The April 2020 P2P update will be similar to the March update as not a lot has changed. Once again I’ve outlined my strategy with each lender in order to protect capital while still trying to make some returns.

The update is a little late this month as we have a new addition to our family, so my focus has been on making sure everything goes well in that area before worrying about investments.

I haven’t yet updated the numbers spreadsheet on the website, but I am still tracking funds of course and I’ll update everything when things start to stabilize and I get some time. Just to give you an idea of where my investments are as of today, I still have £109,000 in GB Pound P2P investments (from a high of £205,000) and I also have €39,000 in Euro P2P (from a high of $54,000). So as you can see, I have reduced my exposure significantly, but I still hold substantial investments in P2P.

Moving On

It’s interesting how some lenders actually seem to be benefiting from this COVID 19 situation, and some are struggling. And not necessarily the ones you would think in each case. I’ve outlined my experience with each in April below.

Disclaimers

The information below is comprised of my opinions on current investment market conditions and my personal actions with my investments. It should not in any way be construed as financial advice. Please do your own research before making investment decisions and do not base them solely on what you read on this website. Please read my full disclaimer of more information.

Some of the links on this website are affiliate referral links. For cashback offers, you’ll generally need to use these links to qualify for the cashback. If you use these links I can sometimes receive a commission, at absolutely no cost to you. This helps me to run the website, write new platform reviews and publish monthly portfolio updates. I don’t receive commissions from all lenders, and it has no effect on my ongoing opinions on platforms, which are entirely focused on generating Income from my investments and preserving capital

Ablrate seem to be overall unaffected by this whole ordeal. I’m sure they have been affected but they are certainly not showing it like some of the others. Monthly payments on the whole seem to be coming in (there are some delays but not much it seems). I decided to sell a couple of loans with higher LTV’s and they sold quite easily so it seems like there is still investment capital coming in to Ablrate.

My Ablrate Strategy.

I’ll be leaving the rest of my capital with them for now as it seems Ablrate are handling things very well. I am gaining trust with them each month.

Ablrate Signup & Cashback Offers

Ablrate offer £50 cashback on your first £1,000 investment for readers of ObviousInvestor.com

Assetz Capital still seem to be struggling a bit with withdrawals from their Access Accounts. They are no longer frozen as they were in March as they are now using a queue system, but it is apparently still slow, I’m guessing due to lack of new funds coming in. Assetz also announced that they will be charging a 0.9% fee to all lenders (on repayments) in order to stay in business as their lending has pretty much ended because of the virus situation. Lending fees are basically where most of their income comes from it appears. They have also laid off many of their staff and directors have taken a large pay cut in order to bring costs down until the situation is over.

My Assetz Capital Strategy.

I have been unable get anything out of my Assetz Capital accounts as half is in the 90 Day Access Account (I did trigger the 90 day queue, but 3 months is a long time considering the current state of the economy). The rest is in the Great British Business Account and getting out of that now is nigh on impossible as loans have to be sold to other investors in order to exit early, and not many seem to be buying currently. So it will likely be a wait until the end of the loan terms (assuming they all get paid back of course). Otherwise it will be going through a default situation to recover assets.

When capital does become available to withdraw, I’ll have to see how things have progressed at that time to see if I actually do withdraw or reinvest with Assetz Capital. I will likely reduce my investment amount with them whatever.

CrowdProperty are another lender which seem to have been affected very little by the COVID 19 situation. They offer property secured development loans, all with first legal charge and reasonable LTV’s. I continue to feel like the loans they have written are well vetted, and are some of the safer development loans available in the P2P market. In the last few weeks of the COVID-19 panic, new CrowdProperty loans are still being written, and they have still been getting funded in a few minutes of being launched. These are large loans worth hundreds of thousands of pounds. This tells me that, even with panic and investors trying to withdraw capital from other platforms, CrowdProperty are still writing new loans and getting investment for them. This bodes well for sustainability moving forward.

My CrowdProperty Strategy.

My capital will be staying with CrowdProperty. I may even add more capital as things progress if the loans continue to be filled quickly and loans continue to be paid back on time. Of course I’ll keep an eye on things and this strategy could change at any time.

My Funding Circle strategy for the COVID-19 situation is the same as it has been since July 1st 2019 – trying to sell out and get my capital back. Nothing has changed, they still have no liquidity and all I’m doing is receiving monthly loan repayments (sometimes). I would not recommend investing new capital with Funding Circle.

Funds in Growth Street are still locked up as they are still in the midst of the “liquidity event”. They have sent out several emails saying they are working to resolve the situation so lenders can withdraw their capital. They are working with other organizations to try and refinance some of the debt, among other things. Currently they are about half way through their 90 day “liquidity event” which if not resolved before, will turn in to a “Resolution Event” which will then mean they request that all borrowers repay their loans and likely put them in to bankruptcy. Growth Street regularly send out emails updating investors on their situation. They try to be positive, but reading between the lines, I’m not so sure. Time will tell.

My Growth Street Strategy.

Once I get my remaining capital back (about 13k), I will likely have to consider seriously if I ever invest with Growth Street again (assuming they are still around).

Kuflinkis still bringing new loans to the platform, and they are still being filled quickly (although a little slower than normal). This shows that investors still trust Kuflink enough to invest with them. My feeling is Kuflink will be one of the lenders who come out of this situation unscathed and possibly even stronger. They will likely be getting a lot of new investors from Assetz Capital, Growth Street & Lending Works I imagine.

My Kuflink Strategy.

I initially sold down just a few of the higher LTV loans on the secondary market (only 10% of total account value), just for piece of mind as we don’t know how bad this situation might get. Most of my capital is still with Kuflink though. I’ll be leaving it there for now and probably also lending into new lower LTV loans as they become available. Of course I’ll keep an eye on things and this strategy could change at any time.

Kuflink Signup & Cashback Offers

Kuflink have a great cashback offer right now which is well worth taking advantage of if you are thinking of investing with them. You can get up to £500 in cashback bonus (depending on how much you invest).

New Kuflink customers receive the following Kuflink cashback on an investment of £100 or more when they use signup links from obviousinvestor.com. Must invest into loans within 14 days of first investment to qualify for cashback.

I decided to retrieve capital (where possible) from lenders who have unsecured loans to reduce my overall exposure to Peer to Peer lending. Although LendingCrowd do have some secured loans, many just have directors personal guarantees. Historically, trying to recover from just these personal guarantees has been hit and miss. So, I made an early decision to withdraw my capital. I was able to sell about 75% of the loans as I was early to start selling in March. I still have about 2.5k left in there and I’ll just draw that down as payments are made as the secondary market has now frozen up it seems.

My LendingCrowd Strategy.

Everything worked out (almost) as expected with LendingCrowd when I started to sell loans. Although I still have a little money with them, I am still receiving payments monthly (although not as much as it should be as obviously some borrowers are not able to pay). I’ll have no hesitation about investing with LendingCrowd again once things normalize, but for now, I’m happy to stand on the sidelines with most my capital in the bank.

I’m lucky as I was able to sell almost all of my Lending Works loans and get out right before the liquidity run came and everyone was trying to withdraw. I still have about £300 stuck in the account but considering that it was 30k at one point, I’m not sweating it.

My Lending Works Strategy.

One thing that irritated me and got a lot of investors upset in March: Lending Works had sneakily slipped in to their T&C’s back in December that people withdrawing loans early are now not only subject to a .5% fee (which I always thought was acceptable), but they are now subject to a shortfall in any loan rates. It really wasn’t clear to most people that they had done this, so when I withdrew my funds, there was another few hundred I had to pay in order to get out. Irritating and reduced the returns on the account, and I will have to really contemplate if I ever want to invest with them again as my trust for this company is weak now. It amazes me that companies like this do underhanded things and expect people will still invest with them.

Loanpad seem to be really benefiting from this situation. I keep in contact with their staff and they say they are still getting a lot of new investors. A few have signed up from this website so I have to believe them. Loanpad offer property secured loans, all with very low LTV’s (all below 50%, and many between 5% and 15%). These kinds of LTV’s mean even if UK property values take a huge nosedive because of the recession, even in the event of a default, lenders would probably get their capital back. In the last few weeks of the COVID-19 panic, Loanpad, although a smaller company, have been able to survive and fulfill capital withdrawal requests even from their “Classic” instant access account without having to declare a “Liquidity Event” and suspend capital withdrawals. Even today it is still possible to get capital out without a problem.

At the beginning of May, Loanpad did send out an email saying they are reducing return rates on their accounts by .50%. So they are still paying 3.5% on their classic account, and 4.5% on the Premier account. We really shouldn’t complain about that when we consider RateSetter (one of the largest lenders) still has many investors capital frozen, and on top of they they just reduced rates on their “Access” account to 1.50% and on their “Max” account from 4% to 2%.

My Loanpad Strategy.

Capital will be staying with Loanpad (it’s in the Premium 60 Day Access Account). I’ve really liked the safety aspect of Loanpad since I started investing with them and it looks like, so far at least, I was correct with this one. They are still getting new investors at a high rate so they are one of the lenders who actually seem to be benefiting from this situation.

Loanpad Signup & Cashback Offers

Loanpad have a great cashback incentive for readers of ObviousInvestor.com if you’re thinking of joining:

£50 bonus if you invest into a lending account a minimum of £1,000 within 4 weeks post registration and keep this invested for 365 days.

£150 bonus if you invest into a lending account a minimum of £10,000 within 4 weeks post registration and keep this invested for 365 days.

Not much changed in Mintos since last month: Most of my Euro loans are short term payday loans. As I’ve decided to get out of unsecured lending until things calm down, I switched my Mintos auto-invest strategies off so loans will complete at term. Most loans in Euros were less than 30 days so I was hoping I would just be able to get my capital back. Of course the news that Varks Armenia (part of the Finko Group) lost it’s lending license in March came out, and guess who most of my short term loans were with 🙄 Not the end of the world though as because Varks are part of the Finko group, there is a group guarantee in place on the Mintos platform. This means that Finko will have to honor the Varks loans. Providing Finko stay in business, capital should be returned eventually. I’ve been getting small amounts each day so I’m quite confident that eventually I should get this capital back.

I sold down many of the Mogo GBP car loans just because they are finished anyway (no new GBP car loans on Mintos now), and I thought better to reduce exposure to Mintos as a whole. I still have about £1,500 in Mogo loans which are already late or in default, so the buyback guarantees should all kick in within 60 days. I have been slowly getting some of this capital back and Mogo are a strong originator so hopefully that will continue.

My Mintos Strategy.

As stated above, I’ll withdraw capital from Mintos as and when able. I have no problems with Mintos though and as soon as things stabilize, I’ll likely reinvest with them as I still think Mintos is one of the best platforms “under normal market conditions” 🙂

I exited Octopus Choice in March. Even though they have well asset secured loans, I decided to exit this account anyway for now as 4% is just not worth the risk, and there was no penalty for withdrawal. I was early in making my withdrawal request so was able to get all of my money out (except for a couple of hundred that were in late loans). My feeling is that it’s better to have the capital in a government protected bank account for now, while things calm down. It’s always easy with Octopus Choice to get back in to the loans when things settle down.

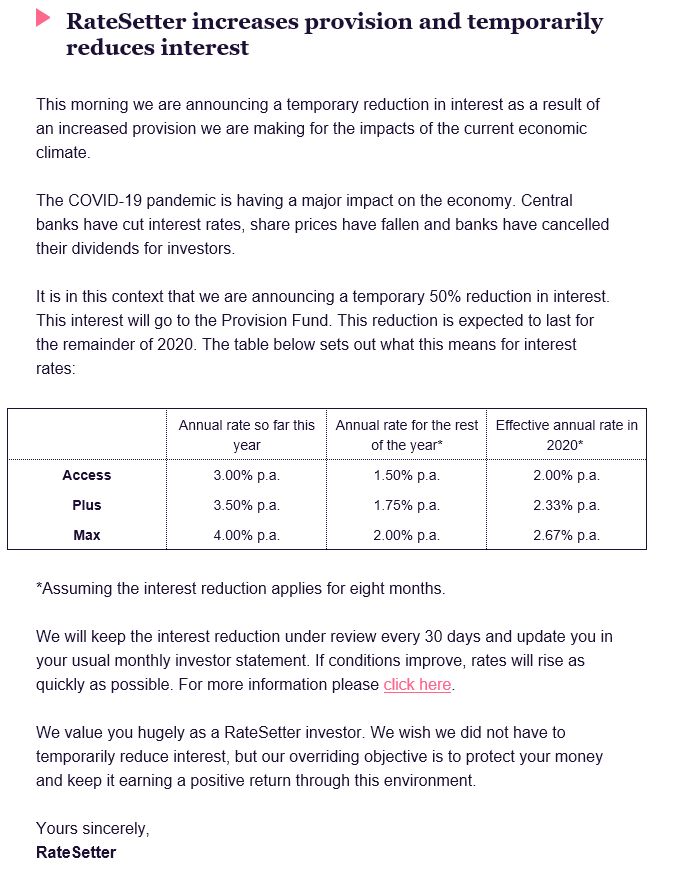

I decided to exit RateSetter March and I was lucky to get out before the liquidity problems set in (still have about £20 stuck in late loans, but considering the account was once £30k, well, you get the picture). A couple of days after I made my withdrawal, RateSetter started to have liquidity problems and now there is quite a long wait to get loans sold and capital out. I think I made the right decision.

To top this off, RateSetter just a couple of days ago sent out the following email saying they are reducing interest rates AGAIN for the rest of the year. 2% for the Max account now? and 1.5% for Access? We can get 1.5% in a FSCS backed bank account with instant access!!! Why the heck would we want to invest with RateSetter? Of course, for the folks that have capital stuck there, not a great update. I read on some of the P2P groups there are some unhappy investors who were (until now) still RateSetter fans.

My RateSetter Strategy.

I am just happy I was able to get out of RateSetter. Unlikely I will ever invest with them again after this. I’ll actually be surprised if they are still in business in a year.

Unbolted are still doing very well it seems. I keep getting repayments as agreed and defaulted items are still being sold. As I had thought, Unbolted are one of the companies that are benefiting from the COVID 19 situation.

Unbolted offer pawnshop style loans to the general public with very liquid assets. These types of assets can be sold very quickly upon default. Pawnshops typically do better in economic downturns than they do in times of prosperity as people will borrow against personal assets when they are unable to get an unsecured personal loans. LTV’s are usually very low as defaults can be high, so pawnshops need to make sure they can always recoup capital. I have been lending with Unbolted for a couple of years now, and although there have been many defaults, assets have always sold at more than the outstanding loan principle and I have always been paid back both principle and interest very quickly. Loans are short to medium term in nature so a complete exit can be had by turning off auto-invest within 3 to 12 months.

My Unbolted Strategy.

I’ll keep investing with Unbolted as normal as I expect them to be one of the most lucrative investments throughout a recession. Still averaging around 8% returns so no complaints here.

Unbolted Signup & Cashback Offers

Unbolted has a cashback bonus for ObviousInvestor.com readers – £50 cashback if you invest just £1,000 by using the the link below.

UOWN are an interesting company and off the usual Peer to Peer lender “track” for me. They are not a Peer to Peer lender but a crowdfunding platform where investors own shares in the properties. Although they haven’t put out any new development loans since the beginning of the COVID 19 situation, payments on rental properties are still being received as normal.

My UOWN Strategy

I decided to stay fully invested with UOWN. As we actually own shares in the properties (not loans) there can be no defaults. The risk here is that developments might not be sold at the same value (if property prices crash), or perhaps a renter can’t always be found for rental income properties. Either way, even in the worse case scenario, I think most of my capital should be recoverable.

So far communication to investors from Crowdestor has been very good. They actually seem to be doing quite well in spite of the situation. I have seen a couple of developer jobs they have posted so they can’t be struggling too much. Although Crowdestor made the decision to pause all repayments from borrowers (and to investors, which upset a few of them as you can imagine) for 90 days to give them breathing space while the COVID-19 is in the initial stages. They don’t appear to be too worried about the business moving forward. Time will tell I guess.

My Crowdestor Strategy

As Crowdestor don’t have any option for early withdrawal (except selling some of the loans at a large 20% discount, which I’m not willing to do), I’ll be riding out the COVID-19 downturn with them until things stabilize. They have been very professional so far so I see no reason I won’t keep investing with them in the future.

In January I did a full write up on the Envestio situation (was a scam). If you missed that, you can read it here in the January update.

It appears that the class-action law suite is progressing aggressively but there are really no more updates than that. I read they have over €10 million in claims against Envestio from a few thousand investors. I’m obviously skeptical about getting anything out of these investments, although most were asset secured so time will only tell.

Grupeer

I’m still a little confused with Grupeer. Last month I mentioned that it appeared like Grupeer are some kind of scam, and they may well be. There are conflicting stories though. There is a lawsuit being arranged by some of the investors (here’s a link to a website specifically about Grupeer and the legal action). Grupeer have been putting out blog updates saying different things that don’t make any sense like “they expect stabilization in 1 to 2 years” whatever that means. They do not reply directly to investors queries though, which tells me they are likely just stalling for time. I tried to make a withdrawal from the Grupeer platform back in March which never reached my bank account.

My Grupeer Strategy

I’m not convinced I’ll ever see my investment in Grupeer again, and if I do, I definitely won’t invest with them again after this.

PeerBerry have actually turned out to be one of the most reliable Euro lenders so far. They are communicating and managing their loans, and the situation well. Capital has been easy to withdraw from the platform and most of it arrives in my bank account the next day.

My PeerBerry Strategy

I have drawn down my account about 50%, but I’ve decided to stay invested with what’s left for now and I’ll keep a close eye on loan delays etc. PeerBerry thus far have shown they are one of the better (if not the best) Euro Peer to Peer lenders. As soon as things start to pick up, I’ll have no hesitation at all in increasing my investment again with PeerBerry.

PeerBerry Signup & Cashback Offers

No cashback offers with PeerBerry this month, however if you would like to take a closer look at their platform, please;

Robocash seem to be communicating and managing their loans well. So far capital has been easy to withdraw from the platform and most of it arrives in my bank account the next day.

As most of the loans on Robocash are unsecured, I’ve decided to switch off reinvestment for now and withdraw capital as it is paid back. Robocash has both short term and long term loans. I’ve already managed to withdraw capital from a lot of repaid short term loans. The longer term loans are up to 1 year so I’ll just withdraw that capital as it is paid back until I reduce my overall exposure to about 50%.

My Robocash Strategy

For now, I’ll keep withdrawing capital until I get the account to about 50% of my overall investment, just to reduce exposure. As soon as things start to pick up, I’ll have no hesitation at all in jumping back in to Robocash.

Swaper is another lender that seems to be doing ok with the COVID 19 situation. Communication is good and it appears to be mostly business as usual, although many loans are delayed of course as borrowers are not working. So far capital has been easy to withdraw from the platform as it is repaid, and most of it arrives in my bank account the next day. I’m not concerned about Swaper as a company, but short term, unsecured payday & personal loans will be the first to default if this lockdown is sustained and people can’t work. So I’m not sure how much pressure mass defaults would put on Swaper.

My Swaper Strategy

As most of the loans on Swaper are short term, unsecured loans; I’ve decided to switch off reinvestment for now and withdraw capital as it is paid back in order to reduce exposure. Once I get to about 50% of my original investment, I’ll reassess.

Viventor are communicating and managing their loans well. They’ve done a couple of webinars for investors to explain the situation and how they are handling it which was well accepted. Many loans are delayed of course but so far capital has been easy to withdraw from the platform when it is repaid and it arrives in my bank account the next day.

My Viventor Strategy

Again, most of the loans on Viventor are unsecured, so I’ve decided to switch off reinvestment for now and withdraw capital as it is paid back in order to reduce exposure.

Overall, not too many changes from last month. Although it looks like many countries are starting to try and come out of lockdown, the damage done by almost 2 months of this so far has likely still yet to have major impact on the world economy.

We are starting to see now the platforms that are worth their salt. Some of the platforms we may have thought were solid (RateSetter, Funding Circle, Growth Street etc.) have shown that under pressure they are unlikely to survive, where other smaller platforms are showing they were well prepared. The most positive thing about this whole situation as far as the P2P lending space is concerned is; when we come out the other side of this situation, the lenders that are still in business will be much safer investments having been through this whole ordeal.

If you do decide to invest in P2P in the current environment, I suggest you stick with lenders with good asset security and low LTV’s like Kuflink, Loanpad, CrowdProperty & Unbolted. Do not take my word for it though, do your own research and make your own investment decisions. For some it will be better just to keep all of your capital in a FSCS insured bank accounts for now.

Good luck with your investments moving forward. I suggest protecting yourself as much as possible, and remember Warren Buffett’s rules; “don’t lose money”, because without capital to invest in the future, it doesn’t matter how good the investment opportunities are.

My best to you and your families. Stay safe and I’ll post an investment update again soon.

Disclaimers:

This page is presented for informational purposes only. I am not a Financial Adviser and therefore not qualified to give financial advice. Please do your own research and make your own investment decisions. Do not make investment decisions based solely on the information presented on this website.

* My opinions, reviews, star ratings and risk ratings are based on my personal investing experience with the company being reviewed. These ratings are personal opinions and are subjective.

** Some of the links on this website are affiliate referral links. When you click on these links, I can sometimes receive a commission, at absolutely no cost to you. This helps me to continue to offer new reviews & monthly portfolio updates here on my website. I don’t receive commissions from all platforms and it has no effect on my ongoing opinions on investments & investment platforms. Income from my investments and capital preservation are my main motivations.

Platforms reviewed on this website I am currently investing with, or I have invested with in the past. You can see with full transparency on my Portfolio Returns page which assets & platforms I am invested with (or have previously been invested with) at any point in time. I am not paid a fee by any of the companies to write reviews, so the reviews are unbiased and purely based on my own personal experiences.

Please read my full website Disclaimerbefore making investment decisions.

2 thoughts on “P2P Lending Portfolio Update For April 2020”

Stan

Just check Ratsetter hasn’t shunted you onto 2.4% as happened to me, folks.

You can set rate on direct debit and reinvestments separately.

Currently matching at 4.2%.

Which you can cut in half.

I put in a request to Assetzcapital on their 90 day access account back in Jan. Was supposed to get it mid April, and even that is totally stuck in the “queuing system”. Not even had 10% of the request filled yet, guessing i’m going to be waiting months. Which is a little annoying- since I put the request in so early. Guessing it’s the 30 day notice account that it’s queued alongside. Oh well, let’s hope it doesn’t last too long!

The Obvious Investor website uses cookies to offer you the best possible browsing experience. By browsing this site, you give us the ok to use cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

_abck

1 year

This cookie is used to detect and defend when a client attempt to replay a cookie.This cookie manages the interaction with online bots and takes the appropriate actions.

bm_sz

4 hours

This cookie is set by the provider Akamai Bot Manager. This cookie is used to manage the interaction with the online bots. It also helps in fraud preventions

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_gat_gtag_UA_127056176_1

1 minute

This cookie is set by Google and is used to distinguish users.

_gat_UA-127056176-1

1 minute

This is a pattern type cookie set by Google Analytics, where the pattern element on the name contains the unique identity number of the account or website it relates to. It appears to be a variation of the _gat cookie which is used to limit the amount of data recorded by Google on high traffic volume websites.

_gcl_au

3 months

Provided by Google Tag Manager to experiment advertisement efficiency of websites using their services.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

NID

6 months

NID cookie, set by Google, is used for advertising purposes; to limit the number of times the user sees an ad, to mute unwanted ads, and to measure the effectiveness of ads.

Just check Ratsetter hasn’t shunted you onto 2.4% as happened to me, folks.

You can set rate on direct debit and reinvestments separately.

Currently matching at 4.2%.

Which you can cut in half.

I put in a request to Assetzcapital on their 90 day access account back in Jan. Was supposed to get it mid April, and even that is totally stuck in the “queuing system”. Not even had 10% of the request filled yet, guessing i’m going to be waiting months. Which is a little annoying- since I put the request in so early. Guessing it’s the 30 day notice account that it’s queued alongside. Oh well, let’s hope it doesn’t last too long!