Looks like Viventor is winding down its operations. The following emails were received in August & September 2021.

Who or What is (was) Viventor?

Viventor was a European Peer to Peer Lender, providing mostly short term loans to consumers & businesses around Europe.

Offering easy, hands-off returns between 12% and 16%, Viventor is an excellent option for diversification when investing in Euro currency loans. They also offer a “Buyback Guarantees” & Payment Guarantees on most of their loans, which means loan originators will buyback loans and repay principal and interest if payments are delayed more than 60 to 90 days.

Viventor is very similar to Mintos, RoboCash & PeerBerry where it does not originate most loans itself, but uses loan originators (other financial retail lenders, who then list their loans on the Viventor marketplace). This means that their loan flow is generally good, keeping cash drag to a minimum and offering a good amount of diversification. Currently Viventor has more than 20 loan originators providing loans to the Viventor marketplace offering lots of liquidity.

My Experience with Viventor so far…..

Although I only started lending with Viventor recently, they are a very well know platform who are established as one of the better lenders with the Euro lending community.

I decided to start lending with Viventor as they were next on my target list for Euro lenders based on their rates, liquidity and loan originator transparency. None of the Euro lenders have been terribly transparent with information on their originators, however recently Mintos led the way with transparency & ratings, and others are starting to follow suite. Although Viventor still has some catching up to do, they are doing a reasonable job of moving towards providing more transparency.

Once I sent funds to Viventor & started lending, my funds were lent out the same day, and from there on in “hands off investing” has been my experience. I’ve literally not needed to change anything. Their auto-invest system works well, distributing funds between loan originators and loans quickly and efficiently. Once lent out, funds seem to stay invested. They are currently making upwards of 14% annual returns with zero cash drag so far.

Latest Update

Some of the Viventor loan originators are struggling to payback investors because of the pandemic. I am cautiously positive that this will happen, but I won’t be investing any more with Viventor until it does.

My Viventor Strategy

For now I’m just watching what happens here as loans are (should start to be) paid back. I’ve already drawn down 50% of my investment with Viventor and I’ll likely keep drawing down moving forward until things become more clear.

Viventor was launched in 2015 in Riga, Latvia. Since then they have grown the platform to over 7,000 investors and have lent over €120,000,000. They have averaged a return of 13.57% for their investors since 2015. Viventor were originally founded by the Finstar Financial Group giving them the backing and credibility of a profitable, Fintech venture capital firm with over 20 years of experience when they were formed.

In June, 2020, Lotus 597 B.V., a Dutch Investment company, part of the Gielen Group that also owns Atlantis Financiers NV, obtained 100% of the SIA ViVentor shares from the Prestamos Prima Group, which had been invested in by international investor Oleg Boyko in 2016. Lotus 597 belongs to the Gielen Group from the Netherlands and is responsible for investing in promising FinTech start-ups and scale-ups. Viventor has now become a Dutch owned peer to peer (P2P) loan investment platform which clearly exceeds the status of a start-up.

Is Viventor Regulated?

Viventor is not regulated as the UK Peer to Peer lenders are by a special entity like the FCA, however now they are based in Latvia which is part of the EU and as such, they will need to adhere to European financial laws. Viventor is also in adherence with the legislative acts of The Republic of Latvia. A bespoke regulation on peer-to-peer lending is currently also in making in Latvia, but not in place as of the date of this Viventor review.

With many of the European lenders, investors look more at the history and strength of the lender, and also asset security to assess the safety of a platform. Instead of relying on a regulator.

How to Signup & Open an Account With Viventor

Opening an account with Viventor is relatively easy. Just the usual ID & anti money-laundering checks.

They typically need a copy of your passport or ID card. A utility bill or bank statement to show your current address will also be required. Both can be uploaded to the platform digitally.

Residents of most countries who can comply with the ID & anti money-laundering checks can signup with Viventor. You’ll also need a Euro currency bank account.

If you don’t currently have a Euro bank account with IBAN number, take a look at this post I did on Currency Exchange and Moving Money which might give you a few ideas.

How Are Deposits & Withdrawals Made?

Deposits and withdrawals are made by bank transfer (SEPA transfer so IBAN number required).

You will be provided with the relevant bank details when you go to the deposits screen.

Deposits usually show up in your account the next working day depending on what time you send them (although they say 1-3 days, this has not been my experience).

Withdrawals are only to a verified bank account, and typically take 1 – 2 business days.

How Long Does It Take To Distribute Capital? – Viventor Review

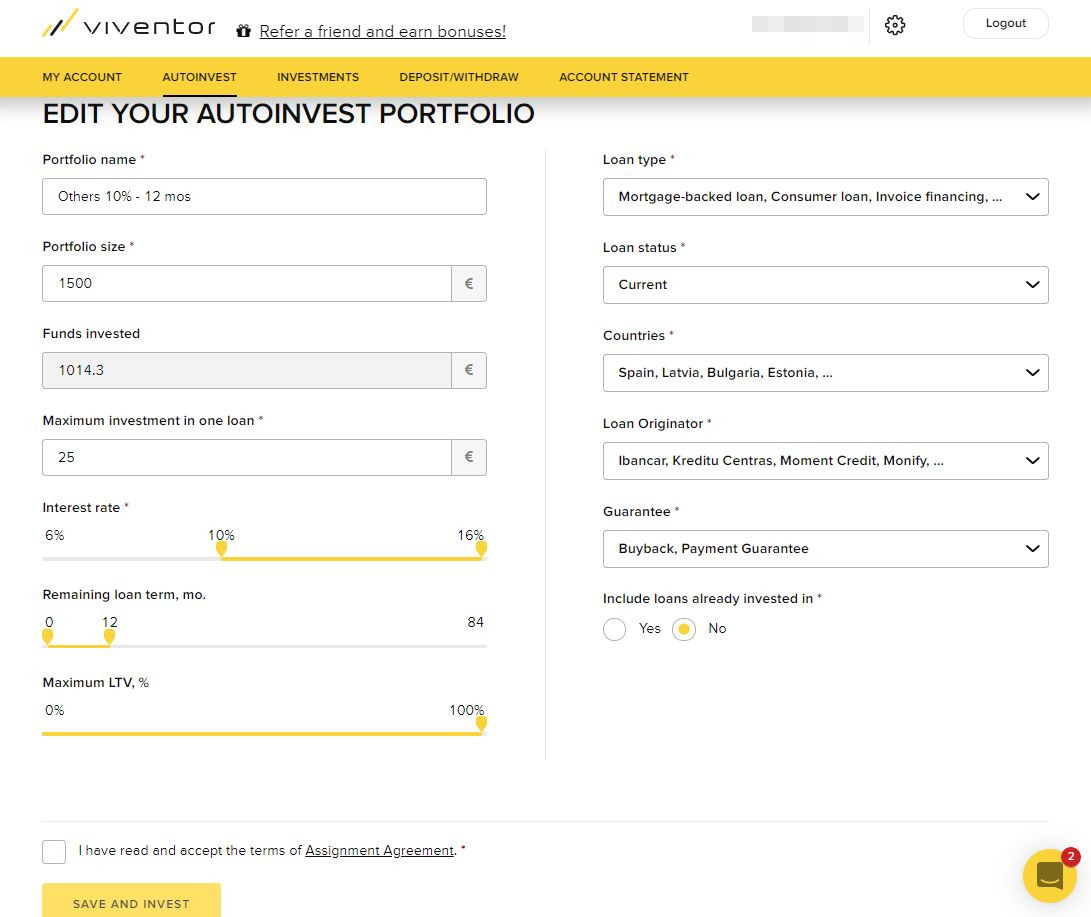

Viventor has a good sized loan book provided by over 20 loan originators. If you use auto-invest (as I do) then once you’ve set up your investment strategy, your capital should get distributed into loans within a few hours. As you can see in the screenshot below, the loan criteria and settings are relatively basic and easy to setup. My personal Viventor lending strategies are discussed later in the review.

If you choose to lend manually with the regular loan listings, it will take as long as it takes you to decide on which loans you want to be invested in, to get capital lent out.

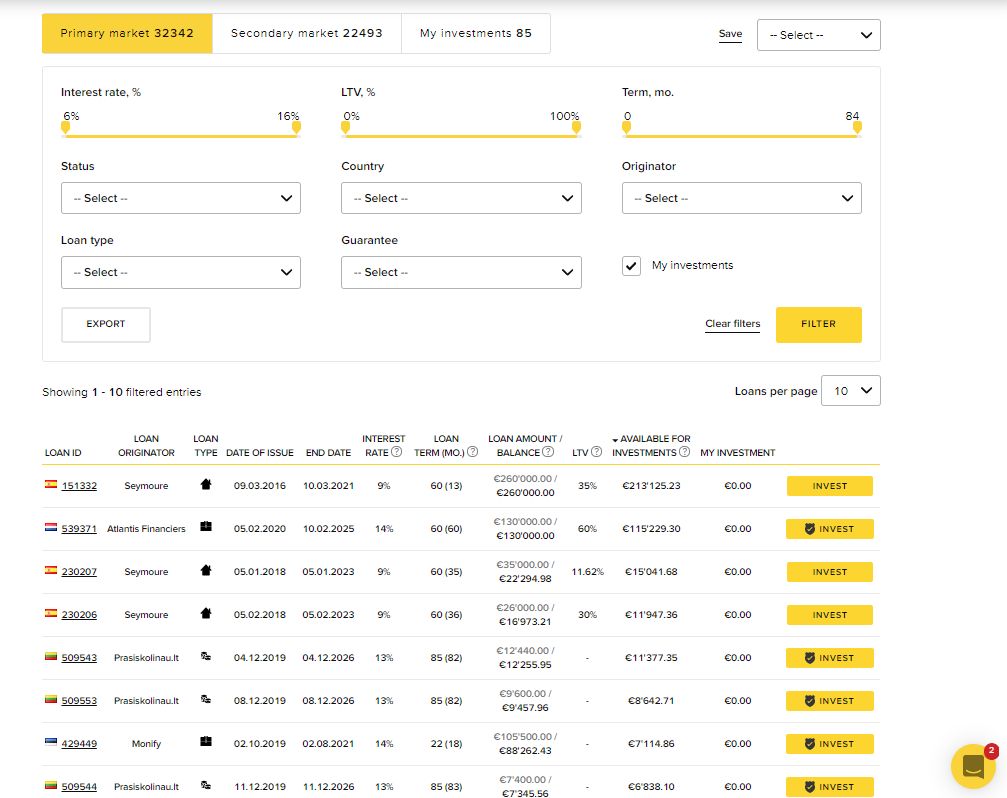

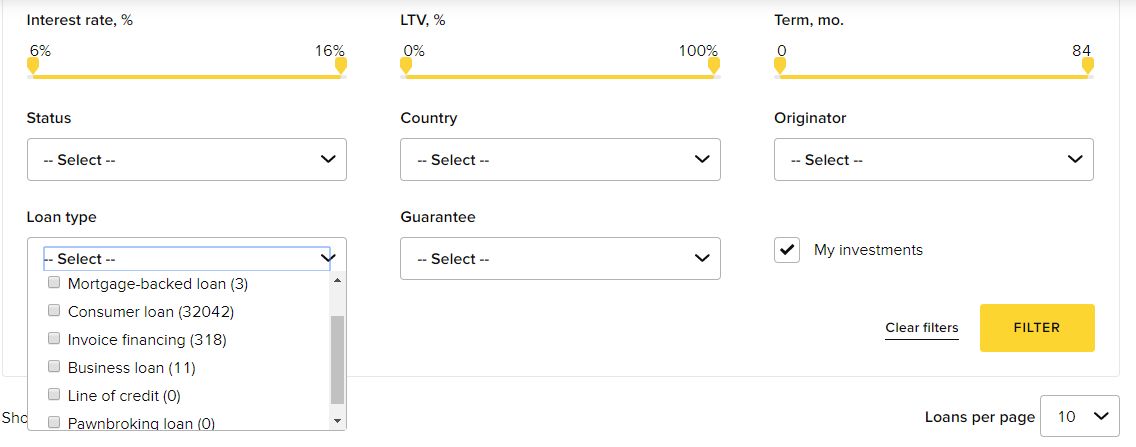

Viventor has a good set of filters, which means you can filter on required fields (similar to the auto-invest filters) to find loans you want to invest in manually.

Who are we lending to With Viventor? – Viventor Review

Viventor P2P is a true Peer to Peer Lending Platform. Lenders (investors) are lending directly to borrowers. Loan agreements are directly between the lender and the borrower. Viventor just acts as a middle man, managing loans, payments and debt collection etc.

Similar to Mintos, Grupeer, Robocash & PeerBerry, Viventor itself doesn’t originate most of the loans like many Peer to Peer lenders. It has over 20 “loan originator companies” it works with, and they originate the loans locally, then provide the loans to Viventor for individual lenders to invest in.

Loan originators can be selected from the main loan listing screen as well as the auto-invest filters. To lean which originators I use, read on .

What Loan Types Does Viventor Offer?

Viventor provides mostly loans to consumers in the form of short term loans (30 – 90 days). They do also provide a few other types of loans, such as real estate loans, business development loans, invoice financing and also pawnbroking loans. However most loans I’ve seen on the platform are short term loans to consumers, as you can see in the screenshot below, that’s where most of the liquidity is.

What Loan Security Do Viventor Loans Offer? – Viventor Review

Both secured and unsecured loans are available on the platform. However most of the short term consumer loans have no asset security.

Remember the Viventor Buyback Guarantee offers security for lent out capital by buying back late loans, so asset security is less important, although not to be discounted if available. There are also other risk-mitigation factors with Viventor, namely their Payment Guarantee and originator “Skin-In-The-Game” (see the section further down on “Provision Fund” for more detailed information).

It’s easy to see if a loan does have loan security on the main loan listing screen as you can see below.

What Are The Current Viventor Default Rates? – Viventor Review

Viventor don’t publish their default rates. As most originators offer buyback guarantees & other risk-mitigation factors, default statistics are less important than if investing though a company like Zopa or Funding Circle that don’t offer any kind of buyback guarantee or provision fund, and therefore default rates can make a significant difference to your account yield.

Do Viventor Loans Amortize?

There are different types of loans on Viventor; fully amortizing, partially amortizing, interest only and bullet loans (balloon payment). Although because most loans are short term loans, they don’t amortize as they are typically paid back in full within a short day period (30 to 60 days in most cases for short term consumer loans).

Amortization is the paying off of debt with a fixed repayment schedule in regular installments over time. It reduces the risk of the loan compared to a non-amortizing loan in which nothing is received until the end of the loan period, or only interest is received monthly, and then the capital repaid at the end of the loan period.

It’s easy to see on the loan repayment schedule if a loan amortizes or not. As you can see below, payment include both interest and principle repayments, signifying this loan is amortizing.

How To Sell Loans & Withdraw Capital Early From Viventor

Viventor has a very active secondary market available. Selling loans in order to retrieve capital early is very easy. Just go to the “My Investments” screen and hit the “Sell” button.

Then you’re able to decide if you want to offer a discount to buyers, or you can also charge up to 1% more for loans if you think they will sell for more. Use the yellow slider to set the discount.

How to Purchase Loans from the Viventor Secondary Market

Investors can purchase loans from the secondary market either manually from the “Invest” screen, or set up an auto-invest portfolio which will automatically pick up loans which meet the predefined criteria as they become available.

The Viventor secondary market has the same filters as the primary, so it’s easy to set the lending criteria for buying loans.

How Easy Is It To Diversify With Viventor Loans? – Viventor Review

Diversifying capital into loans is easy with Viventor because of the size of their loan book and the multiple loan originators which offer loans through the Viventor marketplace.

Their predefined auto-invest portfolios diversify automatically based on the settings you give them, and with the self-select loans, you decide the amount you put into each loan.

Does Viventor Have A Provision Fund Or Buyback Guarantee?

There is technically no provision fund with Viventor. However the previously mentioned Viventor buyback guarantees provided by their loan originators really help to put more confidence in loans.

Buyback guarantees in my eyes are as good as, if not better than a single provision fund. This is because we are not relying on just one company to step in if a loan goes into default. Each originator is responsible for its own guarantee, which Viventor regulates to an extent. The risk of course is if an originator goes out of business, which has happened once in the past with a Mintos originator, but not with Viventor so far to my knowledge (although they have had trouble from one originator, Aforti, but they have not gone bankrupt as far as I am aware).

On top of this, some Viventor loan originators offer other types of risk mitigation including;

Payment Guarantee: Payment Guarantee reduces Investors’ exposure to borrowers’ late payments and default risk. If the loan is late, the Loan Originator guarantees monthly payments on behalf of the borrower.

Skin in the Game (5%): Loan originators on Viventor marketplace are required to keep at least a 5% stake in each loan, putting them in a similar position as other Investors. Should a borrower default, and the payments be delayed, the originator will lose money first, before other investors. This encourages lenders to engage in good due-diligence procedures in order to get the best quality borrowers.

What Is The Viventor Website Like? – Viventor Review

The Viventor Website is simple but effective. It’s fairly easy to figure out where everything is and how to set up auto-invest strategies or manually select loans.

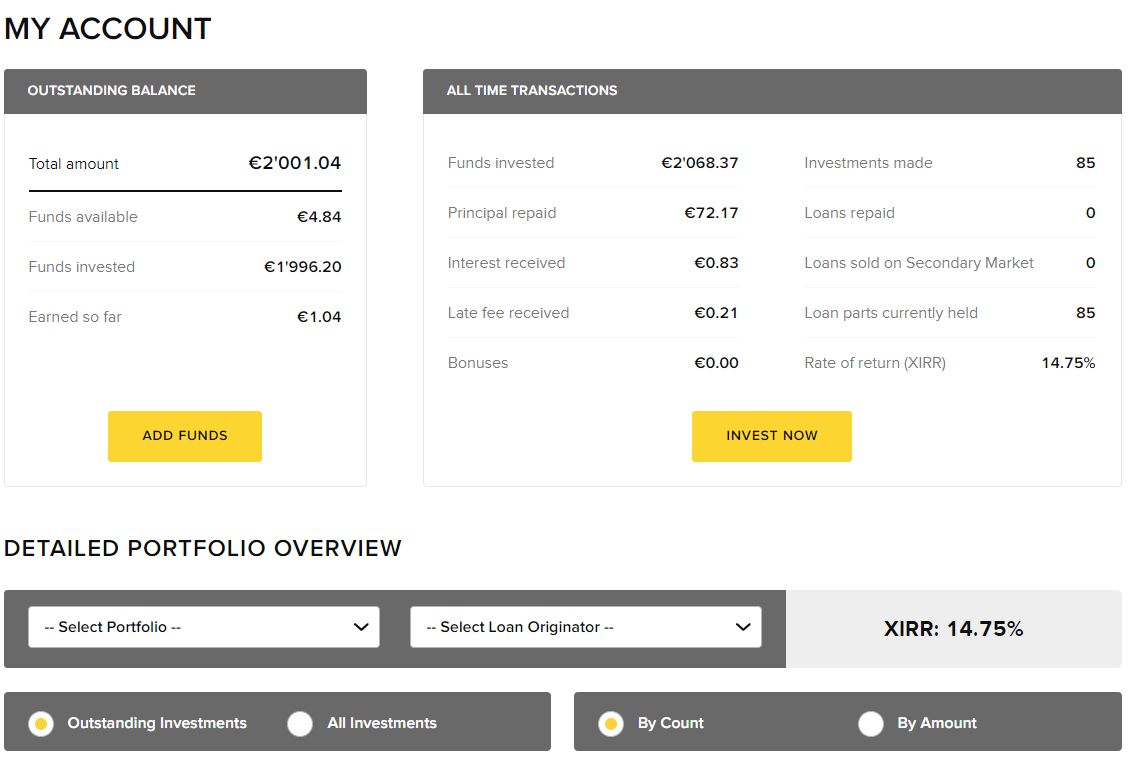

The home screen gives quite a lot of good information on your account including loan distribution and expected cashflow stats.

What Rate of Return Can I Expect From Viventor?

Viventor return rates are very good, at an average of around 13.57% since the platform launched. Although lately there have been a lot of 14.50%+ loans available. As you can see from the screenshot above, my current expected XIRR (according to the platform) is 14.75%.

My Personal Viventor Investment Strategies

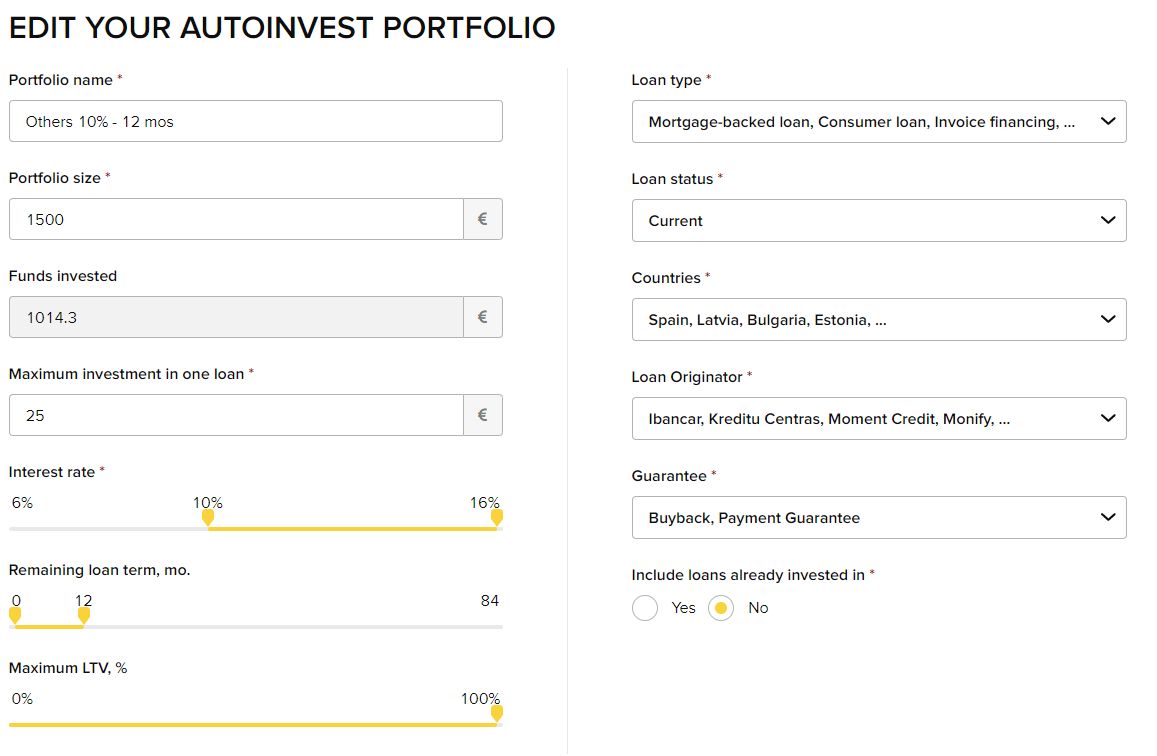

My Investment strategies with Viventor are simple. I choose a few specific originators which get good ratings in various areas like company size, profitability, history & transparency. Currently the loan originators I use are: Ibancar, Kviku, Kreditu Centras, Moment Credit, Monify, Stik Credit, Sofcom, Lenno, Atlantis Financiers & Credissimo. All of which offer a buyback guarantees & payment guarantees (select “buyback guarantee” & “payment guarantee” from the filters), and set the interest rates between 10% and 16%.

I actually have 2 auto-invest strategies, one that chooses a loan interval of up to 90 days with only loans from Kviku (there are a LOT of them right now), the other goes from 90 days to 12 months with all the other lenders. This is so I can get more diversified across lenders and not put everything into Kviku.

Then I set the loan max amount into any one loan at €25 as there are usually plenty of loans available (this will depend on your portfolio size of course).

The rest of the settings I use are in the screenshot below. Once set, I just hit “Save & Invest” and let the strategy go. As previously mentioned, it typically only takes a few hours for Viventor to get all funds loaned out.

Summary – Viventor P2P Review

Viventor is certainly a viable platform for lending out Euros. Their return rates are excellent for auto-invest, short term loans. With little to no time required to manage.

Viventor makes a great addition to any Euro portfolio for diversifying capital, both as a company, and as a marketplace with multiple loan originators.

The Viventor buyback guarantee, Payment Guarantee and Skin-In-The-Game add to the safety of the platform in my opinion.

Thumbs Up Points for Viventor

Unique Diversification – focusing on consumers and businesses in many different countries in Euro currency.

Great Returns – 16%+ possible for loans in Euros is a great rate.

Short Term Loans – If you don’t want to tie money up for long periods, there are usually plenty of short term loans available.

Auto-Invest – auto-invest options are nicely configurable allowing us to pick up just the loans we want in our portfolio.

Website Easy To Use – shortens the learning curve and time to get invested.

Secondary Market – active secondary market available for selling & buying loans.

Viventor Buyback Guarantee & Other Risk Mitigation Factors – most originators offer the “Viventor buyback guarantee” & “Viventor Payment Guarantee” and will buy back the loans if they go in to default, or make the payments if borrowers are late paying, therefor making investments safer.

Thumbs Down Points for Viventor

No Regulation – may make Viventor a riskier proposition, however having a good history and multiple loan originators for diversification helps lower the risk.

Latvian Based – for UK investors this may not be as comfortable as investing in UK companies. European investors don’t seem to see this as an issue though, and I certainly don’t.

Currency Risk – investing in a currency other than your home currency can have it’s own inherent risks if it falls. If your home currency is Euros then this is not an issue.

No Tax Free Savings Account – such as an ISA for interest free investing.

Still Coming Out of the Pandemic – some loan originators struggling to pay back investors.

Is Viventor P2P Safe? I consider Viventor to be in the medium risk category. Even taking in to consideration the Viventor risk mitigation factors, Viventor is still an unregulated business with a relatively short track record in a country far away from home for most of us (depending on where you live of course).

Who Can Invest with Viventor?

Safe?

Residents of most countries that can conform to the EU’s money laundering regulations can invest with Viventor. Contact Viventor for more information

This page is presented for informational purposes only. I am not a Financial Adviser and therefore not qualified to give financial advice. Please do your own research and make your own investment decisions. Do not make investment decisions based solely on the information presented on this website.

* My opinions, reviews, star ratings and risk ratings are based on my personal investing experience with the company being reviewed. These ratings are personal opinions and are subjective.

** Some of the links on this website are affiliate referral links. When you click on these links, I can sometimes receive a commission, at absolutely no cost to you. This helps me to continue to offer new reviews & monthly portfolio updates here on my website. I don’t receive commissions from all platforms and it has no effect on my ongoing opinions on investments & investment platforms. Income from my investments and capital preservation are my main motivations.

Platforms reviewed on this website I am currently investing with, or I have invested with in the past. You can see with full transparency on my Portfolio Returns page which assets & platforms I am invested with (or have previously been invested with) at any point in time. I am not paid a fee by any of the companies to write reviews, so the reviews are unbiased and purely based on my own personal experiences.

Please read my full website Disclaimerbefore making investment decisions.

The Obvious Investor website uses cookies to offer you the best possible browsing experience. By browsing this site, you give us the ok to use cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

_abck

1 year

This cookie is used to detect and defend when a client attempt to replay a cookie.This cookie manages the interaction with online bots and takes the appropriate actions.

bm_sz

4 hours

This cookie is set by the provider Akamai Bot Manager. This cookie is used to manage the interaction with the online bots. It also helps in fraud preventions

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_gat_gtag_UA_127056176_1

1 minute

This cookie is set by Google and is used to distinguish users.

_gat_UA-127056176-1

1 minute

This is a pattern type cookie set by Google Analytics, where the pattern element on the name contains the unique identity number of the account or website it relates to. It appears to be a variation of the _gat cookie which is used to limit the amount of data recorded by Google on high traffic volume websites.

_gcl_au

3 months

Provided by Google Tag Manager to experiment advertisement efficiency of websites using their services.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

NID

6 months

NID cookie, set by Google, is used for advertising purposes; to limit the number of times the user sees an ad, to mute unwanted ads, and to measure the effectiveness of ads.

(3.3 / 5)

(3.3 / 5)