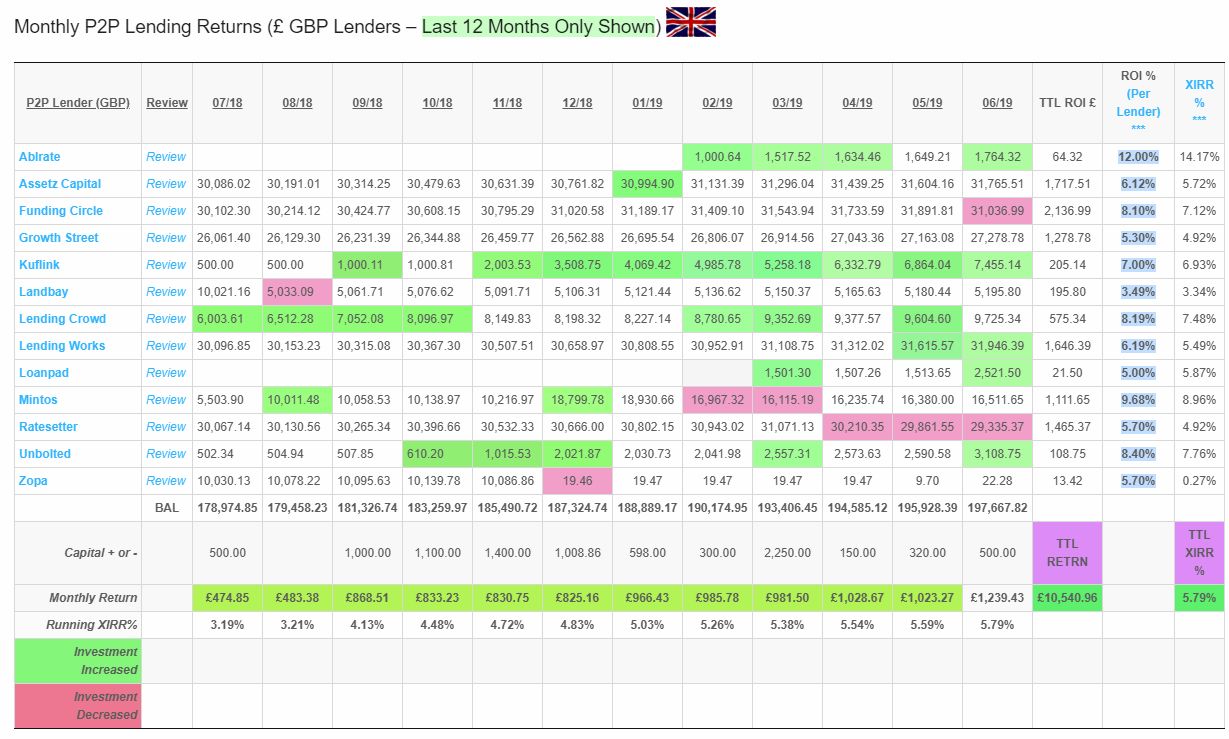

Total GBP XIRR rose just a little again from 5.59% to 5.79% in June, continuing its progression each month since the portfolio was started, towards the target 6% mark. We are likely getting close to the max now as I have a few lenders in there who have a return of less than 6%. That being said, all of the lenders XIRR seems to keep increasing so we’ll see in just a couple more months where it settles.

EURO Portfolio Overview

This is the first month I was able to get a read on XIRR for the Euro Lenders. A target of 6% returns from the GBP portfolio seems paltry when you look at what the Euro Lenders are showing. Even this early in the game, they are averaging almost 13%. I’m still excited for the investment opportunities available in euros. However I still didn’t buy any more euros in June (kicking myself a bit actually as it was down around 1.11 to the USD, I had buy orders set at 1.105). Maybe I’ll pick some up in July. I don’t like paying more than 1.10 for euros.

Moved money

I moved a little money from Funding Circle in June (just repayments, I didn’t sell anything yet). The plan I mentioned last month to redistribute some of my Funding Circle capital along with capital from some of my other larger accounts is still in play, however the return rate has climbed again with Funding Circle so I’m finding it difficult to pull the trigger.

June 2019 Lending Update

On to the individual updates!

There are some great cashback incentives for new investors right now. I have listed them at the end of each lender update, or you can always see my cashback page for current offers on all lenders.

If you are considering investing in any of the lenders I write about, and you think my website is helpful in your research, please consider using my links as I can sometimes get a small commission from the lenders which costs you absolutely nothing and helps me continue to run the website.

You’ll notice the charts below are only showing 12 months of data. This is because the table was getting too big so moving forward I’ll just be using the floating 12 months which is really the most relevant data. You can always get a copy of all of my lending data by downloading a copy of the spreadsheet I use to track my investments.

I sent a little more money over to Ablrate this month and picked up a couple more loans. Nothing exciting to report with them though. Still just watching for now until I decide to move a larger amount of capital over there.

You’ll note that the XIRR on Ablrate is huge (for a UK lender). 14%+ which I believe is mostly due to some secondary market loans I bid on. When bids are accepted lower than the original loan value, the XIRR goes up.

Only one new loan this month (that I noticed anyway) which is the Waste to Energy loan below. I got myself a little piece of it at 14% 🙂

These are my current holdings with Ablrate. The above loan is not shown as it is not yet live.

Ablrate Signup & Cashback Offers

Ablrate offer an exclusive cashback offer to readers of The Obvious Investor – when you sign-up with Ablrate and receive 0.5% cashback on your first investments.

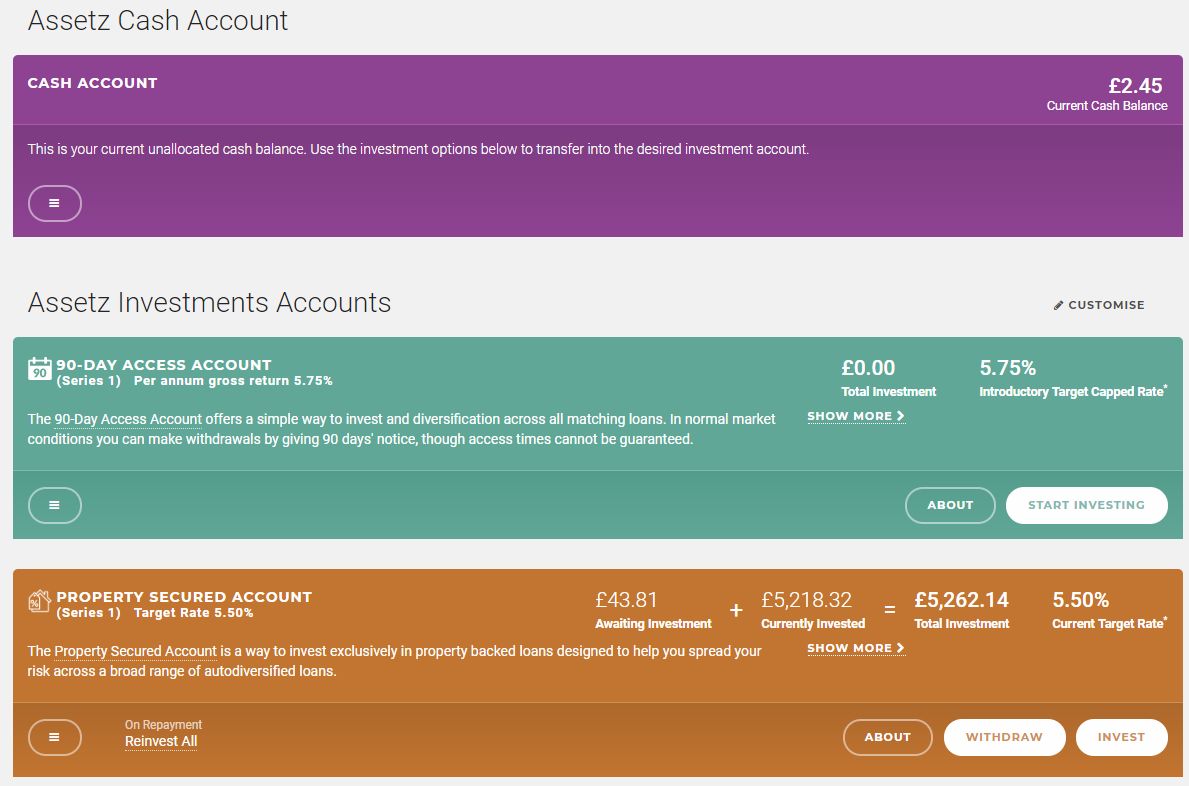

You’ll notice above the rate Assetz Capital says I’m getting now has increased again to 6.12% after taking a little dip last month to 6.06%. XIRR is up to 5.72% from 5.66% last month so everything is proceeding nicely.

Someone emailed me last week and asked which lenders I thought were the safest out of my larger lending accounts. Out of all of my larger (£30k+) lending accounts, I think I feel most safe with Assetz Capital first, then Lending Works, RateSetter and then Funding Circle. I don’t feel unsafe with any of them, but the first 3 have provision funds, Funding Circle doesn’t, however it’s a massive company and at the top for returns. So you can’t have everything 🙂

It’s so difficult to choose between Assetz Capital and Lending Works for the first spot because they are both super-safe lenders in my eyes. Assetz has asset security though, and I think that’s what takes it. RateSetter is just big and your money is also relatively safe there too. It would take a lot for a problem to occur in any of them and put your capital at risk. It could happen though, so always remember that.

Assetz Capital’s cashback finished at the end of May so there is none currently. It won’t stop me from investing more money with them soon though, cashback or not.

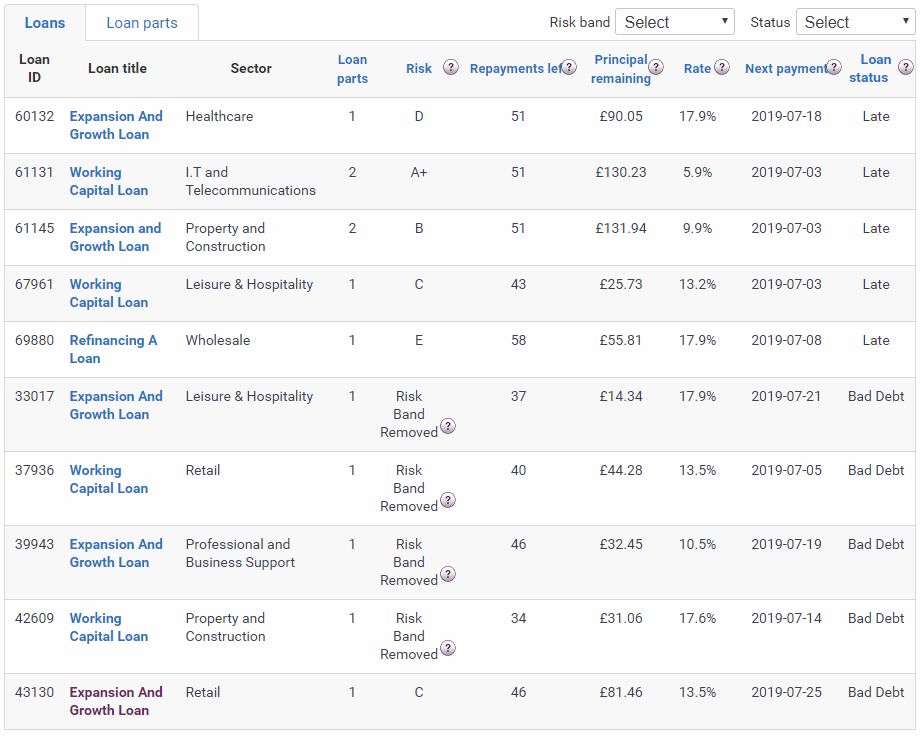

As mentioned previously, Funding Circle really seem to be doing well as far as return is concerned. No further losses this month and the return they say I’ll get annually if I keep all of my money invested and reinvest the income is 8.10%, up from 7.90% last month, and XIRR rose from 6.89% to 7.12% which is really not too shabby after a year lending with them and the defaults issues they were being chastised for. Same number of loans marked as “Late” as last month (21) so not getting any worse this month. Very good sign.

Growth Street are just one of the easiest investments in my opinion. Just set it and forget it!

XIRR rose a little again this month to 4.92% (up from 4.88%) bringing the number closer to the 5.30% target rate they suggest. I have no doubt the account will hit this target rate in the next couple of months. 5.30% is really very good for only having your money tied up for 30 days at a time.

If you look at the screenshot below you can see how everything is taken care of automatically in the background. Interest and capital is paid back after each 30 day period on each loan chunk. Then it is all reinvested automatically into other loans.

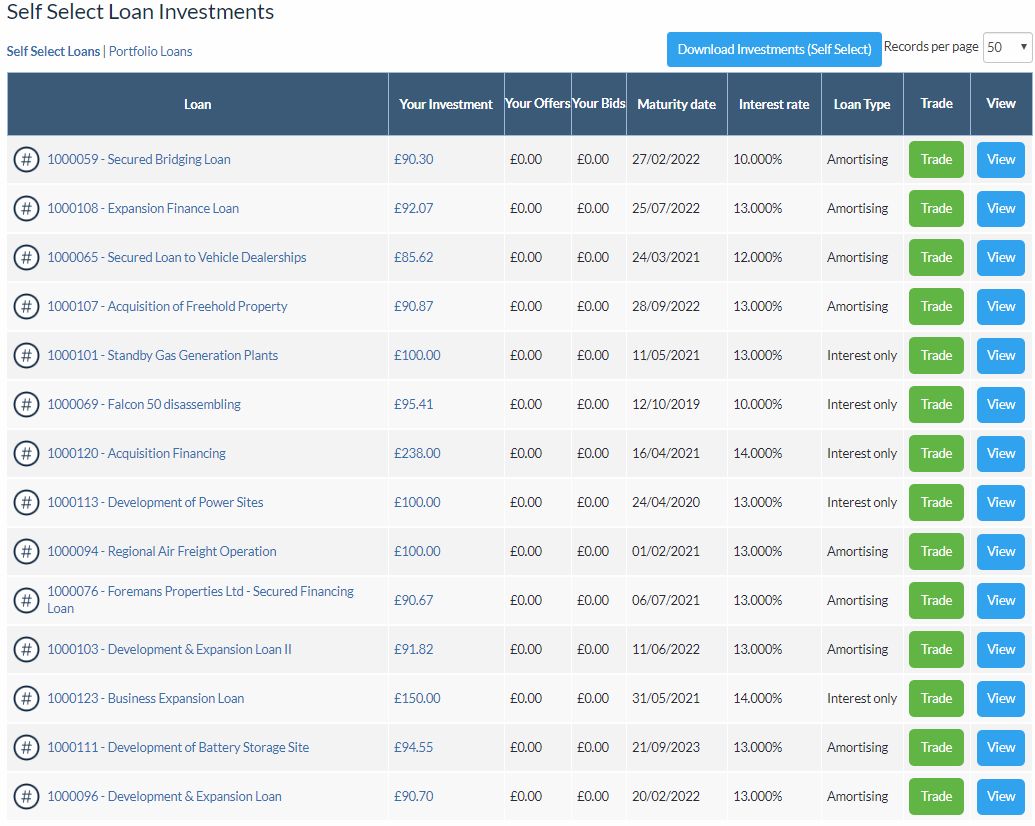

Kuflink’s loan flow keeps on bringing the low LTV loans. They do huge due-diligence on them so the loans are just so well documented. I sent another £500 over to them in June so I could invest in some of the new loans which came out.

June was the 1 year anniversary that I invested my first £500 in Kuflink’s 1 year auto-invest account so the capital and interest was repaid this month (it’s only paid back annually in the auto-invest accounts). I also received some repayments on some other self-select loans which repaid this month.

Finally we can see the sort of returns we are really getting from Kuflink, although remember the interest on the auto-invest account when I invested was a lot less than the select-invest loans I’m investing in now, so I only expect that to continue to grow. The XIRR went from 4.71% in May to 6.93% in June. I expect it to be well over 7% in the next couple of months.

Kuflink really are a very good option for lower risk – higher return investments in my opinion. I’ll be shooting more money over to them as more loans come out as I have done for the past year. They are one of the lenders that I will be increasing my account balance with substantially over the coming months.

I picked up a few more low LTV loans in June as you can see in the screenshot below. I’ve started to put larger chunks of capital into the lower LTV loans now, you’ll see notice I have £530 invested into a 50% LTV loan.

Looks like bad diversification but at 50% LTV, if the loan defaulted, the property would need to lose 50% of it’s value before I lost a penny. On top of that, Kuflink have 5% “skin-in-the-game” on a first-loss basis, so really the property would need to lose a total of 55% of it’s value before I would lose money. That didn’t even happen in the 2008-2009 financial crisis so it’s really unlikely. And if it did, I think there would be a lot more to worry about than the £500 invested in that.

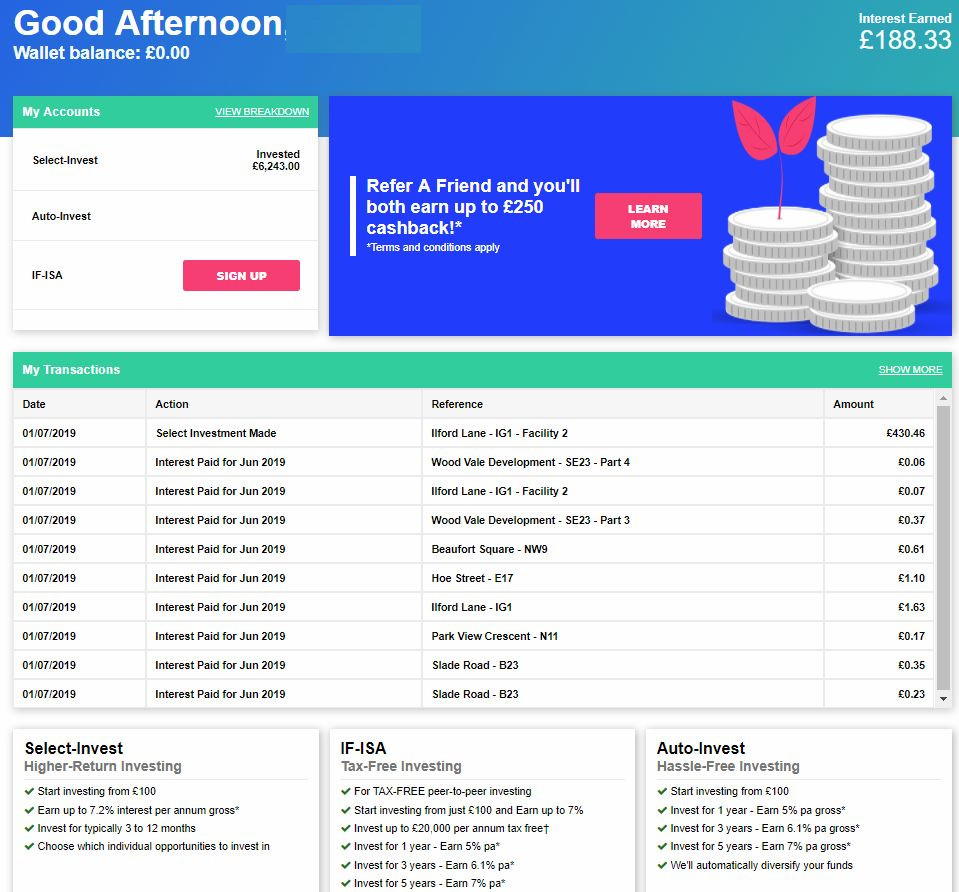

When you look at the account dashboard (first screenshot) you’ll notice it doesn’t match the numbers on the Peer to Peer Lending Results Page. It’s something that could be improved. However if you want to see your net account worth, just click on the “Show More” link on the “My Transactions” section and you get the statement below which gives a better calculation.

Kuflink have a wonderful cashback offer right now which is well worth taking advantage of if you are thinking of investing with them.It equates to 10% at the lower level, and 5% cashback when you get to £5000. Not half bad for asset secured loans with these kind of low LTV’s.

Landbay – “The Peer to Peer Banking Solution” – NOT REALLY! But about the safest lender in the P2P world. About the lowest returns though.

Honestly, if I was really risk adverse, this is probably where much of my capital would be sitting. That being said though, I think there are some safe options out there now with risk similar to Landbay but better returns. As previously mentioned Kuflink’s‘ low LTV loans I consider to be fairly safe, as well as the new lender Loanpad who also have loans with very, very low LTV’s and pay 5%+ with a 60 day notice window. Assetz Capital’s QAA account pays 4.2% on (mostly) asset secured loans with instant access to your money. Or Assetz Capitals Property Secured Account (PSA) is also a good option for asset secured investing and pays 5.5%.

For the said-to-be-safer option for your money, or just for some diversification, Landbay currently have an incentive for new investors: £50 cashback when investing £5000 or more. Click here for more information. Taking this cashback offer increases your income on this investment by 1% for the first year which helps.

Lending Crowd are still delivering with XIRR jumping again this month from 6.56% to 7.48%. A huge jump in returns in one month. I believe this comes from their management of overdue loans. They are still targeting my annual return at 8.02%. I’m starting to think they are going to be dead on. Not bad at all for the Edinburgh based Scottish lender.

You’ll notice in the screenshot above that I’m getting a bit of cash drag. That’s because I have my auto-bid settings set a little high now as there is a lot more capital from investors coming in to Lending Crowd. I just dropped the rates I’m willing to except a small bit so that should get lent out now.

If you remember last year I was getting a little concerned about their late loans, but now I’ve seen the Lending Crowd team manage them, that concern has gone away. They do a great job of either getting borrowers to pay up, or selling the assets and collecting. There are always between 7 and 12 late loans, but a lot of them come current again. On almost 400 total loans in my portfolio, that is very, very good.

Lending Works income was back on track this month after a small dip in May. June was the second highest month since the portfolio began at £180.82.

XIRR keeps slowly climbing from 5.33% last month to 5.49% in June. Even Lending Works own target numbers for my account rose a tiny bit once again from 6.19% to 6.20%.

You really can’t go wrong with Lending Works. Great rates with the safety of the best provision fund in the business, the “Lending Works Shield“. There’s a reason they are one of my largest lending accounts with almost £32k invested.

As you can see below in the screenshot, my repaid capital is being reinvested at the 6.5%. I initially got into Lending Works about a year ago at 6.0%, so it’s nice to see the rates climbing steadily as my reinvestment capital gets lent out at the higher rates.

If you decide to invest with Lending Works (which if you’re getting in to P2P, you probably should consider), they still have the 6.5% available, so if you’re thinking of investing with them, consider doing it sooner rather than later.

Remember, RateSetter was at 6.7% just a few months ago, now they’re at 5.4% 🙁

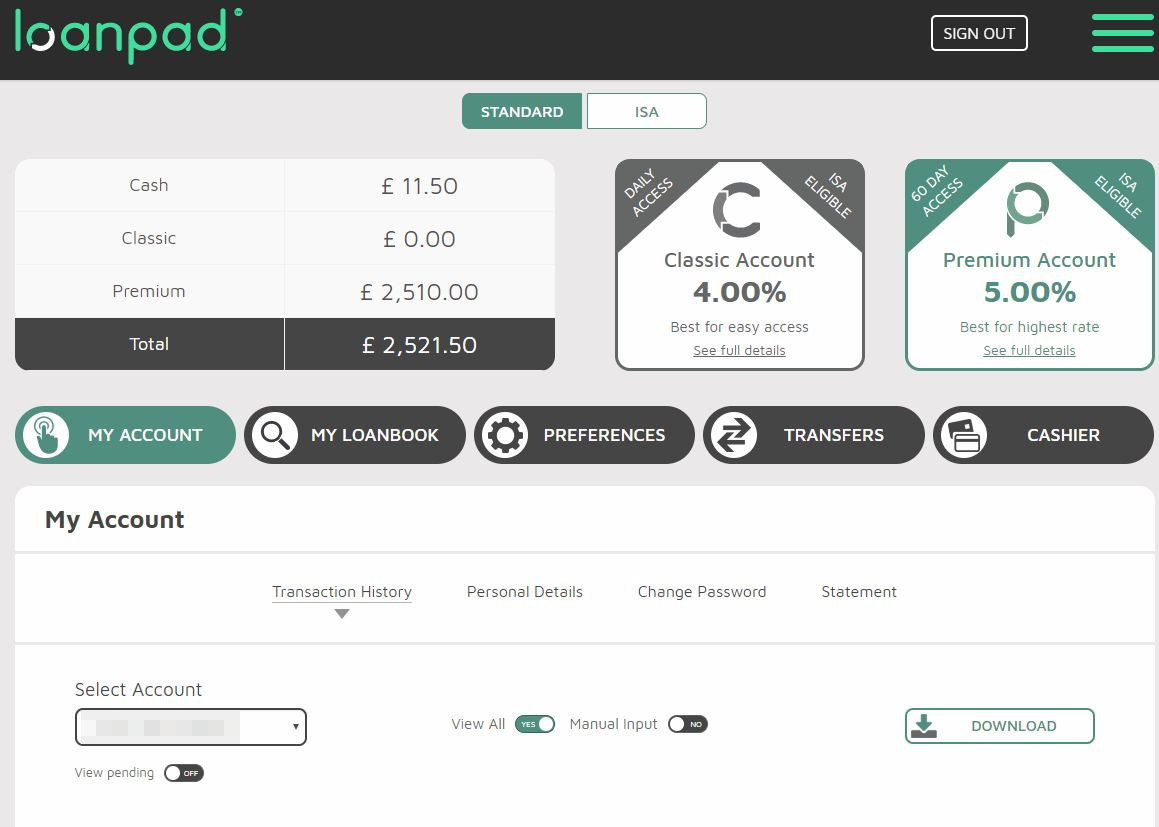

I’m getting more and more comfortable with Loanpad. So much so in fact that I sent over another £1000 to them in June. The more I invest with them, the more it makes me like them a lot. See the Loanpad Review for more detailed information on why, but it’s mainly due to the low LTV’s on ALL of their loans (see screenshot below), plus their loan originators 20% – 60% “skin-in-the-game“.

Also did you notice the XIRR on Loanpad? It’s at 5.87%! That’s on a target return suggested by them of 5.00%. This is because the Loanpad target rate is the actual rate you get (similar to XIRR) instead of the AER (Annual Equivalent Rate) given by most other lenders (both Peer to Peer and Banks/Building Societies) which estimates the rate based on all of the interest being invested back in to the account. So, because I’ve been investing all of the interest back in to the account, my XIRR is higher than the Loanpad target rate.

Do you see the loan at the bottom of the screenshot below with a 5.76% LTV? Seriously, how are you ever going to lose any money on that loan? Have you ever known any real estate, anywhere, losing 94.24% of it’s value? Especially in a first world country like the UK? That is what would need to occur for you to lose any money on that loan. Even then I’m not including the loan originators first loss “skin-in-the-game” percentage which would take any loss before other lenders on the platform. Never going to happen in my opinion. And if it did, you’d have a lot more to worry about than your money in Peer to Peer lending accounts.

On top of that, both of Loanpad’s accounts have relatively early exit available (immediate on the Loanpad Classic Account, and 60 days notice on the Loanpad Premium Account for free, or immediate exit for a fee of 0.5%). If you’re risk averse but still want to make a reasonable return on your capital, you could do a lot worse than Loanpad. I’ll be sending more money over there in weeks to come.

You can see in the screenshot below, interest is being paid back daily in to my lending account, which I then reinvest when it gets to over £10.

If you’re going to invest with Loanpad, they have a cashback incentive right now – £50 bonus if you invest into a lending account a minimum of £1,000 within 4 weeks post registration and keep this invested for 365 days; or £150 bonus if you invest into a lending account a minimum of £10,000 within 4 weeks post registration and keep this invested for 365 days.

Mintos GBP MoGo car loans have slowed down a bit, which means there could be some potential cash drag. So far though I have been able to pick up loans on the secondary market through an auto-invest bot that I have set to pick up loans with 0% premium.

Mintos is still my highest earning GBP account by XIRR (apart from Ablrate which is still new and does not have significant capital invested yet), which rose once again this month from 8.82% in May to 8.96% in June. Based on this, I believe there is still a good chance we will hit the Mintos target rate of 9.68% (which itself rose again from 9.67% in May), probably around August or September.

Unfortunately I received an email from Mintos saying that UK residents can no longer invest in Mintos loans for now. The good news is that this is because Mintos are setting up a UK loans division which will no doubt be regulated by the FCA and have lots more GBP options!

So if you’re a UK resident, hold your horses for a few weeks and hopefully Mintos will be available as a UK based, FCA regulated investment. When this happens, Mintos are going to absolutely kill it if they offer the same rates they offer now along with “Buyback Guarantees” as they offer on most of their current loans.

If you are NOT a UK resident right now, Mintos have a wonderful cashback bonus, one of the best in fact. Mintos offer 1% of the value of your investments cashback for the first 90 days you are investing with them!

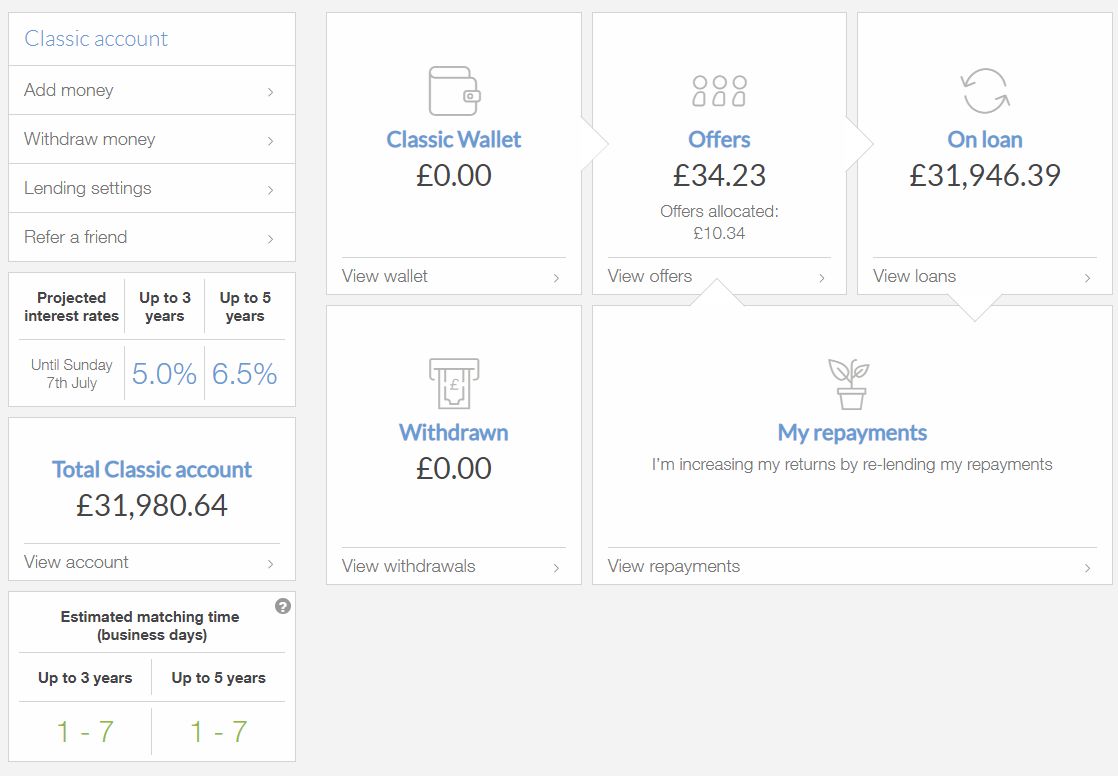

Interesting story on RateSetter in June. For the last few months, RateSetter’s rates have been falling. You can see in the screenshot above it’s sitting at 5.4% average on the 5 year.

The first week in June, I got an email from RateSetter saying that I had a few loans repaid early. I logged on to my account to see about £8k in cash sat there waiting to be lent! I didn’t want to lend it out again in the low 5% area so I started to think about moving it. Then on the following Sunday, I logged in to my account to see rates kicking 6% again! So I quickly put in a lend order at 6% and my £8k got lent out. This had the effect of raising my RateSetter target rate from 5.50% to 5.70%!

I’ve mentioned in previous updates that RateSetter rates seem to climb at the weekend, so it’s really worth waiting if you have money to invest with them. Even in the data screenshot below you can see average rates have begun to rise again which is good news!

As rates are rising again now, if you were thinking about investing in RateSetter, it’s a good idea to shoot some capital over to them so you can take advantage of the 6%+ “weekend blips” as and when they happen.

RateSetter is an excellent option for diversification and safer lending with a big lender. RateSetter’s very well funded provision fund doesn’t hurt either.

RateSetter is offering £100 cashback for investing £1000 for a year (10% ON TOP OF standard returns, so even if you only want to invest £1k, you’ll get 15%+ back for the first year), it is definitely worth considering, especially if you can get in at the 6%+.

I decided to send another £500 over to Unbolted in July to see if my newly found method for getting capital lent out faster was still working. I’m very happy to say that it does! And the capital was lent out in the first week 🙂

XIRR rose again this month from 7.57 in May to 7.76% in June making Unbolted my second highest GBP account based on XIRR. See my Unbolted Review for more info. on how I’m getting more capital lent out.

Euro Portfolio Lenders

Once again in June I didn’t add any new Euro lenders, but I intend to do so as soon as I can change some more euros. I’ve been waiting on that as I mentioned at the beginning of the post but I’m getting impatient (not a good thing).

I am interested in observing how my investments are doing with the lenders I started with in April.

As you can see on the table below, we finally have enough data to post XIRR numbers on the Euro Lenders. They have some exciting numbers, and as with the GBP portfolio, I expect them to continue to grow for the first 12 to 15 months.

Total income in euros for June was a little over €400 which is huge when you take into account that all I have invested is €30k.

Not a great deal to update you with on Crowdestor this month. I reinvested the interest I had earned into another loan as you can see at the top of the list above. Apart from that, everything seems to be on schedule. As soon as I get some more euros, I’ll be picking up a bunch more of Crowdestor’s loans.

Detailed information on their loans is public and can be seen on Crowdestor’s website

Not many new loans from Envestio this month as I believe they are working with some new borrowers. That’s ok with me as I have no euros to invest with them right now so hopefully they are saving the best loans for me when I finally decide to exchange some USD to euros 🙂

Their loans look risky but actually I’m quite comfortable with Envestio the more I research them. We’ll see if I’m right or wrong in time but for now I’ll invest more euros when I get them.

Grupeer are still doing their “Mini Mintos” thing which is working great! I honestly haven’t had to touch this account since my first investment with them. First take on XIRR is at 11.24% which of course will keep climbing for the next year or so I would think.

I’ll have no hesitation at putting some more euros in to Grupeer when I get them. I’ve been doing more research and they really do seem like a solid, well managed company.

Mintos is just a beast of a platform, and with the number of loans they have, it seems like a small country could get capital invested into loans if they wanted. I often see almost 500k loans available just in the primary market, another 400k+ in the secondary.

My Mintos euro lending target rate rose from 12.93% in May to 13.22% in June. The interesting thing here though is that XIRR is showing 14.81% which is more than the Mintos target. I have no idea why that is, unless Mintos is not taking into account that most of the short term loans are with the loan originator Varks who actually pay interest on delayed loans until they hit the buyback guarantee. Either way I’m not complaining about that.

I’ve seen some 17% Varks loans on Mintos in June, plus MoGo have actually started throwing 16% secured car loans in there. Once I get some more euros changed, there will be a significant upgrade to my Mintos euro account. If you’ve read any of my previous Peer to Peer lending updates you’ll know that I have a huge crush on Mintos ♥ 🙂

If you remember in last months update, I mentioned about the number of overdue loans with RoboCash. Well, as I was told at the time, there is no problem at all. It is just part of short term lending. I’ve been watching them and they change day by day. There is always quite a high percentage of loans late and they just get bought back each day.

No worries with RoboCash. I will be investing more euros here too once I buy some. They are currently showing XIRR returns of 12.11% which is a little higher than the 12.00% target. No complaints here about that.

Summary

That’s everything for another month. A shorter post than last month but no use just repeating myself if there is nothing new to say. You can always go back and look at the previous updates for more details on why I’m investing in these companies.

June was the best month for my P2P lending, surpassing the £1200 in GBP and €400 in euros. Not half bad which ever way you look at it.

Finally I hope the month of July goes well for everyone. I wish you all the best of luck with your investments. I will update you on my P2P Portfolio investments around the same time next month.

Thanks for reading my blog! Please feel free to comment below if you have comments, questions, criticisms or suggestions. You can also email me if you prefer. I love feedback!

Please note, most of the cashback offers on this site are for new lenders to a company. I suggest you do your own research before investing as cashback offers change daily.

This page is presented for informational purposes only. I am not a Financial Adviser and therefore not qualified to give financial advice. Please do your own research and make your own investment decisions. Do not make investment decisions based solely on the information presented on this website.

* My opinions, reviews, star ratings and risk ratings are based on my personal investing experience with the company being reviewed. These ratings are personal opinions and are subjective.

** Some of the links on this website are affiliate referral links. When you click on these links, I can sometimes receive a commission, at absolutely no cost to you. This helps me to continue to offer new reviews & monthly portfolio updates here on my website. I don’t receive commissions from all platforms and it has no effect on my ongoing opinions on investments & investment platforms. Income from my investments and capital preservation are my main motivations.

Platforms reviewed on this website I am currently investing with, or I have invested with in the past. You can see with full transparency on my Portfolio Returns page which assets & platforms I am invested with (or have previously been invested with) at any point in time. I am not paid a fee by any of the companies to write reviews, so the reviews are unbiased and purely based on my own personal experiences.

Please read my full website Disclaimerbefore making investment decisions.

The Obvious Investor website uses cookies to offer you the best possible browsing experience. By browsing this site, you give us the ok to use cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

_abck

1 year

This cookie is used to detect and defend when a client attempt to replay a cookie.This cookie manages the interaction with online bots and takes the appropriate actions.

bm_sz

4 hours

This cookie is set by the provider Akamai Bot Manager. This cookie is used to manage the interaction with the online bots. It also helps in fraud preventions

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_gat_gtag_UA_127056176_1

1 minute

This cookie is set by Google and is used to distinguish users.

_gat_UA-127056176-1

1 minute

This is a pattern type cookie set by Google Analytics, where the pattern element on the name contains the unique identity number of the account or website it relates to. It appears to be a variation of the _gat cookie which is used to limit the amount of data recorded by Google on high traffic volume websites.

_gcl_au

3 months

Provided by Google Tag Manager to experiment advertisement efficiency of websites using their services.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

NID

6 months

NID cookie, set by Google, is used for advertising purposes; to limit the number of times the user sees an ad, to mute unwanted ads, and to measure the effectiveness of ads.