

Unbolted are a great lender and I love the fact that they are not real estate property loans. Just something different to diversify in to & they have a great track record.

In case you’re unfamiliar; Unbolted offer pawnshop style loans to the general public with very liquid assets. These types of assets can be sold very quickly upon default so the demand for Unbolted loans exceeds the available loans.

I have been lending with Unbolted for a few years now, and although there have been many defaults, assets have always sold at more than the outstanding loan principle and I have always been paid back both principle and interest very quickly. Loans are short to medium term in nature so a complete exit can be had by turning off auto-invest within 3 to 12 months.

Unfortunately getting capital invested has become difficult because they have so few loans now, and too many investors with a lot of capital waiting to get in.

Here’s a screenshot of my account as it stands at the end of April, 2021.

Here are some of the recent loans capital has been put into by auto-invest. You can see even with a £5k cash balance, I’m still only getting £5 or £10 at a time. That’s going to take a LONG time to lend out £5k with just a couple of loans per day.

My Unbolted Strategy.

I would happily invest more capital with Unbolted if I could get it invested without the cash drag. I really love the platform and I’ve been lending with them for a long time now.

I’ll keep an eye on them and as soon as capital starts to get invested quicker, I will increase investment in Unbolted by a significant number. The question is; when will this happen of course.

I have been drawing down my Euro investments slowly as because I live in Portugal some of the time, when I’m here I live on Euros. So I have been using the Euros that I have invested in Euro Lenders for living expenses.

Typically I would change US Dollars or GB Pounds for Euros, but the Euro has been rising rapidly recently against the USD, and the GBP has still not recovered fully from Brexit. So I decided to use the Euros I have before changing more at this high rate in the hope it comes back down soon.

If you have Euros to invest and are looking for ideas. There are a few Euro Lenders that have come through the pandemic and seem to have been largely unaffected, namely Crowdestor, Swaper, Peerberry & Robocash have all done what they are supposed to do. I will invest in these all again once I am ready to invest Euros again. I believe they are all decent investable companies paying very good returns. Mintos is also worth investing in as long as you realize you’re not investing in Mintos, you’re investing in their LO’s, and as such you should pay more attention to them than to the platform.

No changes from last month. Everything performing as expected.

Recap:

My main Growth Portfolio is doing as expected. REITs took a tumble at the beginning of the pandemic. Actually all assets got hit initially as panic set in, but REITs got hit the hardest losing around 50% of their value in a few weeks. Crazy stuff! That’s what panic does for us.

As always happens, the “safe haven” assets (Bonds & Gold) picked up the slack and started to rally just as they always do when the “big money” (funds) start to move capital into those assets as a safety hedge. The portfolio performed admirably throughout the pandemic after the initial “shock drawdown”.

If you look at the other portfolios based on Harry Browne’s Permeant Portfolio, you’ll see that this Growth Portfolio beats them hands down with just the addition of the REITs. Although all of the Permanent Portfolio assets did as expected.

You may have noticed that the returns numbers have increased significantly for this portfolio. That’s because before I was using inflation adjusted data. I decided to stop that as the data is difficult to correlate so now it just the raw numbers. If you need to know how that looks historically against inflation, you’ll need to do some number crunching yourself 🙂

No changes from last month. Everything performing as expected.

Portfolios based on Harry Browne’s Permanent Portfolio strategy are all still doing well and as expected. They all experienced some drawdown when the pandemic first hit, but nothing out of the ordinary. 7% – 12% drawdowns with these portfolios are a regular occurrence.

None of them perform as well as the USD Growth Portfolio because the portfolios that are not in USD currency are not based on the US markets (historically some of the worlds top performing markets), plus they don’t have the added exposure to REITs and the high dividends they bring. The only difference between the USD Growth Portfolio & the USD Permanent Portfolio are the REITs, so you can see by looking at that the difference they make over time.

Our newest portfolio is still doing exactly as we hoped. I haven’t had chance to put together a tracking spreadsheet yet, but we can see using Portfolio Visualizer pretty much how we’re doing. If you Click here you can see the live test for yourself. Just to give you a quick overview though;

You can see below where we were in January (this image from the original post)

And this is where we are currently (end of April 2021)

As you can see from the charts, all sectors are returning to their average growth lines as expected. The portfolio is almost back to normal levels, which was the whole point of trying to catch the move in the first place as you can read in the original post from back in January).

The question will be of course when it gets all the way back, will I balance the portfolio out with bonds and other assets, keep it as is, or sell it and take a profit? 🤔 This portfolio under normal circumstances is very aggressive and could be subject to large drawdowns in the future, so I’ll need to make a decision when the target is hit.

Toward the end of April, PolkaDOT had a pullback. I decided to put a buy order in for another 250 at £20 which was filled on April 25th. I did what all good speculators do, when an asset pulls back and everyone else is selling, (assuming you still believe in it) buy more!

The other reason I invested more is “Crypo Staking”. Remember last month I briefly discussed how you can “Stake” your Crypto assets to the network, and they pay you a percentage every couple of weeks (PolkaDOT pays 12% per annum).

I tried it and indeed, I am paid in DOT every week! 12% per annum. I still consider Crypto to be a highly volatile investment, but if they’re paying me 12% just to have it there, then I’m willing to invest a bit more. I have a total of £14,840 I invested in DOT now for a total of 650 units at various prices. I’ve already been paid 3.32 units just for staking it. I’m also fairly happy that my overall investment is up 21%+ in the last few months.

You may have also noticed in the above screenshot that Kraken just started allowing ADA to be staked. So I staked that too! Why not?

The thing I have to remind myself with this portfolio is that it wasn’t made as a growth portfolio as such, but a “punt portfolio” as outlined in the original blog post back in March. I’m getting more comfortable with Crypto though, but it’s still a really volatile investment category.

Summary

That’s all for this update. I’ll continue to watch the markets (with one eye, sometimes, in between naps & being jumped on by my 1 year old son) and provide and update in a month or so.

Good luck with your investments in the coming months! Remember, it’s about patience & persistence, not perfection!

My best to you and your families. Stay safe and I’ll post an investment update again soon.

This page is presented for informational purposes only. I am not a Financial Adviser and therefore not qualified to give financial advice. Please do your own research and make your own investment decisions. Do not make investment decisions based solely on the information presented on this website.

* My opinions, reviews, star ratings and risk ratings are based on my personal investing experience with the company being reviewed. These ratings are personal opinions and are subjective.

** Some of the links on this website are affiliate referral links. When you click on these links, I can sometimes receive a commission, at absolutely no cost to you. This helps me to continue to offer new reviews & monthly portfolio updates here on my website. I don’t receive commissions from all platforms and it has no effect on my ongoing opinions on investments & investment platforms. Income from my investments and capital preservation are my main motivations.

Platforms reviewed on this website I am currently investing with, or I have invested with in the past. You can see with full transparency on my Portfolio Returns page which assets & platforms I am invested with (or have previously been invested with) at any point in time. I am not paid a fee by any of the companies to write reviews, so the reviews are unbiased and purely based on my own personal experiences.

Please read my full website Disclaimerbefore making investment decisions.

1 thought on “Investment Portfolios Update, May 2021”

Paul Bagworth

Just found your site via Assetz Exchange monthly news letter and realy enjoyed reading it being a big fan of p2p investing.

The Obvious Investor website uses cookies to offer you the best possible browsing experience. By browsing this site, you give us the ok to use cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

_abck

1 year

This cookie is used to detect and defend when a client attempt to replay a cookie.This cookie manages the interaction with online bots and takes the appropriate actions.

bm_sz

4 hours

This cookie is set by the provider Akamai Bot Manager. This cookie is used to manage the interaction with the online bots. It also helps in fraud preventions

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_gat_gtag_UA_127056176_1

1 minute

This cookie is set by Google and is used to distinguish users.

_gat_UA-127056176-1

1 minute

This is a pattern type cookie set by Google Analytics, where the pattern element on the name contains the unique identity number of the account or website it relates to. It appears to be a variation of the _gat cookie which is used to limit the amount of data recorded by Google on high traffic volume websites.

_gcl_au

3 months

Provided by Google Tag Manager to experiment advertisement efficiency of websites using their services.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

NID

6 months

NID cookie, set by Google, is used for advertising purposes; to limit the number of times the user sees an ad, to mute unwanted ads, and to measure the effectiveness of ads.

{kind=link}

Just found your site via Assetz Exchange monthly news letter and realy enjoyed reading it being a big fan of p2p investing.