To start off this update, I need to apologize as I haven’t done a public update of the site in a couple of months because, even though the P2P sector has been in turmoil for the last few months, not a great deal has changed with many of the lenders. Also I’ve had more pressing family things going on so I haven’t been as focused on the site.

I decided this month though I’ll update everything (including the Growth Portfolios) so you know what I’m up to as far as my investments go. I’m going to be brutally honest about some of the Peer to Peer lenders, and it will likely not “jive” with some of the other bloggers out there who perhaps have different opinions.

At a high level, I’m still invested at about 50% of my highest number with around £100,000 in GB Pound P2P investments (from a high of £205,000) and I also have about €30,000 left in Euro P2P (from a high of $54,000).

Many of the lenders I used to invest in have either become bankrupt, unstable or darn right dangerous because of the economic conditions caused by COVID19. Some lenders actually seem to be thriving from this COVID19 situation though and the ones that are, have huge business coming through from the ones that are doing not as well.

NOTE: I have labeled some of the updates as “Same as last update” which obviously means if you read the last update, nothing has changed.

Disclaimers

The information below is comprised of my opinions on current investment market conditions and my personal actions with my investments. It should not in any way be construed as financial advice. Please do your own research before making investment decisions and do not base them solely on what you read on this website. Please read my full disclaimer of more information.

Some of the links on this website are affiliate referral links. For cashback offers, you’ll generally need to use these links to qualify for the cashback. If you use these links I can sometimes receive a commission, at absolutely no cost to you. This helps me to run the website, write new platform reviews and publish monthly portfolio updates. I don’t receive commissions from all lenders, and it has no effect on my ongoing opinions on platforms, which are entirely focused on generating Income from my investments and preserving capital

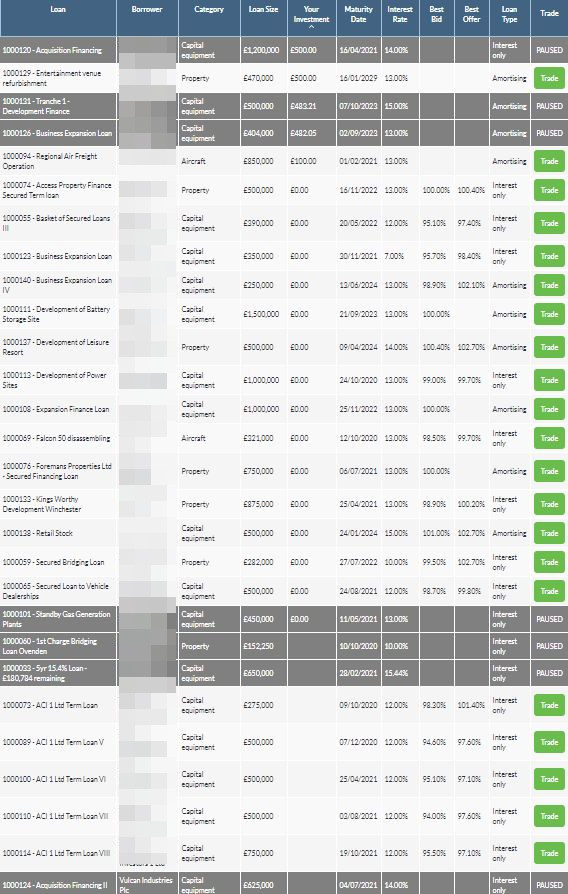

Ablrate still seem to be plodding on, although several of their loans have been “Paused” typically meaning they’re in default. Updates are still forthcoming on loans even though all are not 100% positive (how could they be in this economic situation). I sold most of my loans with higher LTV’s as I’m trying to reduce risk in my P2P lending. I currently have a few loans which are “Paused” and not repaying yet. Not many new loans from Ablrate recently so I have a feeling they are more focused on managing the clients they already have.

Here is a view of the Ablrate loans as they stand. The brown sections are “Paused” loans (click to enlarge images).

My Ablrate Strategy.

I’m drawing down my investment with Abrate now as it becomes available. Not in any major rush as I consider capital relatively safe there, but the loans they have tend to be on the medium to high risk scale & they have about 20% of their loans late or in default so reducing exposure further is a sensible move.

Assetz Capital are still having liquidity problems with their Access Accounts. Trying to get capital out is still not happening at the moment. They implemented earlier in the year a small percentage fee for investors which they are taking from income as they are not making any money from new lending at the moment. Not a great thing, but I would prefer they did this than go out of business as retrieving capital at that point, even though loans are asset secured, would be a long drawn-out process.

Here is the latest update basically saying that the provision fund will no longer be able to cover some of the loans in the Access Accounts, so they can no longer be sold, which means money is stuck until they can be sold, are repaid, or default & assets have to be sold:

Here’s what my account looks like now:

My Assetz Capital Strategy.

I’ve decided to draw down investments from Assetz Capital until they sort out the liquidity crunch. I’m not really worried about losing money as all loans are asset secured, but until things calm down, I’ll not invest more. If they are still around when everything settles down, and they adjust their business model to compensate for drastic economic conditions, I will start to reinvest at that time.

CrowdProperty appear to be thriving in the current COVID19 climate. They offer property secured development loans, all with first legal charge and reasonable LTV’s. I continue to feel like the loans they have written are well vetted, and are some of the safer development loans available in the P2P market.

In August, CrowdProperty wrote more loans than they did in many months before the crisis, and their loans are filling up faster than ever! I used to complain that you had to be fast because loans filled up in a few minutes. Now they fill up in seconds. CrowdProperty have benefited big time from the economic downturn and appear to be well.

All that being said, I do have loans that keep getting delayed, but this is to be expected. Many borrowers are slower to finish developments and therefore need longer to pay their bridging loans back.

Here’s a screenshot of upcoming loans for the first part of September.

My CrowdProperty Strategy.

My capital will be staying with CrowdProperty. I’ll add more capital as things progress if the loans continue to be filled quickly and loans continue to be paid back on time. Of course I’ll keep an eye on things and this strategy could change at any time.

My Funding Circle strategy for the COVID-19 situation is the same as it has been since July 1st 2019 – trying to sell out and get my capital back. Nothing has changed, they still have no liquidity and all I’m doing is receiving monthly loan repayments (sometimes). I would not recommend investing new capital with Funding Circle.

Here’s a screenshot of my account with the “mess” that is Funding Circle.

Funds in Growth Street are still locked up as their “Liquidity Event” became a “Resolution Event”, which then became an orderly wind-down of the company. Growth Street are now focused (they say) on retrieving investors capital. On a positive note I did get a nice little chunk back (around £4.4k) but there is still about £9k stuck in there with the hope of another payment at the end of October (see screenshot below).

Personally I really can’t say much positive about Growth Street or the management. I believe they changed the T&C’s illegally going into the pandemic, and they sold to investors benefits of the platform, which when the sh*t hit the fan, turned out to be false and downright lies. I’m talking about the fact that we were supposed to be able to get capital out within 30 days whatever (30 day short term financing), which obviously was not the case.

My Growth Street Strategy.

Get my remaining capital back (about 9k now), wipe my brow and learn from the experience.

Kuflinkis another platform that seem to be benefiting from the COVID19 situation. They are still bringing new loans to the platform en-mass, and they are still being filled relatively quickly . This shows that investors still trust Kuflink enough to invest with them. Kuflink are going from strength to strength. It’s nice to see them doing well. They offer a fair return for the risk.

I have had several loans paid back in August from Kuflink. To be fair, there are also a few that are delayed, but that is to be expected, and they are all low LTV loans so I do expect they will be paid back shortly.

My Kuflink Strategy.

I initially sold down just a few of the higher LTV loans on the secondary market, just for piece of mind as we don’t know how bad this situation might get. Much of my capital is still with Kuflink though. I’ll be leaving it there for now and probably also lending into new lower LTV loans as they become available. Of course I’ll keep an eye on things and this strategy could change at any time.

Kuflink Signup & Cashback Offers

Kuflink usually have cashback offers and they change frequently

I decided to retrieve capital (where possible) from lenders who have unsecured loans to reduce my overall exposure to Peer to Peer lending. Although LendingCrowd do have some secured loans, many just have directors personal guarantees. Historically, trying to recover from just these personal guarantees has been hit and miss. So, I made an early decision to withdraw my capital.

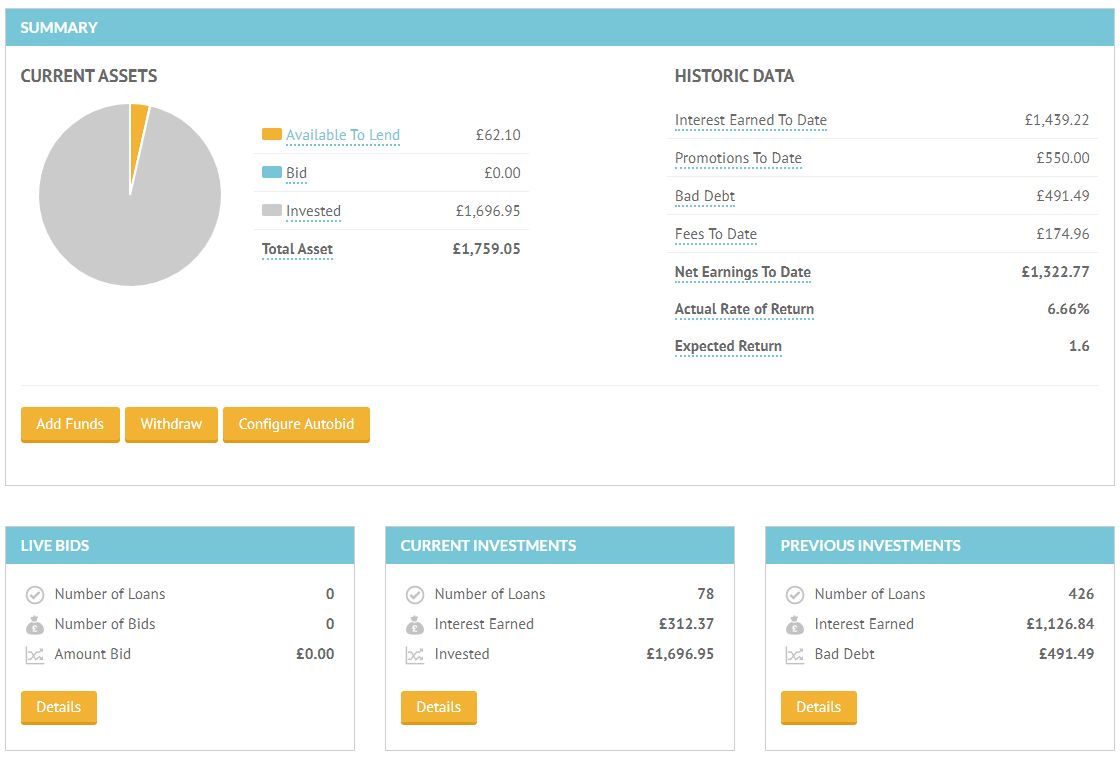

I was able to sell about 75% of the loans as I was early to start selling in March. Repayments have still been coming in slowly and I have been withdrawing capital as they do. I still have about 1.8k left in there and I’ll just draw that down as payments are made as the secondary market has now frozen up it seems. You’ll notice from the screenshot below that the expected rate of return now is just 1.6%. That was around 8% back in February before the crisis.

My LendingCrowd Strategy.

Everything worked out (almost) as expected with LendingCrowd when I started to sell loans. Although I still have a little money with them, I am still receiving payments monthly (although not as much as it should be as obviously some borrowers are not able to pay). I’ll have no hesitation about investing with LendingCrowd again once things normalize, but for now, I’m happy to stand on the sidelines with most my capital in the bank.

I’m lucky as I was able to sell almost all of my Lending Works loans and get out right before the liquidity run came and everyone was trying to withdraw. I still have about £300 stuck in the account but considering that it was 30k at one point, I’m not sweating it.

My Lending Works Strategy.

One thing that irritated me and got a lot of investors upset in March: Lending Works had sneakily slipped in to their T&C’s back in December that people withdrawing loans early are now not only subject to a .5% fee (which I always thought was acceptable), but they are now subject to a shortfall in any loan rates. It really wasn’t clear to most people that they had done this, so when I withdrew my funds, there was another few hundred I had to pay in order to get out. Irritating and reduced the returns on the account, and I will have to really contemplate if I ever want to invest with them again as my trust for this company is weak now. It amazes me that companies like this do underhanded things and expect people will still invest with them.

Loanpad are definitely thriving from the COVID19 situation. Loanpad offer property secured loans, all with very low LTV’s (all below 50%, and many between 5% and 15%). These kinds of LTV’s mean even if UK property values take a huge nosedive because of the recession, even in the event of a default, lenders would probably get their capital back. In the last few weeks of the COVID-19 panic, Loanpad, although a smaller company, have been able to survive and fulfill capital withdrawal requests even from their “Classic” instant access account without having to declare a “Liquidity Event” and suspend capital withdrawals. Even today it is still possible to get capital out without a problem.

Loanpad have reduced their return rates on their accounts a little, just by .50%. So they are still paying 3.5% on their classic account, and 4.5% on the Premier account. We really shouldn’t complain about that when we consider RateSetter (one of the largest lenders) still has many investors capital frozen, and on top of they they just reduced rates on their “Access” account to 1.50% and on their “Max” account from 4% to 2%. Overall with Loanpad though, it seems to be business as usual.

I have withdrawn some capital out of Loanpad, and it was very easy. In my bank account the next day

My Loanpad Strategy.

Capital will be largely be staying with Loanpad (although I have drawn down some, just to diversify risk). I’ve really liked the safety aspect of Loanpad since I started investing with them and it looks like, so far at least, I was correct with this one. They are still getting new investors at a high rate so they are one of the lenders who actually seem to be benefiting from this situation.

Loanpad Signup & Cashback Offers

Loanpad usually still have a cashback incentive for readers of ObviousInvestor.com if you’re thinking of joining:

Mintos has had several loan originators go into default or liquidation over the past few months. I was able to draw out about 50% of my Euro investments over time, but Varks Armenia (part of the Finko Group) lost it’s lending license in March, and guess who most of my short term loans were with 🙄

Mintos looked at Varks and the Finko group guarantee (where larger corporations are responsible for buyback guarantees of their subsidiaries), however they determined that to enforce the guarantee could potentially take the whole Finko group down. So now we have a “promise” by Finko that all loans will be paid back by 2022. Not great news but there you go.

I sold down many of the Mogo GBP car loans just because they are finished anyway (no new GBP car loans on Mintos now), and I thought better to reduce exposure to Mintos as a whole. I still have about £800 in Mogo loans which are paying back slowly.

My Mintos Euro Account Summary (click to enlarge).

My Mintos Strategy.

I’ll withdraw capital from Mintos as and when able. I’ve lost faith in many of the Euro lenders throughout this pandemic so until they get some regulation, I may well just stay out of anything that seems too risky for now. Mintos is the largest Euro lender on the planet so I don’t see them going anywhere, plus they are currently in the process of applying for regulation. However the loan originators are not so solid so best to stay out until things stabilize. I will at that time likely invest with Mintos again.

I exited Octopus Choice in March. Even though they have well asset secured loans, I decided to exit this account anyway for now as 4% is just not worth the risk, and there was no penalty for withdrawal. I was early in making my withdrawal request so was able to get all of my money out (except for a couple of hundred that were in late loans). My feeling is that it’s better to have the capital in a government protected bank account for now, while things calm down. It’s always easy with Octopus Choice to get back in to the loans when things settle down.

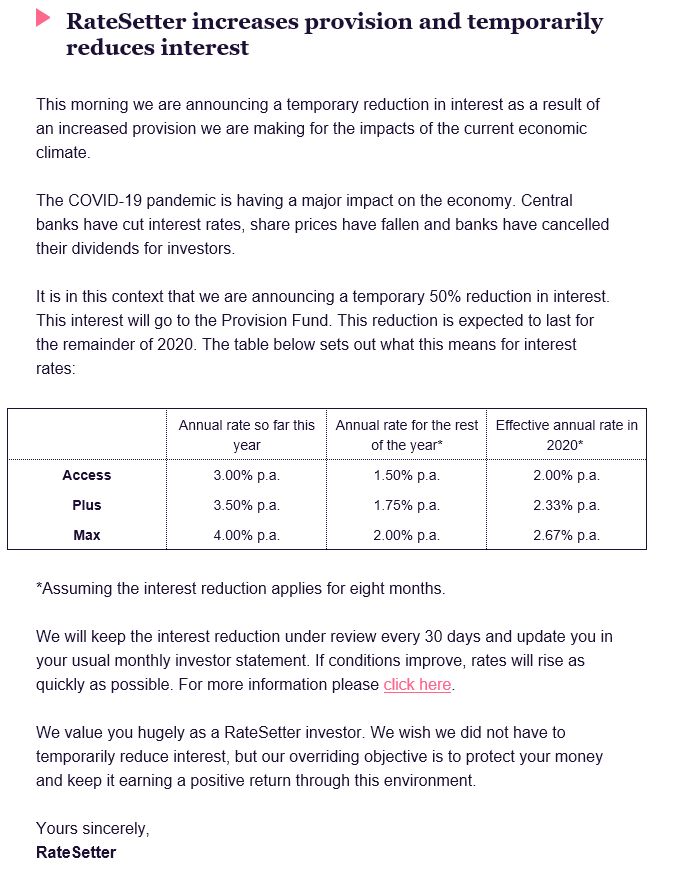

FYI RateSetter was acquired by Metro Bank at the beginning of August for anyone who didn’t know. Here is the announcement

I decided to exit RateSetter March and I was lucky to get out before the liquidity problems set in (still have about £20 stuck in late loans, but considering the account was once £30k, well, you get the picture). A couple of days after I made my withdrawal, RateSetter started to have liquidity problems and now there is quite a long wait to get loans sold and capital out. I think I made the right decision.

To top this off, RateSetter in May sent out the following email saying they are reducing interest rates AGAIN for the rest of the year. 2% for the Max account now? and 1.5% for Access? We can get 1.5% in a FSCS backed bank account with instant access!!! Why the heck would we want to invest with RateSetter? Of course, for the folks that have capital stuck there, not a great update. I read on some of the P2P groups there are some unhappy investors who were (until now) still RateSetter fans.

My RateSetter Strategy.

I am just happy I was able to get out of RateSetter. Unlikely I will ever invest with them again after this. I’ll actually be surprised if they are still in business in a year.

Unbolted are still humming along and doing very well. Even better than before it seems. I keep getting repayments as agreed and defaulted items are still being sold. As I had thought, Unbolted are one of the companies that are benefiting from the COVID 19 situation.

Unbolted offer pawnshop style loans to the general public with very liquid assets. These types of assets can be sold very quickly upon default. Pawnshops typically do better in economic downturns than they do in times of prosperity as people will borrow against personal assets when they are unable to get an unsecured personal loans. LTV’s are usually very low as defaults can be high, so pawnshops need to make sure they can always recoup capital. I have been lending with Unbolted for a couple of years now, and although there have been many defaults, assets have always sold at more than the outstanding loan principle and I have always been paid back both principle and interest very quickly. Loans are short to medium term in nature so a complete exit can be had by turning off auto-invest within 3 to 12 months.

My Unbolted Strategy.

I’ll keep investing with Unbolted as normal as I expect them to be one of the most lucrative investments throughout a recession. Still averaging around 8% returns so no complaints here.

UOWN are an interesting company and off the usual Peer to Peer lender “track” for me. They are not a Peer to Peer lender but a crowdfunding platform where investors own shares in the properties. Although they haven’t put out any new development loans since the beginning of the COVID 19 situation, payments on rental properties are still being received as normal. I did have an email conversation with Haaris (the CEO) and he said that things seem to be progressing well, they are being cautiously optomistic and hopefully will be itroducing some more development projects in the coming weeks.

My UOWN Strategy

I decided to stay fully invested with UOWN. As we actually own shares in the properties (not loans) there can be no defaults. The risk here is that developments might not be sold at the same value (if property prices crash), or perhaps a renter can’t always be found for rental income properties. Either way, even in the worse case scenario, I think most of my capital should be recoverable.

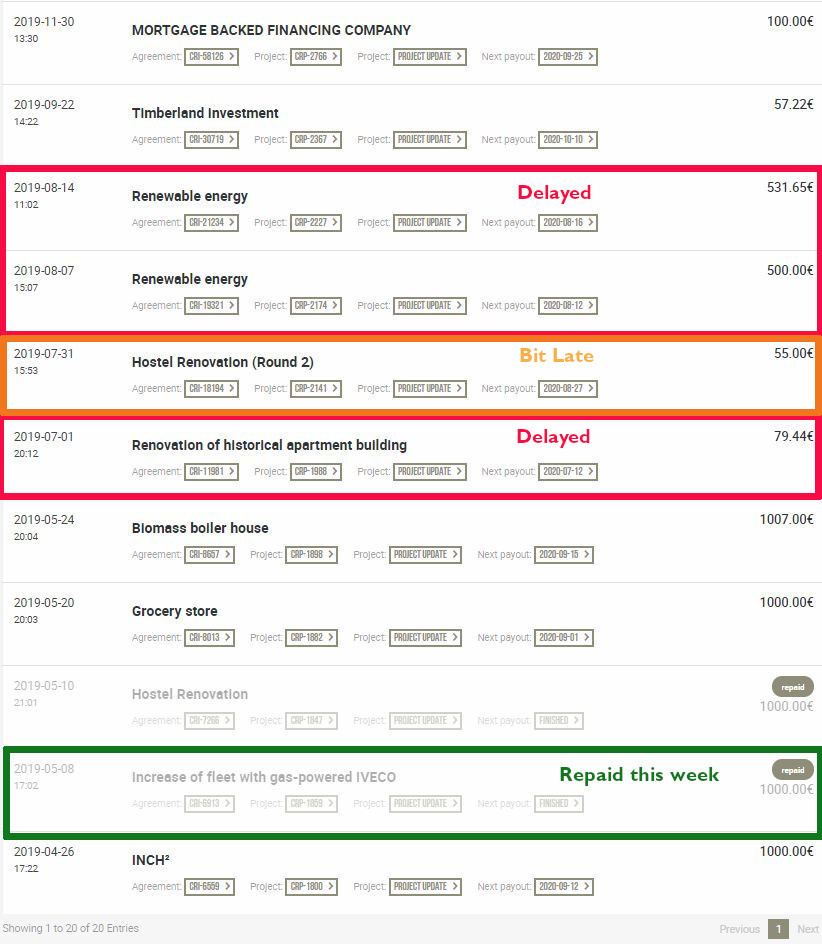

Crowdestor “say” they are doing OK. They keep advertising jobs for programmers etc. I did have one of my loans pay back about €1088 Euros last week, however another 2 loans (Renewable Energy 1 & 2) which should have paid back on August 12th & 16th respectively have been delayed now until October. The positive thing I guess is that at least Crowdestor are still communicating well. It seems overall that Crowdestor have many loans which are delayed, so I’m not sure how this is going to go long term, but again at least they are still trying to make it work. Crowdestor made the decision to pause all repayments from borrowers (and to investors, without asking, which upset a few of them as you can imagine) for 90 days when the pandemic originally hit to give them breathing space. They have also delayed repayments from some borrowers even further so that will obviously affect things. You’ll note in the screenshot of my loan listings below there are several other loans coming due in the next few weeks.

My Crowdestor Strategy

As Crowdestor don’t have any option for early withdrawal (except selling some of the loans at a large 20% discount, which I’m not willing to do), I’ll be riding out the COVID-19 downturn with them until things stabilize. They have been very professional so far so I hope loans will be paid back eventually and Crowdestor will stay in business as they do offer some great returns under normal market conditions.

In January I did a full write up on the Envestio situation (was a scam). If you missed that, you can read it here in the January update.

The law suite is progressing aggressively and the group released some interesting information about the owners of Envestio they had uncovered. Very interesting and all seem to have been in some kind of trouble before. I read they have over €10 million in claims against Envestio from a few thousand investors. I’m obviously skeptical about getting anything out of these investments, although most were asset secured so time will only tell.

Grupeer

Grupeer are either doing a very good job of scamming people, or they are trying to put things right. In April I first mentioned that it appeared like Grupeer are some kind of scam. They had not been replying to investors questions and it looked like some of their projects were fake. From May to August though, we have seen on the Grupeer Blog statements on how they are going to fix this. I have also had several questions answered from their team and they still “seem” to be trying to keep things going. The lawsuit is still moving forward though with some of the investors (here’s a link to a website specifically about Grupeer and the legal action).

On August 31st I received an email stating Grupeer are going to start paying investors back who have completed the KYC information. Who knows if this is true or not, but again they look to be trying. You can read more here.

I guess time will tell what happens next. Perhaps they just panicked when the crisis hit, and now they are trying to patch things up, or perhaps it was a scam . Only time will tell.

My Grupeer Strategy

I’m not convinced I’ll ever see my investment in Grupeer again, and if I do, I definitely won’t invest with them again after this.

PeerBerry really have turned out to be one of the most reliable Euro lenders so far. They are still communicating and managing their loans, and the situation well. Capital has been easy to withdraw from the platform and most of it arrives in my bank account the next day.

My PeerBerry Strategy

I have drawn down my account about 50%, but I’ve decided to stay invested with what’s left for now and I’ll keep a close eye on loan delays etc. PeerBerry thus far have shown they are one of the better (if not the best) Euro Peer to Peer lenders. As soon as things start to pick up, I’ll have no hesitation at all in increasing my investment again with PeerBerry.

PeerBerry Signup & Cashback Offers

No cashback offers with PeerBerry this month, however if you would like to take a closer look at their platform, please;

Robocash are communicating well and truth be told it appears to be pretty much “business as normal”. So far capital has been easy to withdraw from the platform and most of it arrives in my bank account the next day.

Robocash put out their financials to investors in May and frankly they don’t look too bad at all. The platform is part of the larger overall Robocash group which gives all of the subsidiaries strength.

My Robocash Strategy

As most of the loans on Robocash are unsecured, I’ve decided to switch off reinvestment for now and withdraw capital as it is paid back. Robocash has both short term and long term loans. I’ve already managed to withdraw capital from a lot of repaid short term loans. The longer term loans are up to 1 year so I’ll just withdraw that capital as it is paid back until I reduce my overall exposure to about 50%.

So far capital has been easy to withdraw from the Swaper platform as it is repaid, and most of it arrives in my bank account the next day. I’m not concerned about Swaper as a company, but short term, unsecured payday & personal loans will be the first to default if this lockdown is sustained and people can’t work. So I’m not sure how much pressure mass defaults would put on Swaper.

My Swaper Strategy

As most of the loans on Swaper are short term, unsecured loans; I’ve decided to switch off reinvestment for now and withdraw capital as it is paid back in order to reduce exposure. Once I get to about 50% of my original investment, I’ll reassess.

I received an email back in June saying Viventor had been acquired by Atlantis Financiers, one of their loan originators, which happens to be who 98% of my remaining Viventor loans are with. Many of the loans through Atlantis have been extended and are now late between 1 to 60 days (see graphic below). Although it seems loans should still be bought back after the 60 day buyback guarantee period has passed, this has not happened thus far, so I’m waiting to see what transpires in September. It’s kind of difficult to keep track of exactly the date when loans have been extended to, as the loan listings do not make it very clear. The “end date” has already passed on many of them as you can see below.

My Viventor Strategy

For now I’m just watching what happens here as loans are (should start to be) paid back. I’ve already drawn down 50% of my investment with Viventor and I’ll likely keep drawing down moving forward until things become more clear.

A lot is still up in the air with Euro P2P platforms and the lack of regulation makes is difficult to know where each stands. I’m using this experience to see how these platforms come through this to assess which might be the best investments moving forward.

If you do decide to invest in P2P in the current environment, I suggest you stick with lenders with good asset security and low LTV’s like Kuflink, Loanpad, CrowdProperty, UOWN & Unbolted. Or Euro platforms like PeerBerry, Robocash, & Swaper seem to be weathering the storm the best. Do not take my word for it though, do your own research and make your own investment decisions. For some it will be better just to keep all of your capital in a FSCS insured bank accounts for now. I’ve moved a lot of my withdrawn capital to NS&I paying 1.15%, but at least it’s as safe as it can get there. The NS&I growth bonds have no withdrawal penalty so as soon as I start to see other investment opportunities come around, I’ll have the capital to invest at my fingertips.

Good luck with your investments moving forward!

My best to you and your families. Stay safe and I’ll post an investment update again soon.

Disclaimers:

This page is presented for informational purposes only. I am not a Financial Adviser and therefore not qualified to give financial advice. Please do your own research and make your own investment decisions. Do not make investment decisions based solely on the information presented on this website.

* My opinions, reviews, star ratings and risk ratings are based on my personal investing experience with the company being reviewed. These ratings are personal opinions and are subjective.

** Some of the links on this website are affiliate referral links. When you click on these links, I can sometimes receive a commission, at absolutely no cost to you. This helps me to continue to offer new reviews & monthly portfolio updates here on my website. I don’t receive commissions from all platforms and it has no effect on my ongoing opinions on investments & investment platforms. Income from my investments and capital preservation are my main motivations.

Platforms reviewed on this website I am currently investing with, or I have invested with in the past. You can see with full transparency on my Portfolio Returns page which assets & platforms I am invested with (or have previously been invested with) at any point in time. I am not paid a fee by any of the companies to write reviews, so the reviews are unbiased and purely based on my own personal experiences.

Please read my full website Disclaimerbefore making investment decisions.

8 thoughts on “P2P Lending Portfolio Update”

Andrew

Hello i agree totally with your Kuflink assessment. I have been with them for a couple of years and they do exactly what they say on the tin. CV19 has not affected them at all. Proplend is another platform who i invest heavily with, have you heard of them ?

Yes I have heard of Proplend, I was actually looking at them before the virus hit. For now I’m going to hold off with new lenders. I think coming out the other side of this we’ll have some very solid platform choices so I’ll hold off and watch for now.

Looks like you’re right about Ratsetter not being around much longer – acquired by Metro bank (known as a challenger bank).

Metro bank had their own problems in last couple of years – their share price has been a shocker. That was due to the chairman (or similar) paying his wife and dog a huge salary (or something) amongst other issues.

I had a good look at UOWN but in the end went for Property Partner – values have drifted in last few years and it’s a buying opportunity there.

Great article – thanks for taking the time to put together all this detail. Lending Works have indeed been awful through this – zero interest being paid & no update as to when their “Normalisation” period will end. Makes my RateSetter loans look practically awesome…… Ah well, that’s why we diversify investments! Likewise, we’re withdrawing out as any cash paid becomes available and will just have to wait it out for a while yet.

I agree – I have no idea why some of these companies who have just changed T&C’s without a chance to get out think we’ll carry on investing with them as soon as they open up the ability to sell out again…

The Obvious Investor website uses cookies to offer you the best possible browsing experience. By browsing this site, you give us the ok to use cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

_abck

1 year

This cookie is used to detect and defend when a client attempt to replay a cookie.This cookie manages the interaction with online bots and takes the appropriate actions.

bm_sz

4 hours

This cookie is set by the provider Akamai Bot Manager. This cookie is used to manage the interaction with the online bots. It also helps in fraud preventions

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_gat_gtag_UA_127056176_1

1 minute

This cookie is set by Google and is used to distinguish users.

_gat_UA-127056176-1

1 minute

This is a pattern type cookie set by Google Analytics, where the pattern element on the name contains the unique identity number of the account or website it relates to. It appears to be a variation of the _gat cookie which is used to limit the amount of data recorded by Google on high traffic volume websites.

_gcl_au

3 months

Provided by Google Tag Manager to experiment advertisement efficiency of websites using their services.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

NID

6 months

NID cookie, set by Google, is used for advertising purposes; to limit the number of times the user sees an ad, to mute unwanted ads, and to measure the effectiveness of ads.

Hello i agree totally with your Kuflink assessment. I have been with them for a couple of years and they do exactly what they say on the tin. CV19 has not affected them at all. Proplend is another platform who i invest heavily with, have you heard of them ?

Hi Andrew,

Yes I have heard of Proplend, I was actually looking at them before the virus hit. For now I’m going to hold off with new lenders. I think coming out the other side of this we’ll have some very solid platform choices so I’ll hold off and watch for now.

Hi Mark,

I really appreciate the time and expertise you put into your blog, always informative and well researched! A very big ‘thank-you’

Hi Peter,

Thanks for the kind words, you’re welcome & I’m happy you like the blog!

Looks like you’re right about Ratsetter not being around much longer – acquired by Metro bank (known as a challenger bank).

Metro bank had their own problems in last couple of years – their share price has been a shocker. That was due to the chairman (or similar) paying his wife and dog a huge salary (or something) amongst other issues.

I had a good look at UOWN but in the end went for Property Partner – values have drifted in last few years and it’s a buying opportunity there.

Great article – thanks for taking the time to put together all this detail. Lending Works have indeed been awful through this – zero interest being paid & no update as to when their “Normalisation” period will end. Makes my RateSetter loans look practically awesome…… Ah well, that’s why we diversify investments! Likewise, we’re withdrawing out as any cash paid becomes available and will just have to wait it out for a while yet.

I agree – I have no idea why some of these companies who have just changed T&C’s without a chance to get out think we’ll carry on investing with them as soon as they open up the ability to sell out again…

Hi Mark,

Have you tried OnStep investing yet? Interested to hear your thoughts.

Cheers

I’ve spoken with some of the Unbolted staff about it, but I haven’t invested yet. I need to do more research before I comment on it.